MNI US OPEN - Powell, Lagarde, Ueda to Speak at Jackson Hole

EXECUTIVE SUMMARY

- MNI JACKSON HOLE PREVIEW

- POWELL, BAILEY, LAGARDE, UEDA TO SPEAK AT JACKSON HOLE

- RBNZ'S CONWAY SEES LOWER OCR ON WEAK GROWTH

- JAPAN HEADLINE CPI MODERATES, CORE MEASURES STAY STICKY

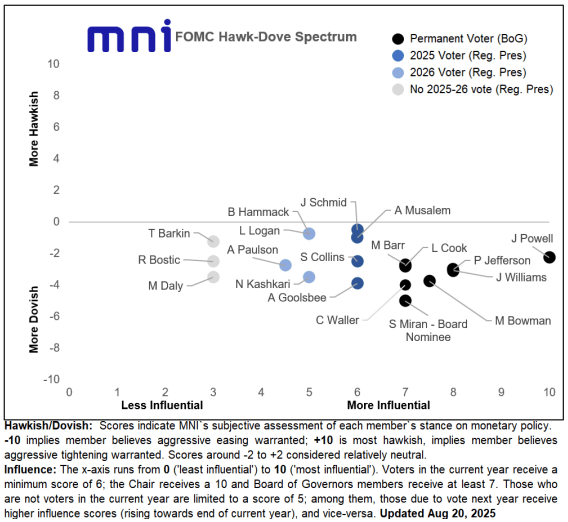

Figure 1: MNI FOMC Hawk-Dove Spectrum

NEWS

The key event at the annual Jackson Hole Economic Policy Symposium (Aug 21-23) is Chair Powell's speech on Friday (1000ET/1500UK). Attention will of course mostly be on any nod Powell makes to a potential September Fed rate cut, a prospect which we discuss in this preview. MNI's Markets Team believes that in contrast to Jackson Hole 2024, Powell will avoid an overtly dovish nod at this meeting, given how split the Committee appears to be on the need to cut rates.

JACKSON HOLE (MNI): Powell, Bailey, Lagarde, Ueda to Speak at Jackson Hole

Federal Reserve Chair Jerome Powell will deliver opening remarks at the Kansas City Fed's annual Jackson Hole symposium Friday at 10 a.m. ET, and Andrew Bailey, Christine Lagarde and Kazuo Ueda, leaders of the Bank of England, ECB and Bank of Japan, respectively, will discuss labor market transition on a panel Saturday at 12:25 p.m. ET. The full agenda of the conference, themed "Labor Markets In Transition: Demographics, Productivity and Macroeconomic Policy", can be found in the link above. Four academic papers will also be presented, each of which are to be posted online at their presentation time.

FED (WSJ): Powell Plans U-Turn on an Economic Strategy That Soured

Federal Reserve officials are preparing to quietly retreat from a signature policy innovation unveiled five years ago. In 2020, officials revamped their approach to setting rates, focusing on the risks brought on by near-zero interest rates and low prices. Today, officials are preparing to scrap that approach, now viewed as no longer relevant when facing the opposite problem of high and more volatile inflation. Fed Chair Jerome Powell is expected to lay out these changes at the Kansas City Fed's economic symposium in Jackson Hole, Wyo., on Friday in what has become the central banking world's most closely watched annual address.

US (WSJ): How Trump Will Decide Which Chips Act Companies Must Give Up Equity

The Trump administration is considering taking equity stakes in companies receiving funds from the 2022 Chips Act but has no plans to seek shares in bigger semiconductor firms that are increasing their U.S. investments, according to a government official. Commerce Secretary Howard Lutnick confirmed in a Tuesday interview with CNBC that the government is in talks to take a 10% equity stake in the troubled semiconductor company Intel and said the administration may consider equity stakes in other firms as well. The comments fueled worries among industry executives that the government might also take equity stakes in large chip makers like Taiwan Semiconductor Manufacturing, Micron Technology and Samsung.

US/CHINA (BBG): Nvidia Asks Suppliers to Halt H20 Work, Information Says

Nvidia Corp. has instructed component suppliers including Samsung Electronics Co. and Amkor Technology Inc. to stop production related to the H20 AI chip, The Information reported, citing unidentified sources. Nvidia issued those orders this week after Beijing urged local companies to avoid using the H20, the Information said, referring to a chip designed specifically for the Chinese market. The US company’s shares slid about 1.9% on alternative trading system Blue Ocean during the Asia morning, said Kok Hoong Wong, head of institutional equities sales trading at Maybank Securities.

EU (FT): EU Speeds Up Plans for Digital Euro After US Stablecoin Law

EU officials are accelerating plans for a digital euro, according to people involved in the discussions, after a new US stablecoin law deepened worries about the competitiveness of a European digital currency. The US Congress last month passed a landmark law overseeing the $288bn stablecoin market, which is largely dominated by the dollar, after extensive lobbying by the crypto industry.

UK (The Times): Quarter of Labour members set to back Jeremy Corbyn’s new party

One in four Labour members could back Jeremy Corbyn’s party at the next general election. Twenty-eight per cent of those surveyed said they were considering supporting the former Labour leader’s new left-wing, pro-Gaza movement, which is set to be launched formally in the autumn. Corbyn announced the venture along with fellow MP Zarah Sultana in July, aiming to win over disaffected Labour voters. The pair will be heartened by polling from Survation, which shows the majority of Labour members want Sir Keir Starmer’s party to change direction.

ISRAEL (BBG): Israel’s Netanyahu Sent Aide to UAE in Quiet Push to Fix Ties

Israeli Prime Minister Benjamin Netanyahu dispatched his top foreign-policy aide to the United Arab Emirates in a bid to improve relations strained by his government’s military campaign in Gaza and expansion of Jewish settlements in the West Bank, according to people with knowledge of the matter. Ron Dermer, Israel’s strategic affairs minister, traveled to the UAE capital of Abu Dhabi last week and held talks with officials including President Sheikh Mohamed Bin Zayed, said the people, who asked not to be identified discussing private meetings.

CHINA (BBG): China Makes Veiled Jab at US Before Hosting Modi, Putin, Erdogan

China used an event marking the final stretch before its biggest diplomatic event of the year to accuse the US of “threatening world peace,” in a thinly veiled critique of the rival superpower just before it hosts a key gathering of global leaders. More than 20 foreign leaders are set to attend the annual summit of the Shanghai Cooperation Organisation, a bloc of countries led by Russia and China, Assistant Foreign Minister Liu Bin told reporters Friday during a briefing in Beijing.

JAPAN (MNI): PM Ishiba's Position Looks More Assured as Polling Improves

Following the 20 July House of Councillors election it was widely assumed that PM Shigeru Ishiba's ouster from office was a matter of 'when' rather than 'if' after the ruling Liberal Democratic Party (LDP)-Komeito coalition lost its majority in the upper house (having already lost its majority in the lower house in the 2024 election). However, a groundswell of public support for the PM has seen betting market odds of his removal from office (in 2025 at least) plummet.

S.KOREA/JAPAN (BBG): South Korean Leader’s Japan Visit to Set Stage for Trump Summit

South Korean President Lee Jae Myung is set to embark on his first overseas trip focusing on bilateral diplomacy this weekend starting with a rare Japan visit that will likely set the stage for his first meeting with President Donald Trump in the US days later. Leaders from South Korea almost always choose the US, the country’s key security ally, as their first destination abroad after taking office. The decision to head to Tokyo to meet Prime Minister Shigeru Ishiba before meeting with Trump on Monday is all the more unexpected given Lee’s reputation as a fierce critic of Japan before he became president.

RBNZ (MNI INTERVIEW): RBNZ's Conway Sees Lower OCR on Weak Growth

The RBNZ's Chief Economist shares his views on the OCR. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

EUROZONE DATA (MNI): Expected Rise in ECB Q2 Negotiated Wages

ECB Q2 Negotiated Wages: 3.95% (vs 2.46% in Q1). An increase was broadly expected by analysts based on national-level tracking. ECB forward-looking wage tracker with unsmoothed one-off payments for Q2: 4.02% Y/Y. It once again does a good job of tracking the actual negotiated wages release. We have noted that the importance of the quarterly negotiated wages series has fallen since the forward looking tracker started being published.

