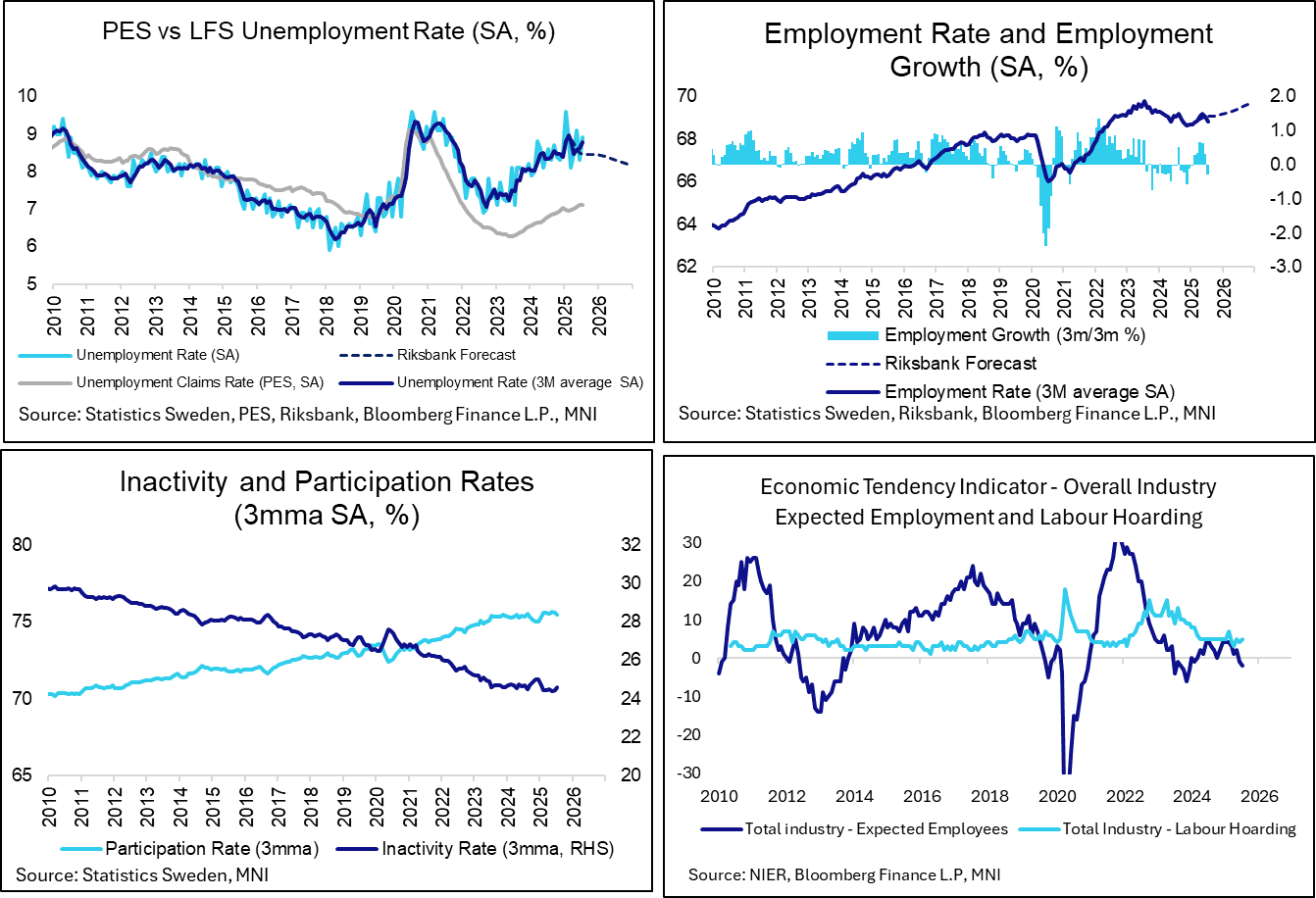

SWEDEN: Another Weak Labour Market Report

The Swedish labour market remains weak, according to the July LFS report. The seasonally adjusted unemployment rate rose six tenths to 8.9%, above the six analyst-strong consensus of 8.6% and June's 8.3%. The Riksbank retained its dovish bias at the August decision, and continued weakness in labour market outcomes leans in favour of one more cut this cycle, potentially as early as September. The final Q2 GDP report (August 29) and August inflation round (early September) will be key to monitor in the coming weeks.

- The LFS report can be volatile month-to-month, with recent swings in the unemployment rate having mostly been a function of labour force changes rather than weaker employment figures.

- However, in July, the unemployment rise was a result of both an increase in the participation rate to 75.3% (vs 75.2% prior) and a fall in the employment rate to 68.6% (vs 68.9% prior).

- On a 3m/3m basis, employment growth was negative (-0.3% vs 0.3% prior) for the first time since December 2024. This echoes the weak signals from the Economic Tendency Indicator’s expected employment series.

- In its August Monetary Policy Update, the Riksbank noted that “it will take time before the labour market improves. Although unemployment fell somewhat during the second quarter, to just above 8.5 per cent, indicators such as redundancy notices and job vacancies point to a continued weak development in the near term. The low growth in the economy is contributing to it taking longer until labour market conditions improves”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Developments In Japan Pull Bunds Lower Overnight

Bund futures were biased lower overnight and have erased all of yesterday’s gains, currently -34 ticks at 130.40. For now, futures remain above the 50-day EMA, which was pierced on Monday. This has undermined a bearish theme and highlights a possible reversal. Initial support is 129.73 (July 21 low), followed by 129.08 (July 14 low).

- Developments in Japan have been the primary source of pressure for FI markets overnight:

- Equity markets are rallying on news of a US-Japan trade deal (Nikkei almost +4%, Eurostoxx 50 futures +1.2%). The deal reduces the tariff on Japanese goods to 15% (from the previous threat of 25%) in exchange for USD550bln of investments into the US. This has increased optimism for further deals with the likes of the EU and China.

- The long-end of the JGB curve remains under pressure following a weak 40-year auction. 40-year yields are up 8bps on the session.

- Reports that Japanese PM Ishiba is set to resign this weekend may have provided further tailwinds to equities and upward pressure on yields, amidst hopes for more fiscal spending in Japan. 10-year JGB yields have reached their highest since 2011 at 1.596%.

- EGB spreads to Bunds unsurprisingly look set to open tighter given the support for risk assets. BTP futures are down 21 ticks at 121.18 at typing.

- Germany will return to the market today with E5bln of the 10-year 2.60% Aug-35 Bund on offer.

- Today’s data calendar includes Eurozone flash July consumer confidence at 1500BST.

- Broader focus remains on tomorrow’s flash PMIs and the ECB decision (MNI preview here )

BRENT TECHS: (U5) Technical Set-Up Remains Bearish

- RES 4: $85.00 - Round number resistance

- RES 3: $81.99 - 2.764 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $80.72 - 2.618 proj of the Apr 9 - 23 - May 5 price swing

- RES 1: $72.66/79.40 - 50.0% of the Jun 23-30 range / High Jun 23

- PRICE: $68.78 @ 07:00 BST Jul 23

- SUP 1: $65.92 - Low Jun 30

- SUP 2: $61.39 - Low May 30

- SUP 3: $58.00 - Low May 5

- SUP 4: $57.70 - Low Apr 9 and a key support

The technical set-up in Brent futures is unchanged. A bearish theme is present and the July recovery appears corrective. The sell-off on Jun 23 continues to highlight a bearish threat. Recent weakness has resulted in a print below the 50-day EMA and note too that $66.17, 61.8% of the May 5 - Jun 23 bull leg, has been pierced. A resumption of the bear leg would expose $61.39, May 30 low. Initial resistance to watch is $72.66, a Fibonacci point.

BTP TECHS: (U5) The Bull Trigger Remains Exposed

- RES 4: 122.71 2.764proj of the May 14 - 20 - 21 price swing

- RES 3: 122.35 2.500 proj of the May 14 - 20 - 21 price swing

- RES 2: 122.00 Round number resistance

- RES 1: 121.42/121.73 High Jul 22 / High Jun 13 and the bull trigger

- PRICE: 121.39 @ Close Jul 22

- SUP 1: 120.65/119.84 20-day EMA / Low Jul 14 and key S/T support

- SUP 2: 119.48 Low May 26

- SUP 3: 118.87 Low May 21

- SUP 4: 118.51 Low May 14 and key support

The primary trend condition in BTP futures remains bullish and this week’s strong rally reinforces this theme. Key short-term support has been defined at 119.84, the Jul 14 low. A break of this level is required to reinstate a short-term bearish threat. On the upside, resistance and the bull trigger to watch is 121.73, the Jun 13 high. Clearance of this level would resume the uptrend.