EMISSIONS: EU Mid-Day Carbon Summary: EUAs/UKAs Rise On Mixed Signals

EUAs Dec25 are rangebound, influenced by both TTF and EU equities movements, with TTF down on steady storage injections, while EU equities up on optimism over potential ceasefire in Ukraine. Meanwhile, UKA Dec25 are edging higher after the BOE cut interest rates to a two-year low, from 4.25% to 4%, in line with market expectations. The market is pricing in one more rate cut by year-end to around 3.5%, as the BOE forecasts inflation to peak at 4% in September.

- EUA DEC 25 up 0.21% at 71.14 EUR/t CO2e

- UKA DEC 25 up 0.74% at 50.69 GBP/t CO2e

- TTF Gas SEP 25 down 0.8% at 33.005 EUR/MWh

- NBP Gas SEP 25 down 1.1% at 81.21 GBp/therm

- Estoxx 50 up 1.6% at 5346.54

- FTSE 100 SEP 25 down 0.6% at 9101.5

- The latest EU ETS CAP3 auction cleared at €70.1/ton CO2e, up 0.04% compared with the previous EU auction at €70.07/ton CO2e according to EEX.

- The UKA auction cleared at a premium to the Dec25 futures contract for a second consecutive session, though no clear pattern in the spread has been identified, ICE data showed.

- Uniper cut direct CO2 emissions by 24% y/y in H1 2025 to 6.3mn tonnes, down from 8.3mn tonnes in the same period of 2024, and expects full-year emissions to fall significantly below 2024 levels, it said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bobl Call Spread seller

OEQ5 117.25/117.50cs sold at 12 in 8k.

OUTLOOK: Price Signal Summary -Bunds and Gilts Clear Support

- In the FI space, Bund futures are trading lower today, extending Monday’s sell-off. Support at 129.77, the Jul 3 low, has been cleared. The clear break confirms a resumption of the recent bearish theme and opens 129.30 next, the May 22 low. On the upside, resistance around the the 50-day EMA, at 130.51, has recently been pierced but for now, remains intact. A clear break of it is required to highlight a possible reversal.

- A bear cycle in Gilt futures remains in play and today’s sell-off reinforces this theme. The contract has breached support at 91.63, the Jul 2 low. Price has also pierced 91.50, the 61.8% retracement of the May 22 - Jul 1 bull leg. This exposes 90.97, the 76.4% retracement point. Clearance of this level would strengthen a bullish theme. On the upside, initial firm resistance is at 92.61, the 20-day EMA.

