SWEDEN: Wage and Manufacturing PMI Data Consistent With A Cyclical Recovery

This morning’s Swedish data were consistent with the ongoing narrative around an economic recovery. The Riksbank is firmly expected to be on hold at 1.75% for "some time", but today's readings add to the stock of data suggesting medium-term risks to rates are tilted towards hikes.

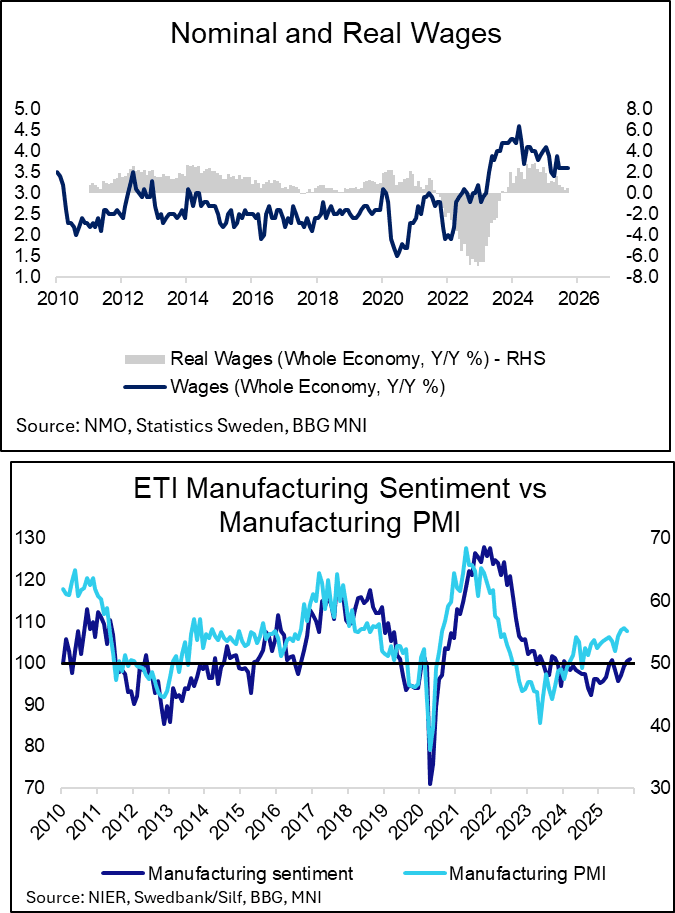

Real wage growth remains positive, which is expected to support household consumption through the end of 2025 and into 2026.

- Whole-economy nominal wage growth was estimated at 3.2% Y/Y in September, while the National Mediation Office’s (NMO) adjustment to account for retroactive payments predicted growth of 3.6% Y/Y.

- This implied whole-economy real wage growth of 0.5% Y/Y (vs 0.4% prior).

- Private sector wages were estimated at 3.3% Y/Y (vs 3.3% prior), with the NMO’s adjustment predicting growth of 3.5% Y/Y (vs 3.6% prior).

- In the public sector, the NMO’s adjustment played a larger role, with wage growth predicted at 3.9% Y/Y based on an original estimate of 3.2% Y/Y.

The November manufacturing PMI remained comfortably in expansionary territory at 54.6 (vs 55.0 prior). The three analyst estimates submitted to Bloomberg were 55.0, 55.1 and 55.5.

- New orders rose back to 56.7 (vs 55.8 in Oct, 57.7 in Sept), while production eased to 57.6 (vs 60.5 prior). Employment rose to 51.6 (vs 50.9 prior), while future production remained elevated at 66.7 (vs 70.1 prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.670 @ 16:16 GMT Oct 31

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.375 @ 16:13 GMT Oct 31

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course Wednesday on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

FED: Gov Waller: Still Advocating For A December Rate Cut

Gov Waller, one of the FOMC's more prominent doves, makes clear in an appearance on Fox Business that he supports a follow-up rate cut in December. He makes reference to Chair Powell's press conference comment that the Fed could skip a cut at the December meeting due in part to a lack of official government data during the federal shutdown (Powell: “what do you do if you are driving in the fog? You slow down").

- Waller says today: "Right now, we know that the labor market has been weak... We know inflation is going to come back down. Inflation expectations are anchored, and in that world, the standard of central bank wisdom is to look through it and proceed with worrying about the labor market. So in my view, we should just look at what the data is telling us and proceed on policy that way.... So this is why I'm still advocating that we cut policy rates in December, because that's what all the data is telling me to do. The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and ... the right thing to do with policy is to continue cutting."

- This is of particular interest since he appeared to suggest he would have a more cautious outlook on further easing after cutting in October.