MNI US OPEN - US Government Shutdown Enters Second Day

EXECUTIVE SUMMARY

- TRUMP RAISES STAKES FOR GOP WITH SHUTDOWN ENTERING SECOND DAY

- US TO PROVIDE UKRAINE WITH INTELLIGENCE FOR STRIKES DEEP INSIDE RUSSIA: WSJ

- GOOLSBEE SAYS LACK OF OFFICIAL DATA DURING SHUTDOWN HARD FOR FED

- UNCHANGED SNB MARKET PRICING WARRANTED LOOKING AT CPI DETAILS

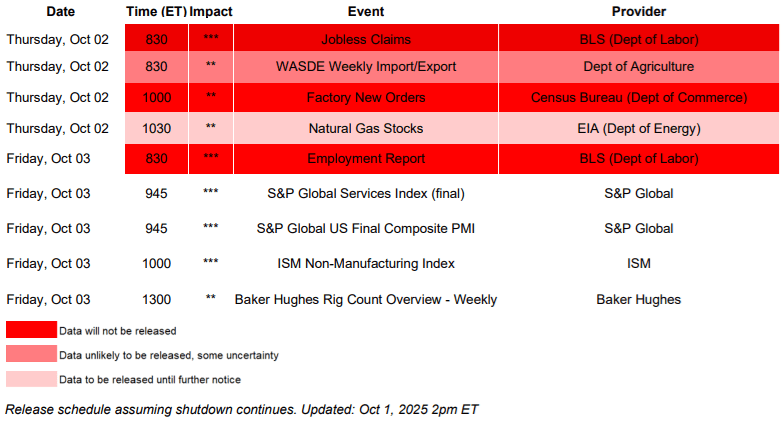

Figure 1: This week's US Data Releases in Federal Government Shutdown

NEWS

US (MNI): Guide to US Data Releases in Federal Government Shutdown

We've updated our shutdown data calendar to make clearer that weekly jobless claims will not be released so long as the shutdown goes on (despite some speculation we had heard to the contrary, the BLS messaging Tueaday night and Wednesday has been clear enough). We are also confident that nonfarm payrolls will not be released Friday. That still gives us a little labor market data Thursday morning though it is not listed on our calendar: Challenger job cuts at 0730ET and the Chicago Fed's new Labor Market Indicators release at 0830ET.

US (BBG): Trump Raises Stakes for GOP With Shutdown Entering Second Day

The US government shutdown entered its second day with the Trump administration having raised the stakes in its showdown with Democrats, first by punishing the home city of its two leading antagonists and then by signaling a willingness to fire thousands of federal workers, despite some Republicans’ concerns that the strategy could backfire.

US/UKRAINE (WSJ): U.S. to Provide Ukraine With Intelligence for Missile Strikes Deep Inside Russia

The U.S. will provide Ukraine with intelligence for long-range missile strikes on Russia's energy infrastructure, American officials said, as the Trump administration weighs sending Kyiv powerful weapons that could put in range more targets within Russia. President Trump recently signed off on allowing intelligence agencies and the Pentagon to aid Kyiv with the strikes. U.S. officials are asking North Atlantic Treaty Organization allies to provide similar support, these people said. The expanded intelligence-sharing with Kyiv is the latest sign that Trump is deepening support for Ukraine as his efforts to advance peace talks have stalled.

US/CHINA (BBG): Trump’s Signal on China Trade Talks Lifts Soybean Prices

Soybean prices bounced back after US President Donald Trump on Wednesday said he would press Chinese President Xi Jinping to restart purchases of the crop when the two meet at the end of the month. “I’ll be meeting with President Xi, of China, in four weeks, and Soybeans will be a major topic of discussion,” Trump posted Wednesday on social media. “It’s all going to work out very well.”

FED (BBG): Goolsbee Says Lack of Official Data During Shutdown Hard for Fed

Federal Reserve Bank of Chicago President Austan Goolsbee said a lack of official data while the US government is shut down will make it harder for central bankers to interpret the economy. Goolsbee reiterated concerns about a recent pickup in services inflation, which he said could mean price pressures are persistent in parts of the economy least impacted by tariffs. While there are many non-government sources of data on the labor market, the same isn’t true for inflation statistics, he said.

EU/RUSSIA (MNI): Belgian PM Demands Risk-Sharing on Using Frozen Russian Assets

Ahead of a meeting of the European Political Community, Belgian PM Bart De Wever says he told EU leaders, "I want your signature," that they will share the risk if the EU uses frozen Russian assets for a 'reparations loan' for Ukraine. Around EUR200bln of frozen Russian assets are held at Belgium's Euroclear, making the stance of the De Wever gov't crucial in determining whether the plans go ahead. De Wever calls on other European countries to be "transparent" about how much they hold in frozen Russian assets. MNI's Political Risk team posted a short PDF outlining the EU's ideas for using frozen Russian assets, the obstacles

it faces, and the risks posed (see here).

