MNI ECB Review: Some Disinflationary Angles Downplayed

Feb-06 15:04By: Chris Harrison

EurozoneChristine Lagarde

Hidden PDF

Executive Summary

- The ECB again left its three key rates unchanged as fully expected, with the deposit rate at 2.0% in the middle of its estimated neutral range.

- The decision statement offered no surprises: the economy is resilient in a challenging global environment whilst it repeated a data-dependent and meeting-by-meeting stance.

- President Lagarde reaffirmed that the ECB is in a “good place”, while noting that “we are in a broadly balanced situation when it comes to the risk assessment”.

- There wasn't any material endorsement of dovish narratives related to geopolitical uncertainty and the exchange rate, helping Euribor futures pull away from post-decision highs but moves were contained.

- She also downplayed the soft January HICP flash release and made comments that could be interpreted as a subtle critique of Eurosystem forecasts.

- Lagarde hinted at an announcement in the coming days on repo lines for other national central banks outside the euro area and outside Europe.

- There was little net change in the OIS-dated rate path for 2026 across the broad suite of communications, with 6bp of cuts priced to September, but that was despite US rates rallying on a series of weak labour data releases and broader risk-off around the decision.

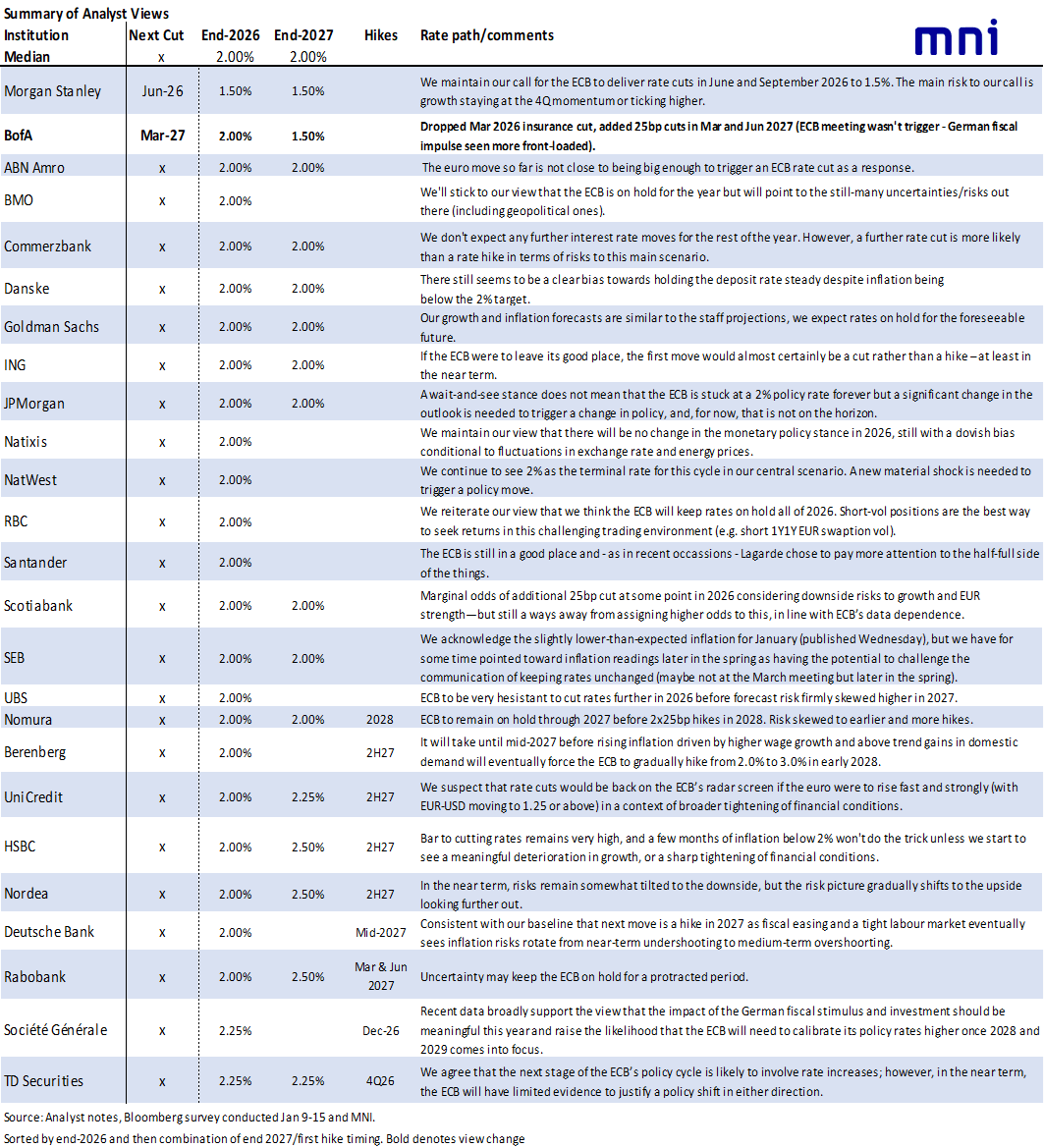

- There are still many analysts who expect rates to remain at 2% throughout both 2026 and 2027. Of those expecting hikes, the majority eye the mid to the second half of 2027 whilst only BofA and Morgan Stanley expect cuts.