MNI US OPEN - Trump Says Not Necessary to Fire Powell

EXECUTIVE SUMMARY

- TRUMP SAYS NOT NECESSARY TO FIRE POWELL AFTER GETTING FED TOUR

- BOJ IS SAID TO SEE POTENTIAL RATE HIKE ENVIRONMENT THIS YEAR

- UNSC TO DISCUSS THAI-CAMBODIA CLASH, BANGKOK REJECTS MEDIATION OFFERS

- UK RETAIL SALES WEAKER-THAN-EXPECTED IN JUNE DESPITE HOT WEATHER BOOST

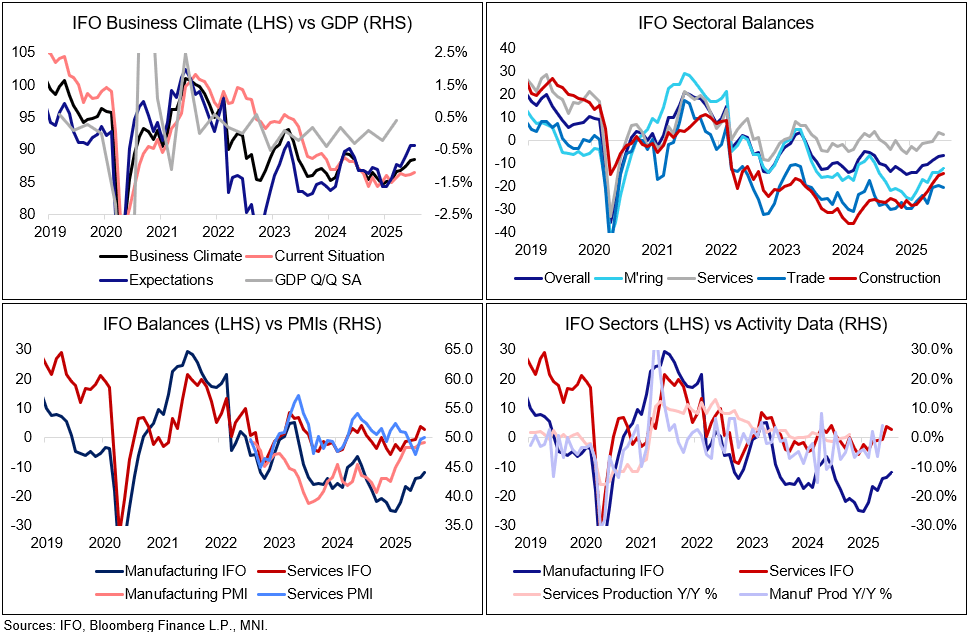

Figure 1: German IFO rises gradually, led by manufacturing

NEWS

US (BBG): Trump Says Not Necessary to Fire Powell After Getting Fed Tour

Donald Trump downplayed his clash with Federal Reserve Chairman Jerome Powell over cost overruns during a tour of the central bank’s renovation project on Thursday, making it clear that he saw the issue of lower interest rates as a more pressing concern. After a tour that saw Trump and Powell publicly trade barbs over the cost of the project, Trump maintained there was “no tension” with the Fed chief and indicated that problems with the project probably weren’t reason enough to fire the central bank head. “To do that is a big move, and I just don’t think it’s necessary,” Trump told reporters.

US/S.KOREA (MNI): ROK Officials to Meet w/USTR Greer as They Push for Trade Deal

South Korea's top trade negotiators will meet with USTR Jamieson Greer today, as they push to secure a trade deal to avert a 25% tariff rate on August 1, per Reuters. Comes after the cancellation of yesterday's high-profile '2+2' finance and trade meeting with Treasury Secretary Scott Bessent. South Korea's presidential office said that US Commerce Secretary Howard Lutnick "showed interest" in a "mutually beneficial plan" proposed by Seoul yesterday, per Yonhap.

US/UK (FT): Keir Starmer to Press Donald Trump Over Deal to Cut Tariffs on UK Steel Imports

Donald Trump arrives in Scotland on Friday for a five-day golf trip, during which Sir Keir Starmer will lobby the US president to accelerate a final deal to cut tariffs on British steel. The UK prime minister is expected to meet Trump on Monday and will also use the encounter to press the case for building closer ties, including cutting tariffs on Scotch whisky, according to UK officials.

BOJ (BBG): BOJ Is Said to See Potential Rate Hike Environment This Year

Bank of Japan officials see the possibility of mulling another interest rate hike this year after the US and Japan struck a trade deal this week, according to people familiar with the matter. The officials view the deal as reducing a key source of uncertainty for Japan’s economy and businesses, allowing the central bank to focus on monitoring the tariffs’ actual impact in incoming economic data, the people said. With more clarity over trade, the central bank may be able to make a decision on policy at an earlier stage, after parsing data and information from companies.

