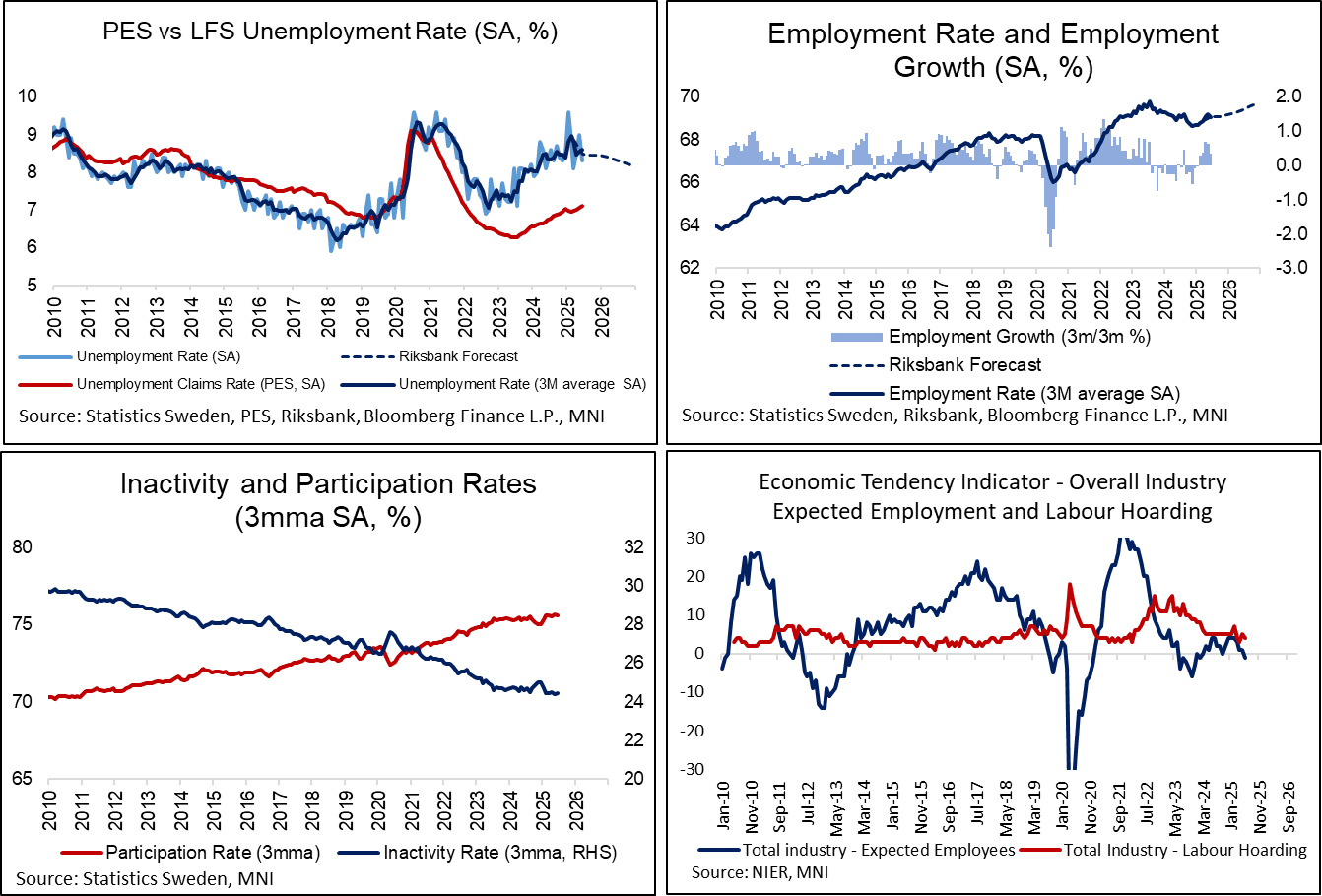

SWEDEN: June LFS Data Consistent With Steady But Subdued Labour Market

The June LFS labour market data appears consistent with steady but subdued conditions. When taken alongside a drift higher in the PES unemployment claims rate and a softening in the Economic Tendency Indicator’s expected employment metric, there is certainly some justification for market expectations of one more 25bp Riksbank cut at some point this year.