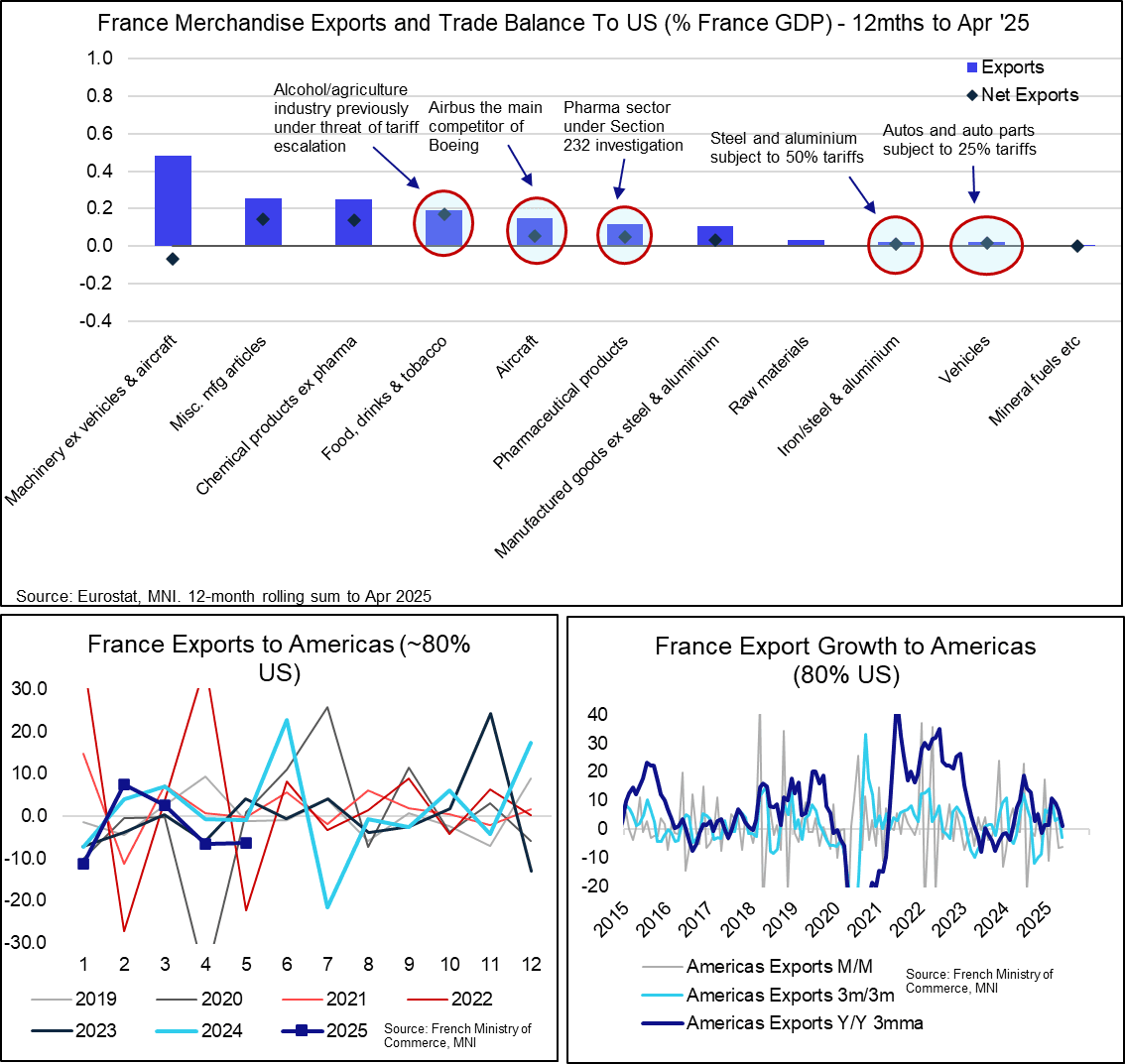

FRANCE DATA: Tariff Impact Clear, But Several Risks Still In Pipeline (2/2)

Ministry of Commerce data highlights a sharp drop in Y/Y French exports to the Americas since March, with exports falling 6.5% M/M in April and 6.4% M/M in May. The US makes up around ~80% of “Americas” exports. Clearly, already implemented tariffs and associated trade policy uncertainty are having an impact on trade with the US.

- However, Eurostat data suggests France is not too exposed to the sector-specific 50% steel/aluminium and 25% autos levies imposed by the US.

- Instead, officials will be more concerned by French sensitivity to:

- (i) Pharmaceuticals, which are currently subject to a Section 232 investigation.

- (ii) Aircraft, given Airbus’ position as Boeing’s main competitor.

- (iii) Food, alcohol and tobacco, with the agricultural sector threatened with 17% tariffs over the weekend and the alcohol sector previously being threatened with punitive measures following initial EU retaliatory plans.

- Other machinery/manufacturing exports to the US are also worth ~0.8% GDP, so are impacted by the 10% baseline reciprocal tariff.

- This sensitivity to potential future tariff announcements has likely underscored the French Government’s slower, more detailed, preference for trade negotiations than the likes of Germany (whose auto industry is more sensitive to already-announced sector-specific tariffs, for example). Reports that spirits and aircraft may be exempted from tariffs in the latest US offer will come as a relief to some French producers.