MNI US OPEN - Riksbank, Norges Bank Unchanged Ahead of BoE

EXECUTIVE SUMMARY

- MNI BOE PREVIEW - COULD “GRADUAL” BE DROPPED?

- TRUMP ADMINISTRATION TO ANNOUNCE TRADE DEAL WITH BRITAIN

- RISKBANK HOLDS POLICY RATE, TWEAKS GUIDANCE

- NORGES BANK LEAVES POLICY AND GUIDANCE UNCHANGED

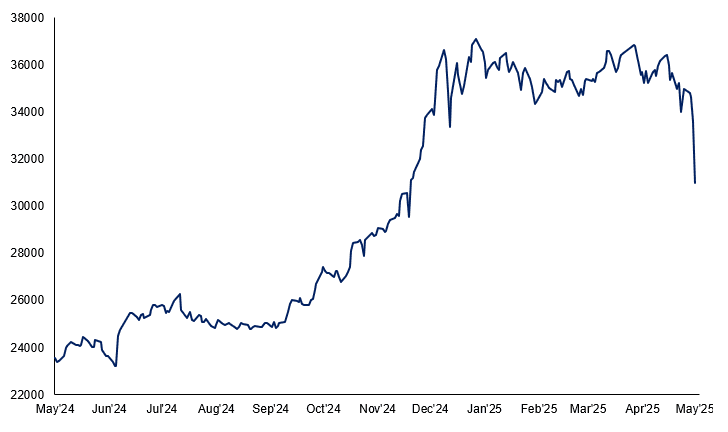

Figure 1: Pakistan's KSE-30 drops over 8% as tensions with India remain at boiling point

Source: MNI/Bloomberg

NEWS

MNI BOE PREVIEW - MAY 2025: Could “Gradual” Be Dropped?

Going into this week’s meeting an outcome other than a 25bp cut would be surprising but there will be a number of things to watch: any changes to the guidance and the inflation / growth forecast changes, the vote split and the introduction of new scenarios. For the guidance we expect "restrictive" and "careful" to remain but we question whether "gradual" will be removed and talk through the rationale for this potential change.

US/UK (NYT): Trump Administration to Announce Trade Deal With Britain

President Trump is expected to announce on Thursday that the United States will strike a trade agreement with Britain, according to three people familiar with the plans. Mr. Trump teased a new trade agreement in a social media post on Wednesday night, though he did not specify which nation was part of the deal. “Big News Conference tomorrow morning at 10:00 A.M., The Oval Office, concerning a MAJOR TRADE DEAL WITH REPRESENTATIVES OF A BIG, AND HIGHLY RESPECTED, COUNTRY. THE FIRST OF MANY!!!” he wrote.

US/UK (MNI): US Deal Unlikely to Be Comprehensive, but Boost to PM’s Standing Nonetheless

The gov't now confirming that an agreement on tariffs with the US will be announced later today. In terms of what is included, an important distinction will be on whether a 'trade deal' or 'trade agreement' is announced. As former BoE MPC member Jonathan Haskell told the BBC earlier today, "Trade deals are limited and short-term and partial, just covering a few items. Trade agreements are broad-based and long-term.". Says that a 'deal' could end up being a short-term change that sees, for example, specific tariffs paused for a certain amount of time.

US (BBG): Trump to Rescind Global Chip Curbs, Prep New AI Restrictions

The Trump administration plans to rescind some Biden-era AI chip curbs as part of a broader effort to revise global semiconductor trade restrictions that have drawn strong opposition from major tech companies and foreign governments. The repeal of the so-called AI diffusion rule, which is not yet final, seeks to refashion a policy launched under President Joe Biden that created three broad tiers of countries for regulating the export of chips from Nvidia Corp. and others.

US/CHINA (BBG): China Reiterates US Should Cancel Tariffs Ahead of Trade Talks

Beijing reiterated its call for the US to cancel unilateral tariffs on China, underscoring a standoff between the world’s largest economies as they prepare for initial trade talks. The US should be prepared to revoke punitive tariffs placed on China, Commerce Ministry spokesman He Yadong said at a regular press briefing Thursday. The US “needs to show sincerity to talk and be prepared to rectify its wrongdoing and cancel unilateral tariffs,” he said.

RIKSBANK (MNI): Riksbank Holds Policy Rate, Tweaks Guidance

The Riksbank left its key policy rate unchanged at 2.25%, as expected, and tweaked its guidance in a marginally more dovish direction. The Riksbank Executive Board stated that it was "somwhat more probable" that inflation would be lower rather than higher than predicted in the previous quarterly forecast round in March and that "this could suggest a slight easing of monetary policy going forward." The March rate path showed 2.25% as the trough with the rate near flat-lining throughout the three year forecast but many analysts now expect further easing ahead and the Swedish central bank has edged in that direction.

NORGES BANK (MNI): Norges Bank Leaves Policy and Guidance Unchanged

The Norwegian central bank's Monetary Policy and Financial Stability Committee left the policy rate unchanged at 4.5% and stuck to the line that the policy rate "will most likely be reduced in the course of 2025" without being more precise about the timing of the first cut. Norges Bank Deputy Governor Pal Longva warned on the risk of premature easing fuelling price increases and the committee stated that "a restrictive monetary policy is still needed to bring inflation down to target within a reasonable time horizon."

INDIA/PAKISTAN (WSJ): India and Pakistan Face Off but Seek to Contain Fallout

India and Pakistan faced off militarily after a militant attack on tourists that New Delhi blamed on Islamabad, but the nuclear-armed neighbors appeared to be calibrating their responses to avoid full-blown conflict after decades of relative peace. Pakistan threatened to hit back after retaliatory strikes by India on nine locations across Pakistan and Pakistan-controlled Kashmir overnight Wednesday. Islamabad said its response would correspond to actions taken by New Delhi, which had described its attacks as non-escalatory. Despite the violence, including cross-border shelling Wednesday, both sides sought to display a measured approach as the Trump administration urged them to avoid further escalation.

INDIA/PAKISTAN (BBG): Pakistan Stocks Plunge After Military Says It Shot India Drones

Pakistan’s stocks fell after the military said Thursday it shot down 12 drones from India, a sign that hostilities between the two nuclear-armed neighbors continue to escalate. The drones, dispatched in the early hours of Thursday, killed one civilian and injured four soldiers, Pakistan’s military spokesman Lieutenant General Ahmed Sharif Chaudhry said at a news conference, while showing photos of the fallen drones. After Chaudhry’s comments, Pakistan’s KSE-30 Index slumped 7.2%, leading to a one-hour trading halt as per exchange rules.

CHINA/RUSSIA (MNI): Xi & Putin Cement Ties With State Visit Underway

MNI (London) Chinese state-run Xinhua reports comments from President Xi Jinping following his meeting with Russian President Vladimir Putin in Moscow. Xi says that "China is ready to work with Russia to safeguard the authority and status of the United Nations, and resolutely defend the rights and interests of the two nations as well as those of developing countries in the face of unilateralism and bullying." Says the two countries should "promote an equal and orderly multipolar world and a universally beneficial and inclusive economic globalisation." Putin and Xi called one another 'dear friend' as Xi is set to observe Russia's Victory Day military parade as part of a four-day state visit.

CHINA (BBG): China Weighs Housing Market Overhaul to Curb Pre-Sales

China is mulling a dramatic overhaul in the way homes are sold nationwide, requiring developers to offer only completed properties instead of using the pre-sales model that has exacerbated the housing crisis, according to people familiar with the matter. The initiative, which hasn’t been finalized, is part of a “new model” of real estate development being formulated by the central government, the people said, asking not to be identified discussing a private matter.

GERMANY (MNI): Coalition to Focus First on Energy, Rent Freezes, Pension Level, Labour

SPD ministers in the German government are planning to initially focus on issues including energy price reductions, a rent freeze extension, ensuring a fix of the pension level at current rates, and "improving collective bargaining coverage" for employees, according to a BILD report overnight. On energy price reductions, CDU/CSU/SPD mention in their coalition agreement that

they plan to "permanently reduce the burden on companies and consumers in Germany by at least five cents per kWh with a package of measures" incl. electricity tax, grid surcharge and levy reductions, as well as the introduction of an industry energy price for certain companies.

BOJ (BBG): BOJ’s Ueda Says Can’t Ignore Risk of Tariffs Affecting Inflation

Bank of Japan Governor Kazuo Ueda says the bank can’t ignore the potential downside risks to prices stemming from US tariff measures. Uncertainties over the outlook for inflation are high, Ueda says in response to questions in parliament. Will closely watch whether food inflation has ripple effects that influence underlying inflation. Expects Japan’s price trend to move toward 2% target in the second half of its three-year outlook period ending March 2028.

BRAZIL (MNI): BCB to Halt Rate Hikes, Higher for Longer Strategy

The Central Bank of Brazil gave strong evidence that the monetary tightening cycle has come to an end with Wednesday’s 50 basis-point hike to 14.75%, as it provided no forward guidance for June and included in the statement that interest rates should remain significantly contractionary “for a prolonged period.” "For the next meeting, the scenario of heightened uncertainty, combined with the advanced stage of the current monetary policy cycle and its cumulative impacts yet to be observed, requires additional caution in the monetary policy action and flexibility to incorporate data that impact the inflation outlook," the statement said. This is likely to curb bets on a residual hike in June and shift the market discussion toward when rate cuts might begin.

NORTH KOREA (MNI): N. Korea Test-Fires SRBMs Amid Talk of Potential Export to Russia

Yonhap News Agency reported that North Korea fired multiple short-range ballistic missiles (SRBMs) from the coastal city of Wonsan towards the East Sea today amid suspicions that it was testing arms before their delivery to Russia. South Korea's Joint Chiefs of Staff (JCS) said that the North may have launched projectiles similar to Russia's Iskander missiles, which 'could be a test to inspect performance or flight stability for possible exports.'

CORPORATE (BBG): Toyota Sees $1.3 Billion Profit Hit in Two Months on Tariffs

Toyota Motor Corp. said US President Donald Trump’s tariffs will result in a ¥180 billion ($1.3 billion) hit to operating income in just two months, with the Japanese carmaker joining a growing list of companies grappling with the fallout of trade turmoil. The company said Thursday that the impact for April and May has been tentatively factored in, and the situation remains uncertain. That’s set to weigh on its full-year results, with its outlook for operating income of ¥3.8 trillion for the year ending March 31, 2026 falling far short of analyst expectations of ¥4.7 trillion.

DATA

GERMANY DATA (MNI): Q1 Trade Surplus Opens Up Possibility for GDP Revision

The German trade surplus increased in March to E21.1bln (seasonally-adjusted, vs E19.1bln cons; E18.0bln prior, revised from E17.7bln). This was driven by a 1.4% M/M decline in imports (0.4% cons; 0.5% prior, revised from 0.7%) and a 1.1% in exports (1.0% cons; 1.8% prior, revised from 1.9%). On a 3m/3m comparison, that means that the trade surplus increased 2.6% (-3.4% Q4) - that is notable since net exports were not flagged as a positive driver by Destatis in their Q1 flash GDP commentary, opening up at least the possibility for a positive revision on these grounds.

GERMANY DATA (MNI): IP Confirms March as Strong Month for Industry Boosted by Pharma

German industrial production grew 3.0% M/M, more than consensus of 1.0% (February -1.3%). That means that Q1 overall saw 1.4% higher production volumes than Q4'24 - the most significant increase since the beginning of early 2022. On a yearly comparison, IP remains negative (but less so than before) at -0.2% Y/Y (Feb -4.1%, revised from -4.0%; the Y/Y has been negative each month since May 2023). In combination with firm factory orders, the print confirms March was a comparatively strong month for German manufacturing - which might have been underpinned by US tariff frontrunning, the German economy ministry speculates.

SPAIN DATA (MNI): Strong Spanish March IP Driven by Energy

The 0.9% rise in Spanish March IP (vs four analyst estimates ranging between 0.0-0.2%) still leaves 3m/3m growth negative at -0.3% (vs -0.2% prior). This is consistent with waning momentum in the manufacturing PMI, but we note that industry value added was 1.1% Q/Q in Q1, according to the flash national accounts. Energy drove the increase in March, rising 3.2% M/M and 3.4% on a 3m/3m basis (vs 2.4% prior). Meanwhile, consumer, capital and intermediate goods also saw positive sequential monthly readings.

NORWAY DATA (MNI): Industry Should Make Positive Contribution to Mainland Value Added in Q1

Norwegian manufacturing industrial production was flat in March on a seasonally adjusted basis, pulling 3m/3m growth down to 1.6% (vs 2.8% prior). That still indicates a positive contribution from industry to Q1 mainland value added, consistent with the expansionary industrial confidence indicator. Notably, momentum in non-petroleum related manufacturing industries has shown signs of recovery, albeit from a low base. 3m/3m growth was 2.1% in March (vs 3.5% prior), with intermediate goods growing 1.0%, capital goods 0.3% and consumer goods 1.6%.

SWEDEN DATA (MNI): Budget Deficit Widens More Than NDO Forecast

The Swedish budget deficit widened to SEK42.2bln in April, above the National Debt Office's SEK27.7bln forecast. That sees the cumulative forecast error since the November 2024 borrowing report widen to SEK19bln. This forecast error, alongside the SEK11.5bln of measures announced in the Government's Spring Budget Bill last month, will need to be accounted for the upcoming forecast/debt issuance plan presented on May 22. Some analysts expect an increase in total borrowing and announced bond auction sizes at that event.

FOREX: Firmer USD Theme Plays Out, Threatening EUR, GBP Consolidation Phases

- The ripple effect of the hawkish Fed yesterday continues to be felt across G10 FX early Friday, with the dollar stronger against all others in G10. USD/JPY has made light work of yesterday's highs and is narrowing in on the next key upside levels at Y145.08 and the bull trigger of Y145.92. Powell's defence of the Fed's policy plans for 2025 reinforced to markets that the Fed won't be pressured or rushed into easing rates this year, adding some pressure to market pricing - ~75bps of easing are now priced for 2025, down from 80bps this time yesterday.

- USD gains are keeping EUR/USD tilted toward recent lows, and well within range of horizontal support at 1.1266. Clearance through here would be a bearish signal, opening levels last seen in early April and turning focus to 1.1110, the 38.2% retracement of the tariff upleg for direction.

- The White House and Downing Street are expected to unveil details of their tariff-reducing trade deal later today - which would be the first since the 90-day tariff delay outlined by Trump a few weeks ago. GBP has seen little reprieve despite local equities seeing early gains. GBP/USD is back below the $1.3300 handle, marking support at 1.3234, a break below which would end the two-week consolidative phase in the pair. Announcements on trade are expected from 1000ET/1500BST.

- The Bank of England are expected to cut rates by 25bps to 4.25% at today's 1202BST rate decision. Focus will be on the language used in the subsequent press conference with Bailey - and in particular whether the phrasing around "gradual" easing will be removed - signalling potential for a faster pace of rate cuts ahead.

- Weekly US jobless claims and the Bank of Canada's Financial Stability Report are then set to cross.

BONDS: Bunds Lower on Equity Bid, Gilts Holding Steady Ahead of BoE

EGBs are lower on the day, with some positive reports on global trade matters (apparent advances in UK-U.S. trade talks and suggestions that the U.S. is set to relax export restrictions for chips) weighing, while providing support for equities

- Bund futures comfortably within yesterday’s range, last -21 at 131.30. Initial support and resistance located at 131.24 and 131.90, respectively.

- German yields 2.5-3.5bp higher, light steepening bias.

- EGB spreads to Bunds a touch tighter alongside the equity bid, BTP/Bunds now ~1bp above year-to-date closing lows, last ~106.5bp.

- SPGB supply passed smoothly enough.

- Gilts have stuck to a narrow range.

- Futures did tick above yesterday’s highs but have faded since, with more meaningful resistance at 93.93 unchallenged, last -6 at 93.37.

- Yields little changed, tightening vs. Bunds.

- 10s last flat at 4.46%, above uptrend support drawn off the Dec ’21 low (4.421% today)

- 2s10s and 5s30s remain shy of cycle highs, aided by the more activist approach to supply considerations from the DMO and BoE in recent weeks, skewing sales away from the long end.