G7/RUSSIA (BBG): G-7 Nears Agreement to Ramp Up Curbs on Russian Oil Revenue

Group of Seven nations are closing in on an agreement to significantly increase sanctions on Russia over its continued war in Ukraine, according to a statement released after a finance ministers’ meeting on Wednesday. “We are aligned on the need to act together and believe that now is the time for a significant coordinated escalation of measures to bolster Ukraine’s resilience and critically impair Russia’s ability to wage war against Ukraine,” the statement said.

EU (BBG): EU to Propose Doubling Tariff Rate on Steel Imports to 50%

The European Union plans to hike tariffs on its steel imports to 50%, according to a draft proposal seen by Bloomberg. The move will align the bloc’s rate with the US, which has sought to push back against overcapacity from China. The EU currently has a temporary mechanism in place to safeguard its steel industry, which imposes a 25% duty on most imports once quotas are exhausted. That mechanism expires next year and the EU has been working to replace it with a more permanent instrument, which it plans to unveil next week.

BOJ (BBG): BOJ’s Deputy Chief Reiterates Stance on Rate Hikes After Tankan

Deputy Governor Shinichi Uchida reaffirmed the Bank of Japan’s standing policy to raise benchmark interest rates if the economy performs in line with forecasts, in comments a day after a key indicator showed business sentiment remains positive. “If the outlook for economic activity and prices is realized, the bank will continue to raise the policy interest rate and adjust the degree of monetary accommodation accordingly,” Uchida said Thursday in a brief speech at a financial conference in Tokyo.

JAPAN (BBG): Japan’s 10-Year Bonds Slip on Caution After Another Weak Auction

Japan’s 10-year government bonds edged lower after the second poorly received auction this week, underscoring jitters over the ruling party’s looming leadership election as well as growing risks of a Bank of Japan rate hike. The benchmark yield rose half a basis point to 1.65% while bond futures gave up their earlier gains. The average bid-to-cover ratio in the sale of 10-year debt fell to 3.34, compared with 3.92 in September.

CORPORATE (BBG): Samsung, SK Hynix Shares Leap After OpenAI Taps Korea for Chips

Samsung Electronics Co. and SK Hynix Inc. shares rose to their highest in years after South Korea’s largest companies forged initial agreements to supply chips to OpenAI’s Stargate project, reinforcing their lead in artificial intelligence memory. OpenAI’s Sam Altman signed a letter of intent Wednesday to enlist the two firms in his data center construction effort, a global undertaking that involves the sector’s biggest players from Nvidia Corp. to Oracle Corp. The US startup could need as many as 900,000 wafers per month as Stargate expands, the companies said.

DATA

EUROZONE AUG UNEMPLOYMENT RATE 6.3% (VS 6.2% JUL) (MNI)

UK DATA (MNI): DMP Data Has Something for Both the Hawks and Doves

The DMP survey showed an increase in own price growth (but probably largely expected) and fall in realised employment (but also well flagged by last month's single month data). Wage growth expectations continue to remain stable at 3.6% Y/Y for the year ahead. We don't think this data will change the opinion of any MPC member. It's got something for both the more dovish and more hawkish members in here. Realised price growth increased to 4.1% Y/Y (4.06% Y/Y unrounded) in the single month measure in September (from 3.6% Y/Y in August). This was the first time above 4.0% since September 2024.

SWITZERLAND DATA (MNI): Unchanged SNB Market Pricing Warranted Looking at CPI Details

- SWISS SEP CPI -0.2% M/M, +0.2% Y/Y

- SWISS SEP SERVICES CPI +1.4% Y/Y

Looking at the details of Swiss September CPI, there were multiple moving parts in the data. Having said that, the big picture remains that inflation remains within the SNB target, keeping market expectations for further meetings roughly unchanged at around 10bps of easing priced through June 2026. Contributions of services excl. rents rose for the fourth consecutive month in September. However, the September increase was driven by hotels and package holidays, which added 0.15pp in contribution - meaning that without these (often volatile) categories, services excl. rents look a bit softer than in August.

AUSTRALIA DATA (MNI): Services Keep Consumption Positive, Next Month Q3 Volumes Print

August household consumption was weaker than expected rising 0.1% m/m with the annual rate slowing to 5.0% from 5.3% but still above the series average. The RBA noted in September that private consumption was stronger than it expected as financial conditions have eased and real incomes are higher. While the monthly data are nominal, it will be monitoring the quarterly volumes included in the September release on 3 November before the 4 November RBA decision.

AUSTRALIA DATA (MNI): Trade Surplus Lowest in Over 7 Years

- AUSTRALIA AUG TRADE BALANCE A$+1825

Australia's merchandise trade surplus narrowed to $1825mn in August from a downwardly-revised $6612mn, which was significantly more than expected. The weakness was driven by a sharp 7.8% m/m drop in exports while imports rose 3.2%, but it is worth noting that the former has been gradually recovering over the last two years. This was the lowest surplus in over seven years.

FOREX: USD Index Lower Again, But Lack of Data Could Contain Vol

- Into the second day of a US government shutdown, and the USD is weaker again, pressuring the USD Index to trade lower for a fifth consecutive session. Yesterday's 97.462 low is in tact for now, largely as USD/JPY is yet to make another convincing move lower, after yesterday's downside bias has failed to spill over into Thursday trade. That said, support into 146.59 is well within reach, but the lack of US data may contain intraday vol in the interim, and prevent any furher breakout here.

- Global equities trade well, helping underpin a climb for EURUSD to 1.1757. $6.86bn of option notional expire today between 1.1695/1.1800 - these sizeable strikes could further contain spot into the NY cut. The trend condition in the pair is bullish, and a clear resumption of gains would open 1.1923, a Fibonacci projection. Support to watch lies at 1.1686. the 50-day EMA.

- NZD outperforms in a partial reversal of recent AUDNZD price action. Profit taking may be at play as the AU-NZ 2yr swap spread holds firm, just off recent highs. This has been the strong driver of the cross, evident in the EMAs pointing north, with key resistance and the 2022 high standing at 1.1491. The 20-day EMA meanwhile sits at 1.1259.

- With a lack of US data, central bank speakers are in focus. Today sees ECB's Makhlouf, Kazaks, Villeroy & de Guindos as well as Fed's Logan & Goolsbee.

BONDS: Tight Ranges for Core Bonds, Mixed Supply Outcomes

Bund futures little changed at 128.605. Initial support and resistance at 128.26/24 & 128.82 remain intact. Our technical analysts suggests that recent gains in the contract only appear corrective, with the medium-term bearish theme intact.

- German yields flat to 1.5bp lower, curves flatter.

- EGB spreads to Bunds flat. OAT supply passed smoothly.

- EUR 10s30s swaps curve holds steeper after one of the larger Dutch pension funds showed increased confidence in its proposed pension transition date yesterday, shy of September highs.

- Gilts also in narrow ranges. Futures flat at ~90.90. Bears remain in technical control, with initial support and resistance still located at 90.26 & 91.28, respectively.

- Fiscal worry remains front and centre for the UK long end. The latest FT report has reaffirmed existing estimates surrounding the fiscal “black hole” (~GBP30bln).

- 10-Year gilt supply saw soft demand. The bid/cover was lowest seen at a 10-Year auction since ’23, albeit skewed by increased auction sizes over that horizon.

- BoE-dated OIS still shows just ~5bp of BoE easing through year-end. We continue to suggest that the market underprices the odds of a Q4 cut.

- The latest BoE DMP survey had something for both the hawks and doves.

- Looking forwards, ECBspeak from de Guindos, Villeroy and Makhlouf is due this afternoon. Don’t expect much in the way of meaningful view changes/fresh commentary given the broader accord currently struck within the Governing Council and the fact that all three have spoken recently. EUR STIRs show less than 10bp of additional easing in the current cycle.

EQUITIES: Bull Cycle in E-Mini S&P Intact as Contract Trades to Fresh Cycle High

Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens 5646.00 next, a Fibonacci projection, with potential for a test of the 5700.00 handle further out. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high. A bull cycle in S&P E-Minis remains intact. The contract has again traded to a fresh cycle high to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6666.25. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6550.28.

- Japan's NIKKEI closed higher by 385.88 pts or +0.87% at 44936.73 and the TOPIX ended 7.34 pts lower or -0.24% at 3087.4.

- Across Europe, Germany's DAX trades higher by 292.87 pts or +1.21% at 24410.52, FTSE 100 higher by 1.95 pts or +0.02% at 9448.56, CAC 40 up 84.15 pts or +1.06% at 8051.87 and Euro Stoxx 50 up 68.66 pts or +1.23% at 5649.87.

- Dow Jones mini down 11 pts or -0.02% at 46712, S&P 500 mini up 10.75 pts or +0.16% at 6772.25, NASDAQ mini up 87.25 pts or +0.35% at 25104.5.

Time: 10:00 BST

COMMODITIES: Recent Pullback for WTI Futures Reinforces Bearish Theme

WTI futures have pulled back from their recent highs. This reinforces a bearish theme and suggests S/T gains are corrective. Initial firm resistance has been defined at $66.42, the Sep 29 high. The key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. The clear reversal lower refocuses attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend. A bull cycle in Gold remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3700.1, the 20-day EMA. A pullback would be considered corrective.

- WTI Crude up $0.07 or +0.11% at $61.82

- Natural Gas down $0.05 or -1.38% at $3.428

- Gold spot up $9.74 or +0.25% at $3873.44

- Copper up $7.8 or +1.6% at $496.05

- Silver up $0.18 or +0.39% at $47.4824

- Platinum up $15.09 or +0.96% at $1580.7

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University | ||

| 03/10/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/10/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/10/2025 | 0645/0845 | * | Industrial Production | |

| 03/10/2025 | 0700/0300 | * | Turkey CPI | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0800/1000 | * | Retail Sales | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/10/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/10/2025 | 0900/1100 | ** | EZ PPI | |

| 03/10/2025 | 0940/1140 | ECB Lagarde Speech At Knot Farewell Symposium | ||

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson | ||

| 03/10/2025 | 2200/1800 | NY Fed's John Williams |