- The pullback in the seasonally adjusted LFS unemployment rate to 8.3% (vs 8.8% cons, 9.0% prior) was mostly due to a fall in the participation rate to 75.2% (vs 75.8% prior). However, the employment rate did tick up a touch to 69.0% from 68.9%.

- On a 3mma basis, the unemployment rate of 8.60% is above the Riksbank’s 8.47% projection from the June MPR.

- Meanwhile, the 3mma employment rate (69.07%) is broadly in line with Riksbank projections (69.05%). 3m/3m employment growth has actually been positive for five consecutive months now, despite more pessimistic survey data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

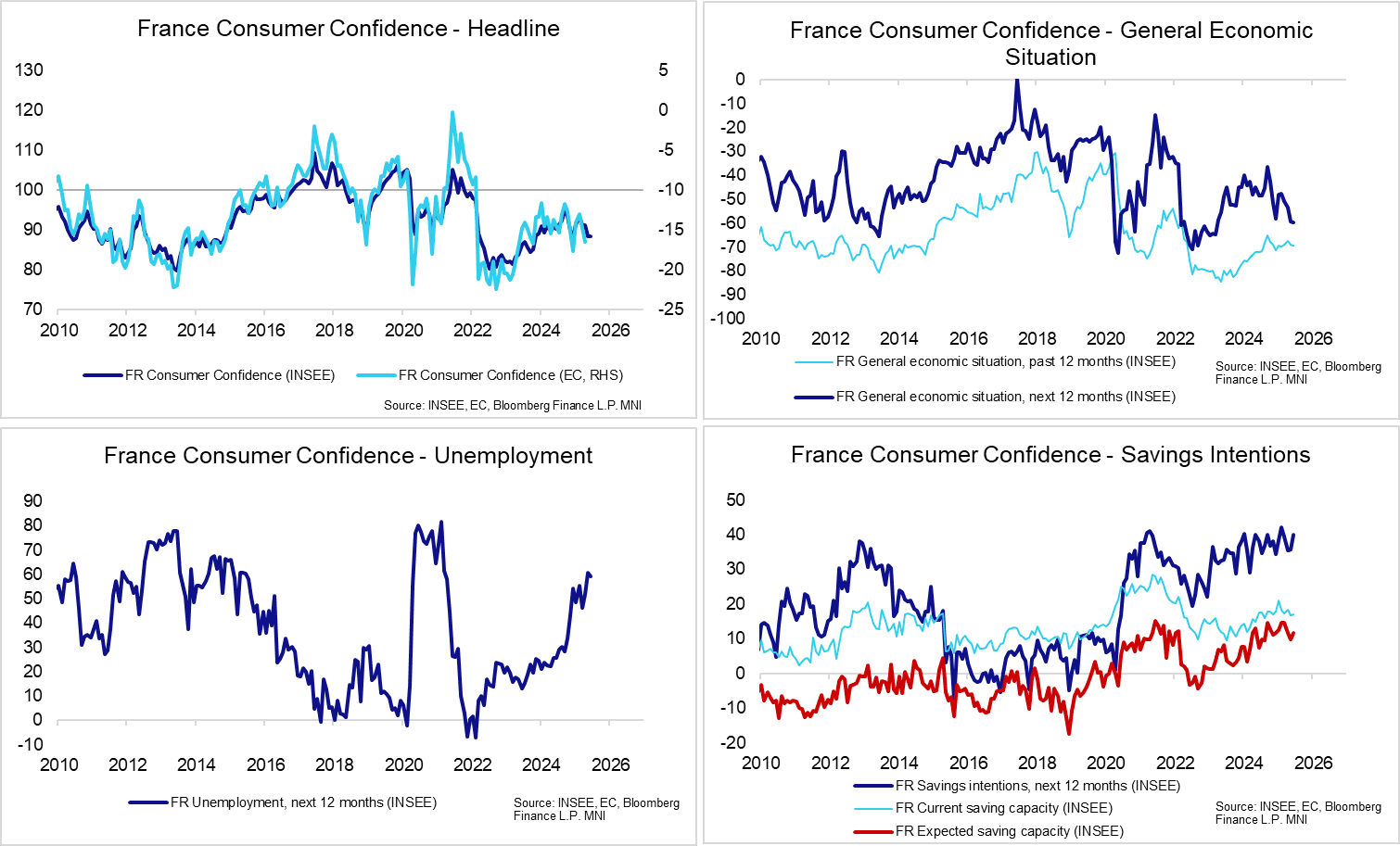

FRANCE DATA: French Consumer Sentiment Weak; Political Uncertainty In Focus

French June consumer confidence was steady at 88.4 (vs 88.3 prior), a touch below the 89.0 rounded consensus. There are likely downside risks to French sentiment ahead though, with political uncertainty set to ratchet higher again in the coming months. After the Bayrou government failed to reach an agreement on pension reforms with social partners yesterday, the Socialist party (supported by others on the left) have proposed a censure motion. While the far-right RN will not support censure at this stage, they have highlighted the 2026 budget as a key event to determine if they will continue to tacitly support (or at least, not bring down) Bayrou.

- In June, consumer’s perception of the general economic outlook worsened on both the backward- and forward-looking measures. Meanwhile, unemployment expectations remained elevated at 59.1 (vs 60.8 in May, 51.9 in April).

- Savings intentions also rose notably to 39.9 (vs 35.8 prior).

- The weak consumer outlook comes with Bayrou expected to propose further fiscal tightening measures in the 2026 budget proposal, provisionally due for next month.

BONDS: Firmer In Recent Trade

Some questions surrounding the bid in core global FI markets. Bund futures still within yesterday's range, while TY futures pierce yesterday's high.

