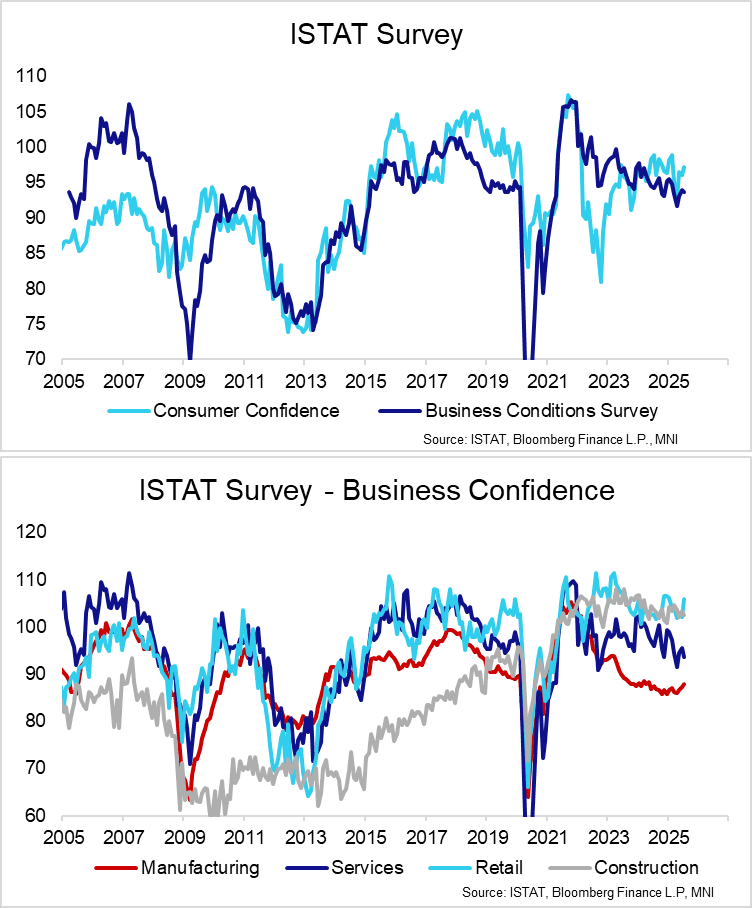

ITALY DATA: Consumer Confidence Rebound Since April More Notable Than Businesses

Italian consumer confidence has seen a more notable rebound from the April 2025 lows compared to business confidence. Consumer confidence was 97.2 (vs 95.9 cons, 96.1 prior), the highest since February and still above the 91.6 average between 2000-2019. They key question will be whether this translates into better household consumption growth readings - real consumption rose 0.2% Q/Q in Q1 and Q4. Flash Q2 GDP is due next week, but won’t contain a quantitative expenditure breakdown.

- The rise in consumer confidence was driven by the personal economic climate subindex (96.9 vs 94.8 prior). The general economic climate index fell back to 98.2 (vs 99.6 June, 97.5 May).

- Business confidence was 93.6 (vs 93.9 prior). This was driven by a fall in services sentiment to 93.7 (vs 95.5 prior), with construction also falling to 102.4 (vs 103.4 prior).

- Manufacturing confidence was 87.8 (vs 87.5 cons, 87.3 prior). Domestic orders and 3-month ahead production were behind the slight increase.

- Retail sentiment picked up to 105.8 (vs 102.0 prior), the highest since January.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWAPS: Long End German Spread Outperformance

Outperformance in the long end of the German swap curve (30s) with yesterday’s sell off in 30-Year spreads now completely reversed (both in conventional swap spreads and ASWs), as the impact of the DFA’s Q3 funding plan and accompanying commentary is unwound (some of the bearish details initially caught some off guard).

- Note that long end spread widening remains evident even as 30-Year yields move off session lows.

- 10-Year Bund yields failed to break below 2.50% during this morning’s rally.

- Commerzbank recommend using any relief rally “in Bunds as a selling opportunity today as supply prospects sink in”.

- Further out, they note that “given the revised Q3 calendar and our expectation for the Q4 adjustment, we now expect record gross Bund issuance of EUR293bln (from EUR265bln at the beginning of the year), which corresponds to a net issuance volume of EUR110bln”.

GREECE T-BILL AUCTION RESULTS: 26-week GTB

| Type | 26-week GTB |

| Maturity | Dec 29, 2025 |

| Amount | E500mln |

| Target | E500mln |

| Previous | E500mln |

| Avg yield | 1.75% |

| Previous | 1.74% |

| Bid-to-cover | 2.12x |

| Previous | 1.91x |

| Previous date | May 28, 2025 |

EUROZONE DATA: Indeed Wage Tracker Eases In May; Consistent With ECB Tracker

The May Indeed wage tracker, released yesterday, eased to 2.5% Y/Y (vs 3.2% prior) for the lowest rate since late 2021. The 3mma Y/Y rate was steady at 3.0%. Overall, the message from Indeed remains broadly consistent with the ECB’s forward looking wage tracker.

- Wages for posted jobs in Germany eased to 3.3% Y/Y (vs 4.6% prior), with the 3mma rate steady at 3.8%.

- In France, which makes up a significant proportion of total observations in the Euro-area wide tracker, posted pay growth was unchanged at 2.0% Y/Y (3mma also unchanged at 1.9%).

- Spain and Italy have much smaller sample sizes, which limits the signal from the tracker. Italian job posting pay growth was supposedly 0.0% Y/Y (!) in May, with Spanish growth easing to 2.9% Y/Y (vs 3.3% prior).