ECB (BBG): ECB’s Kazaks Sees Little Need for Further Interest-Rate Cuts

There’s little reason for the European Central Bank to lower interest rates further unless the economy suffers a major blow, according to Governing Council member Martins Kazaks. With inflation at 2% and the euro zone largely performing in line with the ECB’s latest forecasts, the grounds for a cut in September — as expected by a majority of economists before this week’s meeting — aren’t obvious, the Latvian central-bank chief said.

ECB (MNI): Rehn's Post Decision Comments Still Screen Dovish

Bank of Finland Governor Rehn's full post-ECB decision comments are in this blog. Overall, while he backs an interest rate pause for now, his bias still tilts towards easier monetary policy. He references the downside risks to inflation, not upside risks: "inflation is expected to slow down to well below 2 percent by the end of the year before it is forecast to return to the target level by the end of 2026. The drop is primarily due to lower energy prices than the previous year, so it is expected to be only temporary, but we are monitoring this development particularly closely"

MIDEAST (MNI): Gaza Ceasefire Talk to Resume Next Week - Al Qahera

Reuters reports, per sources cited by Egypt's Al Qahera News that, "Gaza ceasefire talks are expected to resume next week following Israel's review of Hamas' response." The report comes after talks in Qatar appeared to stall yesterday following a decision by Israel and the US to recall negotiators, citing a "lack of desire" on behalf of Hamas to reach a cease-fire. President Donald Trump's Special Envoy, Steve Witkoff, said in a statement: "We have decided to bring our team home from Doha for consultations after the latest response from Hamas, which clearly shows a lack of desire to reach a ceasefire in Gaza We will now consider alternative options to bring the hostages home... We are resolute in seeking an end to this conflict..."

JAPAN (MNI): Ishiba Opponents Secure Required Signatures to Convene LDP Meeting

Jiji Press reports that opponents of Prime Minister Shigeru Ishiba have secured the requisite signatures from "one-third of the Diet members" to convene a joint meeting of upper and lower house lawmakers from the governing conservative Liberal Democratic Party (LDP). Opposition to Ishiba from within the LDP has reached a near-breaking point after the governing coalition lost its majority in the upper chamber of the Diet in the 20 July House of Councillors election. The meeting will take place on Monday, 28 July. FNN reports that "former Minister of Economy, Trade and Industry [Sanae] Takaichi and 14 members of the [former PM Taro] Aso faction have signed the petition."

THAILAND/CAMBODIA (MNI): UNSC to Discuss Thai-Cambodia Clash, Bangkok Rejects Mediation Offers

The UN Security Council will hold an emergency meeting on the ongoing clashes between Thailand and Cambodia at 20:00BST/15:00EDT, with both countries' envoys expected to attend, after Bangkok rejected of third-party mediation and insisted that it was only willing to accept bilateral talks. Thai Foreign Ministry spokesperson told Reuters that Thailand has turned down offers from the US, China and Malaysia (in its capacity as the current chair of ASEAN) to help facilitate dialogue with Cambodia.

PHILIPPINES (BBG): Philippine Court Says Duterte Impeachment Unconstitutional

The Philippines’ Supreme Court on Friday said the impeachment complaint against Vice President Sara Duterte is unconstitutional. The top court said the complaint didn’t comply with the constitutional rule that only one impeachment proceeding may be initiated against the same official within one year. The vice president was impeached in February by the House of Representatives on accusations she plotted to assassinate President Ferdinand Marcos Jr. and misused public funds. She denies all allegations of wrongdoing.

DATA

UK DATA (MNI): June Retail Sales Weaker-Than-Expected Despite Hot Weather Boost

- UK JUN RETAIL SALES +0.9% M/M, +1.7% Y/Y

- UK JUN RETAIL SALES EX-FUEL +0.6% M/M, +1.8% Y/Y

UK retail sales were softer-than-expected for the second consecutive month in June, with last month's weak reading also revised a tenth lower on a sequential basis. There has been a bit of early pressure on GBP FX following the release, but EURGBP is still only up 0.12% at typing, testing yesterday's 0.8710 high. The retail sales data is often too volatile to garner much attention from the MPC, but readings since April are consistent with increasing consumer caution against a backdrop of still-elevated inflation and expectations for more fiscal tightening in the Autumn.