GERMANY DATA (MNI): Q2 GDP Expenditure Split Highlights Weakness

- GERMANY Q2 FINAL GDP SA -0.3% Q/Q, WDA +0.2% Y/Y

Germany's final Q2 GDP growth figures were downwardly revised by 0.2pp, at -0.3% Q/Q (-0.1% flash, 0.3% Q1). "In June 2025 output in manufacturing and in the construction industry, in particular, was worse than expected. In addition, household final consumption expenditure for the 2nd quarter of 2025 has been revised downwards due to new information available on the services sectors", Destatis comments on drivers for the revision. Underlying drivers point towards a weak print, with lower investment, while government expenditures contributed positively.

UK AUG GFK CONSUMER CONFIDENCE INDEX -17 (MNI)

FRANCE AUG MANUF SENTIMENT 96 (MNI)

SWEDEN DATA (MNI): Another Weak Labour Market Report

- SWEDEN JUL UNEMPLOYMENT 8%

The Swedish labour market remains weak, according to the July LFS report. The seasonally adjusted unemployment rate rose six tenths to 8.9%, above the six analyst-strong consensus of 8.6% and June's 8.3%. The Riksbank retained its dovish bias at the August decision, and continued weakness in labour market outcomes leans in favour of one more cut this cycle, potentially as early as September. The final Q2 GDP report (August 29) and August inflation round (early September) will be key to monitor in the coming weeks.

JAPAN DATA (MNI): Headline CPI Moderates, Core Measures Stay Sticky

Japan July nationwide CPI was close to market expectations. Headline printed at 3.1%y/y, in line with market forecasts, while prior was 3.3%. The ex fresh food measure was slightly above expectations at 3.1% (3.0% was forecast and June printed at 3.3%). The ex fresh food, energy core measure was steady at 3.4%y/y, in line with the consensus estimate (3.4% was also the June outcome). Headline is now comfortably off 2025 highs (3.7%), but core measures are seeing less downside momentum in recent months. Still, the core measure which excludes all food and energy was steady at 1.6%y/y, which is where we have been on this metric since March of this year.

RATINGS: Stable Sovereign Outlooks Up for Review Later

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Fitch on the United Kingdom (current rating: AA-; Outlook Stable)

- Moody’s on Austria (current rating: Aa1; Outlook Stable) & Sweden (current rating: Aaa; Outlook Stable)

FOREX: USD Index Holds Firm Into Powell Appearance

- The USD Index hold firms early Friday, building on the closing gains from Thursday trade. Focus for the duration of Friday rests on the speech from Fed's Powell at the Jackson Hole Policy Symposium. With markets pricing 15-20bps of cuts for the September meeting, Powell's conviction on easing policy, or not easing policy, at today's speech could prove highly market-moving.

- GBP/USD printed a new pullback low alongside the European open, marking six consecutive sessions of lower highs and lower lows as the correction continues. Weakness in pair this week comes in the context of a bullish background condition. Recent gains resulted in a breach of 1.3589, the Jul 24 high, signaling scope for a climb towards 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1.

- The very front-end of the USD vol curve has printed very minimal risk premium headed into Friday's Powell speech - potentially signalling that markets are looking through this year's Jackson Hole symposium as the trigger to revalue vols to the year's norms.

- Indeed, one-week EUR vols printed multi-month lows of 6.2 points earlier this week - the lowest of Trump's term in office so far - mirroring realised vols, that saw very little pick-up on recent US PPI and UK CPI surprises this week. Worth noting Powell's appearance coincides with the Friday 10am NY cut.

- Outside of Powell's appearance at 1500BST/1000ET, Canadian retail sales are due, with markets expecting a rebound after the particularly poor May reading. Fed's Collins and Hammack are also set to speak. Hammack's comments moved markets yesterday, after the Cleveland Fed rep talked against a September cut.

EGBS: Bunds Outperforming Core FI Peers, But Technical Bear Threat Still Present

Bunds are outperforming USTs and Gilts this morning, but remain only +3 ticks today at 129.08. A technical bear threat nonetheless remains present, with strength above the 20-day EMA (129.52) and the more important 50-day EMA (129.84) required to signal a reversal.

- German Q2 GDP was revised down two tenths to -0.3% Q/Q, but didn’t move markets given the weak June industrial production had already pointed to a downward revision. Similarly, ECB Q2 negotiated wages rose to 3.95% Y/Y (vs 2.46% in Q1), broadly in line with the bank’s forward looking wage tracker.

- The German curve has very lightly twist flattened, with 2-year yields up 0.5bps and 30-year yields down ~1bp. In the 10-year, the 2.80% handle remains the main level to watch on the upside (currently at 2.755%).

- 10-year EGB spreads to Bunds are now a little tighter on the session, with European equity futures off lows. The BTP/Bund spread briefly tested the 84bp handle this morning, before easing back to 82bps at typing.

- Global focus remains on Fed Chair Powell’s Jackson Hole address at 1500BST.

GILTS: Support Pierced in Futures

Gilt weakness has extended, with support breached in futures and 10-Year yields topping 4.75%.

- Futures as low as 90.34.

- Technical outlook in the contract remains bearish. Initial support at the August 19 low (90.43) is pierced, with the next downside level of note located at 90.11.

- Yields are ~2bp higher across the curve.

- Upside levels of interest in 10-Year yields are 4.80% followed by the cycle high 4.921%.

- SONIA futures flat to -4.5, SFIZ5 tests the late May low, while SFIZ6 nears its August low.

- Just 8bp of BoE easing is priced into OIS through year-end.

- Little of note on the UK calendar today, with broader focus on Fed Chair Powell’s Jackson Hole appearance.

- Roll actively is notably boosting volume in gilt futures, with ~80% of today’s activity in U5 seemingly related to roll flow. A reminder that U5 goes first notice on Thursday 28 August. A thinner calendar ahead of comments from Fed Chair Powell and the long weekend in the UK is likely expediting roll flow.

- Elsewhere, BoE Governor Bailey will speak on a panel with other central bank leaders on Saturday. The topic covered will be “the policy implications of labour market transition”.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.976 | +0.8 |

Nov-25 | 3.926 | -4.1 |

Dec-25 | 3.889 | -7.8 |

Feb-26 | 3.801 | -16.7 |

Mar-26 | 3.764 | -20.4 |

Apr-26 | 3.697 | -27.0 |

EQUITIES: Recent Pullback for E-Mini S&P Appears Corrective for Now

The trend set-up in Eurostoxx 50 futures remains bullish and the contract traded to a fresh short-term cycle high earlier this week. The recent print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies are in a bull-mode position, highlighting an uptrend. Support to watch lies at 5365.06, the 50-day EMA. The dominant uptrend in S&P E-Minis remains intact and the latest retracement appears to be a correction - for now. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, support to watch lies at 6291.07, the 50-day EMA.

- Japan's NIKKEI closed higher by 23.12 pts or +0.05% at 42633.29 and the TOPIX ended 17.92 pts higher or +0.58% at 3100.87.

- Elsewhere, in China the SHANGHAI closed higher by 54.66 pts or +1.45% at 3825.759 and the HANG SENG ended 234.53 pts higher or +0.93% at 25339.14.

- Across Europe, Germany's DAX trades higher by 32.33 pts or +0.13% at 24326.07, FTSE 100 lower by 2.5 pts or -0.03% at 9306.74, CAC 40 up 18.32 pts or +0.23% at 7957.24 and Euro Stoxx 50 up 17.75 pts or +0.33% at 5480.67.

- Dow Jones mini up 120 pts or +0.27% at 44972, S&P 500 mini up 13.5 pts or +0.21% at 6401.5, NASDAQ mini up 32.25 pts or +0.14% at 23252.

Time: 10:00 BST

COMMODITIES: Bear Cycle in WTI Futures Intact Despite Short-Term Gains

A bear cycle in WTI futures remains intact and short-term gains appear corrective - for now. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $63.85, the 50-day EMA. A bull cycle in Gold remains intact. Moving average studies are in a bull-mode position highlighting a dominant uptrend. The sideways trend that has been in place since the Apr peak appears to be a medium-term pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

- WTI Crude down $0.08 or -0.13% at $63.44

- Natural Gas down $0.04 or -1.38% at $2.787

- Gold spot down $8.52 or -0.26% at $3330.15

- Copper up $0.6 or +0.13% at $451.8

- Silver down $0.09 or -0.23% at $38.0579

- Platinum down $13.2 or -0.97% at $1344.57

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1400/1000 | Fed Chair Jerome Powell | ||

| 22/08/2025 | 1400/1000 | *** | US Fed Chair Speech | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/08/2025 | 1625/1725 | BOE Bailey at Jackson Hole | ||

| 23/08/2025 | 1625/1825 | ECB Lagarde at Jackson Hole |