MNI US OPEN - Ueda Hints at December Hike

EXECUTIVE SUMMARY

- UEDA SAYS BOJ WILL MULL PROS AND CONS OF RAISING RATE

- US SAYS UKRAINE TALKS PRODUCTIVE AS WITKOFF HEADS TO RUSSIA

- REEVES REPORTED FOR POSSIBLE "MARKET ABUSE," MINISTERIAL CODE BREACH

- RENEWED DIVERGENCE BETWEEN DE/FR PMIs AND THE REST

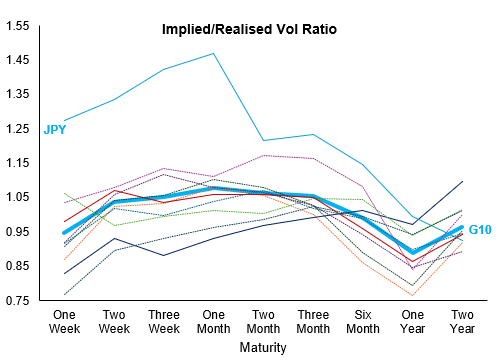

Figure 1: G10 FX vols settle... except for JPY

Source:

NEWS

BOJ (MNI): BOJ Will Mull Pros and Cons of Raising Rate - Ueda

Bank of Japan Governor Kazuo Ueda said on Monday that the BOJ will consider the pros and cons of raising the policy interest rate and make decisions as appropriate at its Dec. 18-19 meeting. “At the MPM, the Bank will examine and discuss economic activity and prices at home and abroad as well as developments in financial and capital markets, including the point I just mentioned, based on various data and information, and will consider the pros and cons of raising the policy interest rate and make decisions as appropriate,” Ueda told business leaders in Nagoya City.

BOJ (BBG): BOJ’s Ueda Says Has Had Good Discussions With Govt

Bank of Japan Governor Kazuo Ueda says that he has had frank, good discussions at meetings with Prime Minister Sanae Takaichi and economic ministers. Wants to keep sufficient communications with the government, Ueda tells reporters in Nagoya, central Japan. Need to watch risk of foreign exchange rates affecting underlying inflation. A weak yen could be a factor to boost inflation via higher import cost.

US/RUSSIA/UKRAINE (BBG): US Says Ukraine Talks Productive as Witkoff Heads to Russia

US and Ukrainian negotiators said they had productive discussions about a framework for a peace deal, but there was no final breakthrough as President Donald Trump continues to push for a truce with Russia. “There’s more work to be done,” Secretary of State Marco Rubio told reporters in Florida after meeting for at least four hours with Ukrainian officials led by National Security and Defense Council Secretary Rustem Umerov. “This is delicate. It’s complicated.”

ECB (BBG): Current Level of ECB Rates Appropriate, Guindos Tells Periodico

European Central Bank Vice President Luis de Guindos indicated he is comfortable with current interest-rate settings, according to an interview in El Periodico newspaper. “The markets are pricing in stability, with no rate increases or decreases in the coming months. What we are saying is that the current level of interest rates is appropriate.”

ECB (BBG): Guindos Says De Cos Was Great Governor, No Lock for Lagarde Job

European Central Bank Vice President Luis de Guindos extolled the virtues of fellow Spaniard Pablo Hernandez de Cos but declined to say if that put him on track to succeed Christine Lagarde as ECB president in two years. “Pablo was an excellent governor — he restored Banco de España’s reputation,” Guindos told the Spanish newspaper El Periódico in an interview published on Monday.

UK (MNI): Reeves Reported for Possible "Market Abuse," Ministerial Code Breach

As expected, the weekend's fiscal headlines reacted to the aftermath of the Budget. The biggest stories were surrounding whether Chancellor Rachel Reeves mis-led the public and financial markets by misrepresenting how much worse the OBR forecasts had made the headrom and how the income tax plans had been changed by updated OBR forecasts that weren't so good. Indeed, she has since been reported to the FCA by Shadow Chancellor Mel Stride of the Conservatives for "possible market abuse". She has also been reported by Reform UK leader Nigel Farage to Sir Magnus Laurie, the PM's Independent Adviser on Ministers' Interests, regarding a potential breach of the ministerial code.