UK JUL GFK CONSUMER CONFIDENCE INDEX -19 (MNI)

GERMANY DATA (MNI): IFO Rises Gradually, Led by Manufacturing

- GERMANY JUL IFO BUSINESS CLIMATE INDEX 88.6

Germany's IFO Business Climate Index continued to rise in July, to 88.6 (its highest since June 2024, vs 88.4 prior), but remained below expectations of 89.0 - as yesterday's flash PMI's also did. Across sectors, manufacturing strengthened (also to its highest reading since June 2024) but services wasn't able to consolidate last month's gains in full. Companies' current assessment at 86.5 (vs 86.7 cons; 86.2 prior) and expectations at 90.7 (vs 91.1 cons; 90.6 prior) both rose but remained below expectations.

FRANCE DATA (MNI): Consumer Confidence Rises Slightly, But Details Still Weak

- FRANCE JUL CONSUMER SENTIMENT 89

French consumer sentiment index ticked up slightly to 88.6 in July (rounded cons 88, prior 88.4), but still remains below its long-term average of 100. Consumers' view of the general economic situation continued to deteriorate, with the backward-looking component softening to -70.4 (vs -69.6 prior) and the forward-looking 12-month ahead component falling for the fifth consecutive month to -60.9 (vs -60.0 prior). Against a backdrop of continued domestic political and fiscal uncertainty, these trends are unsurprising.

ITALY DATA (MNI): Consumer Confidence Rebound Since April More Notable Than Businesses

Italian consumer confidence has seen a more notable rebound from the April 2025 lows compared to business confidence. Consumer confidence was 97.2 (vs 95.9 cons, 96.1 prior), the highest since February and still above the 91.6 average between 2000-2019. They key question will be whether this translates into better household consumption growth readings - real consumption rose 0.2% Q/Q in Q1 and Q4. Flash Q2 GDP is due next week, but won't contain a quantitative expenditure breakdown.

SWEDEN DATA (MNI): June LFS Data Consistent With Steady But Subdued Labour Market

- SWEDEN JUN UNEMPLOYMENT 9.4%

The June LFS labour market data appears consistent with steady but subdued conditions. When taken alongside a drift higher in the PES unemployment claims rate and a softening in the Economic Tendency Indicator's expected employment metric, there is certainly some justification for market expectations of one more 25bp Riksbank cut at some point this year. The pullback in the seasonally adjusted LFS unemployment rate to 8.3% (vs 8.8% cons, 9.0% prior) was mostly due to a fall in the participation rate to

75.2% (vs 75.8% prior). However, the employment rate did tick up a touch to 69.0% from 68.9%.

JAPAN JULY TOKYO CORE CPI +2.9% Y/Y; JUNE +3.1% (MNI)

JAPAN JULY TOKYO CORE-CORE CPI +3.1% Y/Y; JUNE +3.1% (MNI)

JAPAN JUNE SERVICES PPI +3.2% Y/Y; MAY REV +3.4% (MNI)

FOREX: Unusually Strong Volumes for a Friday, JPY Will Need More Rates Impetus

The rate-driven demand for USD/JPY has the pair comfortably through 147.52 resistance but further relief for the longer-end of the Japanese curve will likely be needed to tip prices through Y148 and anywhere closer to 149.19. The sensitivity to the long-end has firmed this week and raises the focus on 10y, 30y JGB auctions at the beginning of August (conveniently the week after the July Fed decision). Markets have shrugged off overnight reports that the BoJ are said to see potential rate hike environment in 2025 - which sits broadly inline with market pricing.

- GBP/USD trading back below broken uptrendline support drawn off the January low is a by-product of this USD demand - particularly as today's retail sales firms the focus on the August 7th BoE (at which a 25bps rate cut is effectively fully priced). The rate has oscillated either side of this trend (today at 1.3511). June retail sales came in notably below expectations, at 0.6% on the month vs. Exp. 1.2%.

- This makes for a decent start to the session for FX futures volumes: EUR, JPY and GBP futures are all seeing above-average activity - particularly for a Friday.

- Optionality today sees $600mln interest across Y147.75-85 strikes in USD/JPY, E1.7bln at $1.1740-50 in EUR/USD, while the rallies in both EUR/GBP and USD/CAD bring sizeable strikes at 0.8725-50 and 1.3700-20 into play (E892mln and $1.2bln respectively).

- Focus for the duration of Friday trade turns to the Kansas City Fed Services data and any post-decision commentary from members of the ECB governing council after yesterday's press conference leaned hawkish and suggested scant opportunity for further rate cuts this year. The Fed remain inside their pre-meeting media blackout period.

EGBS: Bund Futures Off Lows But Hawkish ECB/BoJ Undertones Still Felt

Bund futures have moved away from session lows, with this morning’s sharp selloff in response to a hawkish BOJ sources piece and yesterday’s ECB press conference taking a breather. Bunds are -56 ticks at 129.02, but have pierced key support of 129.08 (July 14 low). The 129.00 handle marks a key area of support and a clear break of it would represent an important bearish development.