- German curve bull flattens, U.S. paper and gilts see a parallel shift in yields.

- We can’t see a clear headline driver and the move has started to fade.

- News that the Iranian parliament has approved the legislation to suspend cooperation with the UN nuclear watchdog a potential factor, although it was expected, which could explain why the rally has faded a little.

- Also note that EGB spreads to Bunds are tighter, not wider here, suggesting a bit of a pull higher from the periphery.

- OATs manage to overcome the latest round of political uncertainty after the French Socialists filed a no-confidence measure against Prime Minister Bayrou following the collapse of the pension talks. Some suggest the motion is unlikely to pass at this stage, given the lack of support from the far-right. OAT/Bunds ~1.5bp tighter on the day, sub 69bp.

- E-minis consolidate near yesterday’s late NY highs, while the Q3 funding update out of Italy didn’t provide any material surprises.

SILVER TECHS: Trend Set-Up Remains Bullish

- RES 4: $39.026 - 1.382 proj of the Apr 7 - 25 - May 15 price swing

- RES 3: $38.246 - 1.236 proj of the Apr 7 - 25 - May 15 price swing

- RES 2: $38.000 - Round number resistance

- RES 1: $37.317 - High Jun 18

- PRICE: $35.973 @ 08:14 BST Jun 25

- SUP 1: $35.581 - 20-day EMA

- SUP 2: $34.315/31.651 - 50-day EMA / Low May 15

- SUP 3: $30.915/28.351 - Low Apr 11 / 7 and the bear trigger

- SUP 4: $27.686 - Low Sep 6 ‘24

A bull wave in Silver is in play and the latest pullback is considered corrective. The metal has recently traded through resistance at $34.903, the Oct 23 ‘24 high and a key bull trigger. The break of it marks an important medium-term bullish development. Sights are on the $38.00 handle next. On the downside, initial support to watch lies at $35.581, the 20-day EMA. It has been pierced, a clear break would open $34.315, the 50-day EMA.