CHINA (MNI): China Export Controls Concerning - European Chamber

MNI (Beijing) China’s export control regime continues to create operational challenges for European companies, according to the European Union Chamber of Commerce in China, citing a survey released Monday that showed 40% of respondents found the export-licence approval process exceeded the official 45-day timeframe. The bottlenecks have disrupted delivery schedules, with 40% of surveyed firms indicating that export-control approvals have added more than two months to delivery times for affected goods, the chamber said.

CHINA (BBG): China Vanke Asks for 12 Months to Pay Bond Under Extension Plan

China Vanke Co., the distressed builder that surprised markets last week when it proposed an unspecified delay in paying a local bond, has now asked holders to wait a year to be made whole, as it faces mounting liquidity pressure amid waning state support. Shenzhen-based Vanke, once the nation’s largest builder by sales, told creditors Monday that it was seeking a one-year delay to pay the 2 billion yuan ($283 million) note originally due on Dec. 15 along with interest, people familiar with the matter said. During the extension period, the 3% coupon would remain unchanged, according to the people, who asked not to be identified discussing private matters.

CHINA (BBG): China Tells Stats Providers to Halt Home Sales Data Publication

Two of China’s private data agencies withheld monthly home sales figures at the government’s behest, people familiar with the matter said, stoking transparency concerns in a critical sector of the world’s second-largest economy. China Real Estate Information Corp. and China Index Academy, which are among the country’s biggest private property data providers, didn’t disclose the combined sales of the nation’s 100 largest developers for November on Sunday.

RBA (MNI EXCLUSIVE): RBA Sees Balanced Risk, Despite Monthly CPI Shock

MNI discusses the RBA's cash rate view. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

INDIA (MNI): USD/INR Teases 90 on NDF Market, RBI Intervention Described as Sporadic

USD/INR rose to a new record high, prompting intervention from the RBI to prevent a further slide in the local currency. However, reports suggest that intervention from the central bank was sporadic, and the price action continues to suggest that authorities are loosening their grip on the currency. Spot rose to a high of 89.78, narrowing the gap to the psychological 90.00 handle. Rupee weakness was more notable in the NDF market where the pair fell just 2 pips shy of 90. The lack of a US-India trade deal and a widening trade deficit remain key rupee headwinds, despite local press continuing to suggest that a trade deal is inching to completion, while portfolio outflows have been cited as a source of weakness on an intraday basis.

THAILAND (BBG): Thai Central Bank Proposes New FX Rules to Ease Pressure on Baht

The Bank of Thailand plans to roll out additional measures to ease appreciation pressure on the baht and tighten oversight of gold-related foreign-exchange transactions after the currency strengthened about 1% over the past week. The local currency’s gains were driven by a weaker US dollar and increased foreign exchange selling from exporters; bond inflows; and gold traders amid a more than 4% jump in global bullion prices, Pimpan Charoenkwan, assistant governor for the central bank’s financial markets, said in a statement on Monday.

DATA

EUROZONE DATA (MNI): Renewed Divergence Between DE/FR PMIs and the Rest

- EUROZONE NOV FINAL MANUF PMI 49.6 (49.7 FLASH 50.0 OCT)

- GERMANY NOV FINAL MANUF PMI 48.2 (48.4 FLASH, 49.6 OCT)

- FRANCE NOV FINAL MANUF PMI 47.8 (47.8 FLASH, 48.8 OCT)

The November manufacturing PMIs highlighted renewed divergence between Germany/France and the rest of the region. Our estimate of the ex-Germany/France manufacturing PMI remained in expansionary territory at 51.5 in November, while the Germany/France manufacturing PMI was revised down to 48.1 (vs 48.2 flash, 49.4 prior). Manufacturing PMI momentum is easing in Germany, France and Spain, with Italy the main exception in November. The report suggests Eurozone core goods inflation pressures remain subdued.

ITALY DATA (MNI): Manufacturing PMI Strongest Since Mar '23, But Employment Still Falling

- ITALY NOV MANUF PMI 50.6 (50.1 FCAST, 49.9 OCT)

The Italian November manufacturing PMI was stronger-than-expected at 50.6 (vs 50.1 cons, 49.9 prior), its highest since March 2023. An improvement in international demand follows on from Friday's Q3 GDP report, where net exports made a positive contribution to sequential growth. There were some continued signs of softness for the consumption outlook though, with the consumer goods sector contracting in November and overall employment falling.

SPAIN DATA (MNI): Manufacturing PMI Still Expansionary But Some Signs of Waning Momentum

- SPAIN NOV MANUF PMI 51.5 (52.3 FCAST, 52.1 OCT)

The Spanish manufacturing PMI has now been in expansionary territory since April. However, alongside the lower-than-expected reading, details of the November report were soft in places, with higher demand in part driven by discounting.

SWITZERLAND DATA (MNI): Solid October Retail Sales

- SWISS OCT RETAIL SALES +0.7% M/M, +2.7% Y/Y (VS +0.5% M/M, +1.8% Y/Y SEP)

Retail sales data underpins the narrative that barring new shocks, the SNB is likely to hold its policy rate at 0% for the foreseeable future. The series started off Q4 on a solid note, at 0.7% M/M in October (0.5% September, revised from 0.6%). Looking at the drivers of the release shows that clothing and footwear stands out positively, at 2.6% M/M (0.4% prior). However, over the last couple of months, none of the main subseries have exhibited a clear directional trend on a M/M basis.

SWEDEN DATA (MNI): Wage and Manufacturing PMI Data Consistent With a Cyclical Recovery

This morning's Swedish data were consistent with the ongoing narrative around an economic recovery. The Riksbank is firmly expected to be on hold at 1.75% for "some time", but today's readings add to the stock of data suggesting medium-term risks to rates are tilted towards hikes. Real wage growth remains positive, which is expected to support household consumption through the end of 2025 and into 2026.

UK DATA (MNI): BOE Credit Data In Line, Continued Pre-Budget Housing Resilience

- UK OCT M4 MONEY SUPPLY -0.2% M/M, +3.5% Y/Y

- UK BOE OCT MORTGAGE APPROVALS 65,018

- UK BOE OCT CONSUMER CREDIT GBP1.12 BLN

- UK BOE OCT SECURED LENDING GBP4.27 BLN

BOE money and credit data for October again printed broadly in line with expectations. New mortgage approvals continue to trend around the historical average. On the whole, the release points to resilience in the housing market in the lead-up to the Budget, and a return to historical norms following frontloading of homebuying in March. New mortgage approvals came in at 65.0k, broadly in line with consensus of 64.5k, and almost exactly in line with the average level since 2016 of 64.9k.

UK NOV FINAL MANUF PMI 50.2 (50.2 FLASH, 49.7 OCT) (MNI)

CHINA DATA (MNI): China November Manufacturing PMI Remains Below 50

MNI (Beijing) China's Manufacturing Purchasing Managers Index rose by 0.2 points to 49.2 in November from October, remaining below the breakeven 50 mark for the eighth month, data from the National Bureau of Statistics showed Sunday. Both the production and new orders sub-indices were up by 0.3 and 0.4 points to 50.0 and 49.2.

CHINA DATA (MNI): Nov RatingDog China Mfg. PMI Falls Below 50 Mark

- CHINA NOV RATINGDOG MANUFACTURING PMI 49.9 VS 50.6 IN OCT

MNI (Beijing) China's RatingDog manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 49.9 in November, down from October's 50.6, falling into the contraction zone below the 50 mark after expanding for three months, the publisher said on Monday. Growth of production sub-index came to a halt as new orders nearly stalled. A renewed rise in new orders overseas failed to reverse the sluggish state of the manufacturing sector, the publisher said.