- 10-year Bund yields are up 5bps today at 2.753%, having pierced the March 31 high of 2.744%. The psychological 2.800% will be the next area of focus.

- The German curve has bear steepened, with Schatz yields up 3bps and 5- through 30-year yields between 4.5-6bps higher.

- Relatively contained moves in 10-year EGB spreads to Bunds, with early widening fading as European equities bounce from lows. The 10-year BTP/Bund spread is 0.5bps wider at 85.5bps.

- The balance of this morning’s ECBspeak has been mixed. Kazaks and Simkus have struck cautious tones (in line with the signals from Lagarde’s presser), while Rehn and Villeroy have had a more dovish feel.

- This morning’s heavy regional data calendar has generally not been market moving. The German July IFO survey was slightly weaker-than-expected.

GILTS: Holding Lower, Futures and Yields Respect Recent Ranges

Gilts outperform Bunds following softer-than-expected retail sales data, but ultimately trade lower on the day given hawkish cues from abroad (namely source reports and rhetoric re: the BoJ & ECB).

- Futures remain within yesterday’s range, registering a fresh session low at 91.23 in recent trade.

- Initial support at yesterday’s base (91.18), which protects the bear trigger at the July 18 low (91.08).

- Yields 3-4bp higher, curve flatter. Pre-existing month-to-date highs intact across major benchmarks.

- 2s10s and 5s30s don’t stray too far from 75bp & 140bp, respectively, after spill over from yesterday’s ECB decision promoted some flattening yesterday afternoon.

- 10-Year gilt/Bund spread further away from the 200bp marker after failure to close above the round number in recent sessions.

- Spread last 2bp tighter at ~190bp, off session lows.

- GBP STIRs generally a literally more hawkish on the day given influence from the long end, but retail sales means that pricing doesn’t stray too far from 50bp of cuts through year-end (just under 90% odds of a cut showing for August, with 47bp of easing priced through year-end). Pre-existing July lows in SFIZ5 & Z6 are untouched.

- Little of note on the UK calendar for the remainder of the day, which leaves focus on macro matters and spill over from wider global markets.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.993 | -22.4 |

Sep-25 | 3.957 | -26.0 |

Nov-25 | 3.804 | -41.3 |

Dec-25 | 3.747 | -47.0 |

Feb-26 | 3.636 | -58.1 |

Mar-26 | 3.606 | -61.1 |

EQUITIES: E-Mini S&P Climbs to Fresh Cycle Highs

The trend condition in Eurostoxx 50 futures remains bullish and short-term weakness for now, appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains would refocus attention on key resistance and the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00. S&P E-Minis have traded to fresh cycle highs this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6142.04. Support at the 20-day EMA is at 6289.07.

- Japan's NIKKEI closed lower by 370.11 pts or -0.88% at 41456.23 and the TOPIX ended 25.69 pts lower or -0.86% at 2951.86.

- Elsewhere, in China the SHANGHAI closed lower by 12.072 pts or -0.33% at 3593.655 and the HANG SENG ended 278.83 pts lower or -1.09% at 25388.35.

- Across Europe, Germany's DAX trades lower by 180.95 pts or -0.74% at 24114.68, FTSE 100 lower by 32.05 pts or -0.35% at 9106.36, CAC 40 up 7.45 pts or +0.1% at 7826.49 and Euro Stoxx 50 down 18.19 pts or -0.34% at 5337.15.

- Dow Jones mini up 61 pts or +0.14% at 44960, S&P 500 mini up 6.25 pts or +0.1% at 6407.75, NASDAQ mini up 3 pts or +0.01% at 23379.75.

Time 10:00 BST

COMMODITIES: Gold's Short-Term Weakness Corrective, Bull Cycle Still Intact

A bearish theme in WTI futures remains intact and the shallow recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.75. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. On the upside, initial resistance to watch is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range. Gold has pulled back from Tuesday’s high. Short-term weakness is considered corrective and a bull cycle that started Jun 30 remains intact. Resistance at $3395.1, the Jun 23 high, has recently been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend. An initial firm support to watch is 3282.8, the Jul 9 low.

- WTI Crude up $0.44 or +0.67% at $66.45

- Natural Gas up $0.01 or +0.29% at $3.103

- Gold spot down $23.73 or -0.7% at $3345.84

- Copper up $2.8 or +0.48% at $583.3

- Silver down $0.21 or -0.55% at $38.8555

- Platinum down $22.12 or -1.56% at $1392.59

Time 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |