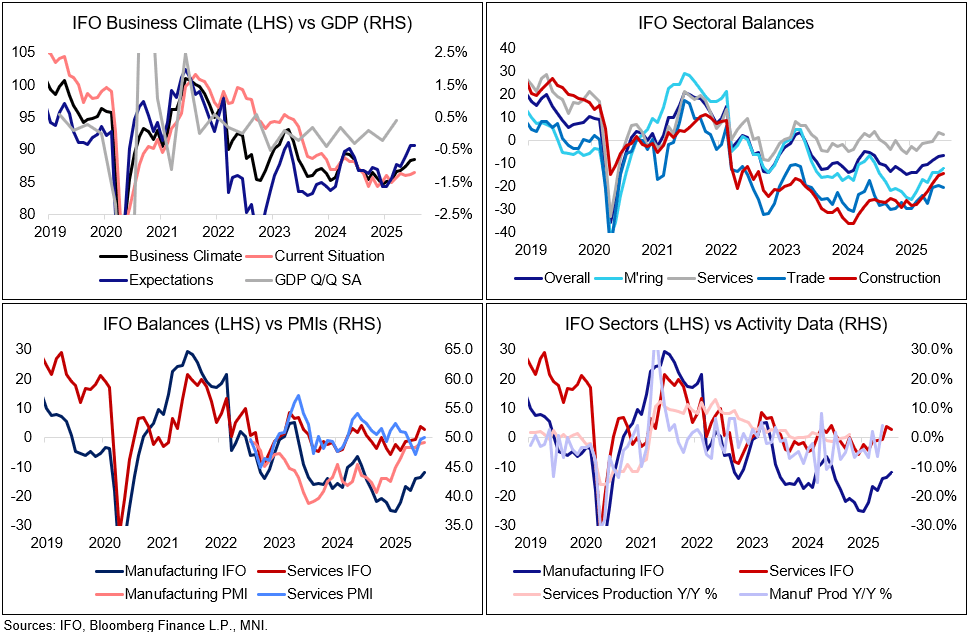

GERMAN DATA: IFO Rises Gradually, Led By Manufacturing

Germany's IFO Business Climate Index continued to rise in July, to 88.6 (its highest since June 2024, vs 88.4 prior), but remained below expectations of 89.0 - as yesterday's flash PMI's also did. Across sectors, manufacturing strengthened (also to its highest reading since June 2024) but services wasn't able to consolidate last month's gains in full.

- Companies' current assessment at 86.5 (vs 86.7 cons; 86.2 prior) and expectations at 90.7 (vs 91.1 cons; 90.6 prior) both rose but remained below expectations.

- Across sectors:

- Manufacturing: "The index went up. Companies assessed their current situation as noticeably better. Their expectations also brightened further. However, incoming orders still lack momentum. Capacity utilization rose only slightly from 77.0 to 77.2 percent."

- Services: "The business climate deteriorated. Current business activity was assessed less favorably, while expectations were also revised slightly downward. IT service providers suffered a setback. By contrast, the transport and logistics sector showed a positive development. Here, the business climate improved noticeably."

- Trade: "The index weakened somewhat due to more pessimistic expectations. Although the current situation improved slightly, it remained unsatisfactory."

- Construction: "the index rose again. Both assessments of the current situation and expectations improved. Nevertheless, a lack of orders remains a major problem."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDNZD: Westpac Recommend Short Position

Westpac recommend short AUD/NZD, targeting a move to the 1.0650- 1.0700 area, with a tight trailing stop at 1.0815.

- They believe that “momentum from the negative reaction to today’s monthly Australian CPI data could persist during the next few days. The RBA’s stated ambition is to proceed in a “cautious and predictable” manner. But understandably, the 8 July RBA meeting is live in the wake of a benign May monthly CPI (2.1%), which opens the door to potential downward revisions to the Bank’s inflation outlook”.

NATO: Leaders Meet To Sign Off On 5% Spending Commitment

NATO leaders are delivering doorstep comments ahead of the main session of the alliance's summit in The Hague later this morning. Secretary General Mark Rutte is due to speak alongside US President Donald Trump shortly, followed by the welcoming ceremony and 'family photo' shortly. The meeting of the 'North Atlantic Council' (the collective group of NATO countries) at leaders' level gets underway ~10:30CET (04:30ET, 09:30BST ), with a live stream here.

- Rutte will hold a press conference after the Council meeting, at ~13:45CET (07:45ET, 12:45BST). He will then meet with the 'Indo-Pacific Partners' (Australia, Japan, New Zealand, South Korea) at 14:30CET (08:30ET, 13:30BST). The only IP-4 partner to have their head of gov't travel to the summit is New Zealand, with PM Christopher Luxon in attendance. All others have sent their foreign ministers.

- At ~15:30CET (09:30ET, 14:30BST) Rutte and the leaders of the E5 (France, Italy, Germany, Poland, Ukraine) will meet with Ukrainian President Volodymyr Zelenskyy. It is also expected that Zelenskyy will meet with President Trump during the course of the summit.

NATO leaders are expected to sign off on a much briefer communique than is usually the case at these events, due to its truncated nature (down to one session lasting a couple of hours, compared to the normal multiple sessions lasting several hours each). Commitments on the '3.5%+1.5%' of GDP on defence spending likely to be agreed, although potentially with wording that allows Spain, still holding out on the 5% total, to accept.

RIKSBANK: Minutes Dovish Leaning In Line With June Decision; Relaxed About

Overall, the Riksbank minutes suggest the Board does not seem too worried about possible upside inflation risks, placing further weight on the activity data to determine the likelihood of another cut this year. The minutes have a dovish bias, but that’s consistent with the tone of the June decision and rate path. As such there hasn’t been much reaction in SEK FX or rates.

Some further comments from Board members on the inflation/growth outlook:

- Bunge: “The weaker demand also reduces the scope for companies to raise prices. I think that the economic outlook in itself entails a risk for inflation being below target further ahead. In addition, the strengthening of the krona during the spring will have a dampening effect on import prices”.

- Breman: “Inflation outcomes and projections have strengthened out view of inflation being in line with the target going forward”….” At the same time, there are always risks of inflation going higher or lower than in the forecast”…” energy and food prices are particularly important for households' inflation expectations”

- “An overall assessment is that households and companies are in a wait-and-see mode, and this is weighing on the Swedish economy in a situation where we have had weak growth for several years”.

- Jansson: “A closer look at the details of the latest outcome rather paints a picture of more underlying inflationary pressures that risk becoming too low going forward"

- “The current situation for the Swedish real economy is not one in which there is any need to be concerned about a very rapid economic improvement that could ultimately create problems with excessively high demand-driven inflation”.

- Seim: “Even though there are factors that could create inflationary impulses in the economy, such as rising oil prices, supply chain shocks, increased transport costs, a weaker krona or fiscal policy stimulation measures, no such tendencies can be seen in the data. Rather, there is a risk that the weaker demand caused by the uncertainty will create low inflation”

- Thedeen: “Growth appears to be weakening somewhat, although I do not believe that the downturn will be particularly deep. However, as I perceive that the risks of inflation persistently overshooting the target have decreased somewhat”.