RATINGS: Affirmations on Friday

Sovereign rating reviews of note from after hours on Friday include:

- S&P affirmed Latvia at A; Outlook Stable

- S&P affirmed Lithuania at A; Outlook Stable

- Morningstar DBRS confirmed Germany at AAA, Stable Trend

- Morningstar DBRS confirmed Spain at A (high), Stable Trend

FOREX: USDJPY Stabilizes Above 20-day EMA; Focus Shifts to US Data

- USDJPY stabilises just above the daily low of 155.26, finding support into the 20-day EMA. Renewed pressure on the pair here would expose the 50-day EMA at 153.06 for direction - a level that could come into play should the pick-up in volumes at the NY crossover extend the hawkish JPY move.

- Ueda's comments overnight (namely his statement that raising rates should be seen as easing off the accelerator, rather than applying the brakes) keep December BoJ hike speculation in play, evident in market pricing for a hike rising to ~80% - up from around ~60% Friday. Perhaps notably, Ueda has also scheduled a speech to take place on December 25th - one week after the BoJ decision.

- With no further BoJ comments scheduled for Monday, focus shifts to the USD leg of the trade: ISM Manufacturing will be the key datapoint today as private sector data remains more timely than the still-catching-up government stats. The USD Index remains inside the S/T downtrend posted off the late November high (100.395), with support expected into the 98.992-99.063 area, which could contain a further decline in USDJPY.

EGBS: Confluence of Factors Applying Pressure to Bunds, Bear Trigger in Sight

The combination of higher oil prices, impending EU-bond supply and hawkish JGB spillover overnight has weighed on major EGB futures this morning. Bunds are -30 ticks at 128.58, narrowing the gap to the short-term bear trigger at 128.37 (Nov 20 low). Clearance of this level would resume the bear leg and open 128.25, the Oct 7 low.

- A reminder that futures volumes are likely to be impacted quarterly roll activity this week.

- The German curve has bear steepened, with 5s30s up 0.5bps to 104bps. Whether the spread can test the Sep 3 year-to-date high of 111bps may depend on the details of Germany’s 2026 issuance plan – usually released in the middle of December. 10-year Bund yields are back above 2.70%, up 3bps today.

- EGB spreads vs. Bunds little changed to ~1bp wider with headwinds for risk sentiment driving the initial widening seen early this week.

- The EU will hold its final EU-bond auction of 2025 at 1030GMT, with up to E2bln of the 0% Oct-28 EU-bond, up to E2bln of the 2.75% Dec-32 EU-bond and up to E1bln of the 0.45% Jul-41 EU-bond on offer.

- The November manufacturing PMIs highlighted renewed divergence between Germany/France and the rest of the region, but were not market movers. Eurozone-wide November flash inflation is due tomorrow.

GILTS: Bear Steepening on Global Cues

Gilts hold lower, with hawkish BoJ comments and firmer oil prices weighing on wider core global FI markets.

- Political pressure for Chancellor Reeves also noted in the wake of the Budget (via accusations that she misled the Cabinet, parliament and financial markets in the run up to the Budget).

- Gilt futures as low as 91.16. First support not seen until the November 26 low (90.53). A break there would negate some of the recent bullish momentum.

- Yields 2-6bp higher, curve steeper.

- 10+-Year yields have failed to retest October/early November lows, despite the post-Budget rally in UK paper. This morning’s sell off leaves 10s 6bp above post-Budget lows, while 30s are 9bp above last week’s base.

- The backloaded nature of the fiscal tightening outlined in the Budget, coupled with some questions surrounding the accuracy of the fiscal headroom calculations, could leave gilts susceptible to steepening pressure. This could be particularly true in times when wider core global FI markets are coming under pressure.