- The BoE decision dominates the UK calendar today. A 25bp cut is both fully discounted and unanimously expected (97bp of easing priced through year-end).

- There are dovish risks to both the guidance and vote split, we eye a potential removal of the word “gradual” from the former and have flagged a chance of more than one vote for a 50bp cut (consensus looks for 8-1, with Dhingra voting for a 50bp move).

- We believe this skews the risks towards gilt curve steepening intraday and eye GBP 1y1y and SFIM5/M6 further forward on the curve (if dovish risks crystalise).

EQUITIES: Eurostoxx 50 Futures Maintain Bullish Tone, Close to Recent Highs

Eurostoxx 50 futures maintain a bullish tone and the contract is trading at its recent highs. Price has recently cleared both the 20- and 50-day EMAs, and attention is on 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. This hurdle has recently been pierced, a clear break of it would pave the way for a climb towards 5341.00, the Mar 27 high. Initial support to watch lies at 5093.95, the 20-day EMA. Clearance of this level would signal a possible reversal. Trend conditions in S&P E-Minis are unchanged, they remain bullish. The contract has breached the 50-day EMA, at 5624.12. A continuation higher would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5547.58, the 20-day EMA.

- Japan's NIKKEI closed higher by 148.97 pts or +0.41% at 36928.63 and the TOPIX ended 2.56 pts higher or +0.09% at 2698.72.

- Elsewhere, in China the SHANGHAI closed higher by 9.331 pts or +0.28% at 3351.996 and the HANG SENG ended 84.04 pts higher or +0.37% at 22775.92.

- Across Europe, Germany's DAX trades higher by 229.92 pts or +0.99% at 23345.01, FTSE 100 higher by 22.35 pts or +0.26% at 8581.84, CAC 40 up 65.3 pts or +0.86% at 7691.61 and Euro Stoxx 50 up 56.42 pts or +1.08% at 5285.96.

- Dow Jones mini up 266 pts or +0.65% at 41483, S&P 500 mini up 51 pts or +0.9% at 5703, NASDAQ mini up 256 pts or +1.28% at 20217.25.

Time: 09:55 BST

COMMODITIES: Short-Term WTI Future Gains Still Considered Corrective

A downtrend in WTI futures remains intact and short-term gains are considered corrective. The move down that started Apr 23 signals the end of the correction between Apr 9 - 23. That cycle higher allowed an oversold condition to unwind. Attention is on $54.67, the Apr 9 low and a bear trigger. Clearance of this level would resume the downtrend and open $53.72, a Fibonacci projection. Key resistance to watch is $63.88, the 50-day EMA. Gold has recovered from its recent lows. The rally suggests the correction between Apr 22 - May 1, is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the primary uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

- WTI Crude up $0.49 or +0.84% at $58.54

- Natural Gas up $0.04 or +0.99% at $3.656

- Gold spot down $26.21 or -0.78% at $3338.74

- Copper down $6.85 or -1.47% at $458.9

- Silver down $0.13 or -0.41% at $32.327

- Platinum down $2.32 or -0.24% at $976.61

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem press conference on Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 09/05/2025 | 2330/0830 | ** | average wages (p) | |

| 09/05/2025 | 2330/0830 | ** | Household spending | |

| 09/05/2025 | 0600/0800 | *** | CPI Norway | |

| 09/05/2025 | 0800/1000 | * | Industrial Production | |

| 09/05/2025 | 0840/0940 | BOE Bailey Keynote Address at Reykjavik Economic Conference | ||

| 09/05/2025 | 0955/0555 | Fed Governor Michael Barr | ||

| 09/05/2025 | 1045/0645 | Fed Governor Adriana Kugler | ||

| 09/05/2025 | 1115/1215 | BOE's Pill At National MPC Agency Briefing | ||

| 09/05/2025 | - | *** | Trade | |

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | New York Fed's John Williams | ||

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 09/05/2025 | 1235/0835 | New York Fed's Roberto Perli | ||

| 09/05/2025 | 1530/1130 | Fed Governor Christopher Waller | ||

| 09/05/2025 | 1530/1130 | New York Fed's John Williams | ||

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |