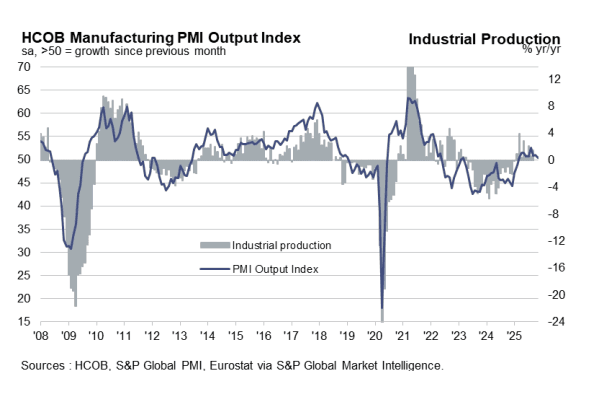

EUROZONE DATA: Nov Manuf PMI: Renewed Divergence Between DE/FR and The Rest

The November manufacturing PMIs highlighted renewed divergence between Germany/France and the rest of the region. Our estimate of the ex-Germany/France manufacturing PMI remained in expansionary territory at 51.5 in November, while the Germany/France manufacturing PMI was revised down to 48.1 (vs 48.2 flash, 49.4 prior).

- MNI: EUROZONE NOV FINAL MANUF PMI 49.6 (49.7 FLASH 50.0 OCT)

Manufacturing PMI momentum is easing in Germany, France and Spain, with Italy the main exception in November. The report suggests Eurozone core goods inflation pressures remain subdued.

Key notes from the Eurozone-wide release:

- “After stabilising in October, the volume of new work received by eurozone manufacturers decreased, signalling fresh headwinds to demand….Sales to overseas markets remained a challenge for eurozone factories, latest survey data showed, with new export orders falling for a fifth month running.”

- “Manufacturing output growth was sustained, marking nine successive months of expansion. The rate of increase slowed, however, to a pace that was only marginal and the weakest across the current upturn.”

- “Prices charged for euro area goods fell for the sixth time in the past seven months.”

- “Looking ahead, eurozone manufacturers reported greater optimism towards the next 12 months. In fact, the overall level of positive sentiment rose above its historical average (since 2012) to its highest since June”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.670 @ 16:16 GMT Oct 31

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.375 @ 16:13 GMT Oct 31

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course Wednesday on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

FED: Gov Waller: Still Advocating For A December Rate Cut

Gov Waller, one of the FOMC's more prominent doves, makes clear in an appearance on Fox Business that he supports a follow-up rate cut in December. He makes reference to Chair Powell's press conference comment that the Fed could skip a cut at the December meeting due in part to a lack of official government data during the federal shutdown (Powell: “what do you do if you are driving in the fog? You slow down").

- Waller says today: "Right now, we know that the labor market has been weak... We know inflation is going to come back down. Inflation expectations are anchored, and in that world, the standard of central bank wisdom is to look through it and proceed with worrying about the labor market. So in my view, we should just look at what the data is telling us and proceed on policy that way.... So this is why I'm still advocating that we cut policy rates in December, because that's what all the data is telling me to do. The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and ... the right thing to do with policy is to continue cutting."

- This is of particular interest since he appeared to suggest he would have a more cautious outlook on further easing after cutting in October.