- Gilt/Bunds ~175bp, sticking within the multi-week range.

- Front end still pricing over 80% odds of a BoE rate cut later this month.

- Dhingra, the most dovish member of the BoE’s MPC, will give a keynote speech at the UK Trade Policy Observatory’s annual conference (15:30 London). We expect Dhingra to vote for a cut later this month and she should reaffirm her dovish credentials later today, if she does touch on monetary policy.

- Elsewhere, the DMO will conduct its consultation with investors and GEMMS this afternoon.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.748 | -22.0 |

Feb-26 | 3.684 | -28.5 |

Mar-26 | 3.599 | -37.0 |

Apr-26 | 3.499 | -47.0 |

Jun-26 | 3.451 | -51.8 |

Jul-26 | 3.388 | -58.0 |

Sep-26 | 3.369 | -60.0 |

EQUITIES: Move Lower for Eurostoxx Futures Last Week Undermines a Bearish Theme

The move higher in Eurostoxx 50 futures last week undermines a recent bearish theme and the contract is holding on to most of its gains. Price has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5691.30 and 5742.40, Fibonacci retracement points. For bears, a reversal lower would instead expose the key S/T support and bear trigger at 5475.00, the Nov 21 low. S&P E-Minis are holding on to the bulk of their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed lower by 950.63 pts or -1.89% at 49303.28 and the TOPIX ended 40.11 pts lower or -1.19% at 3338.33.

- Elsewhere, in China the SHANGHAI closed higher by 25.41 pts or +0.65% at 3914.006 and the HANG SENG ended 174.37 pts higher or +0.67% at 26033.26.

- Across Europe, Germany's DAX trades lower by 203.95 pts or -0.86% at 23631.47, FTSE 100 lower by 7.46 pts or -0.08% at 9712.96, CAC 40 down 29.62 pts or -0.36% at 8093.09 and Euro Stoxx 50 down 14.44 pts or -0.25% at 5653.73.

- Dow Jones mini down 211 pts or -0.44% at 47532, S&P 500 mini down 41.25 pts or -0.6% at 6818.5, NASDAQ mini down 199.5 pts or -0.78% at 25282.75.

Time: 10:00 GMT

COMMODITIES: Trend Condition in Gold Remains Bullish, Key Resistance at $4381.50

Recent weakness in WTI futures highlights a bearish theme. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. The contract has recovered from its latest low, resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. Note that the recovery since Oct 28 signals the end of the corrective cycle. Key support to watch lies at the 50-day EMA, at $3991.7. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $1.2 or +2.05% at $59.75

- Natural Gas down $0.07 or -1.53% at $4.773

- Gold spot up $9.12 or +0.22% at $4247.49

- Copper up $1.6 or +0.3% at $528.8

- Silver up $0.82 or +1.45% at $57.299

- Platinum up $10.19 or +0.61% at $1680.77

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 01/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 01/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/12/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 01/12/2025 | 1530/1530 | DMO to hold FQ4 consultations with investors / GEMMs | ||

| 01/12/2025 | 1530/1530 | BOE Dhingra Keynote at UK Trade Policy Observatory | ||

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/12/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 02/12/2025 | 0030/1130 | * | Building Approvals | |

| 02/12/2025 | 0030/1130 | Balance of Payments: Current Account | ||

| 01/12/2025 | 0100/2000 | Fed Chair Jerome Powell | ||

| 02/12/2025 | 0700/0700 | BOE Financial Stability Report | ||

| 02/12/2025 | 0745/0845 | Budget Balance | ||

| 02/12/2025 | 0900/1000 | Unemployment | ||

| 02/12/2025 | 1000/1100 | ** | EZ Unemployment | |

| 02/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 02/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 02/12/2025 | 1500/1000 | Fed Vice Chair Michelle Bowman | ||

| 03/12/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 03/12/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |