MNI US Macro Weekly: Powell Widens Door To September Cut

Aug-22 16:55By: Chris Harrison and 1 more...

Federal Reserve+ 1

Download Full Report Here

- A dovish Powell at Jackson Hole acknowledged that "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance". Further, the risks appear to have shifted since the July meeting ("The balance of risks appears to be shifting"), as "downside risks to employment are rising”.

- It follows what had been a succession of on balance patient Fedspeak from FOMC members, including Cleveland Fed’s Hammack (’26 voter) explicitly saying she doesn’t see a cut next month.

- President Trump’s attack on the Fed has continued, saying he will fire Fed Governor Cook (in a permanent voting role through to 2038) if she doesn’t resign after FHFA accusations of mortgage fraud.

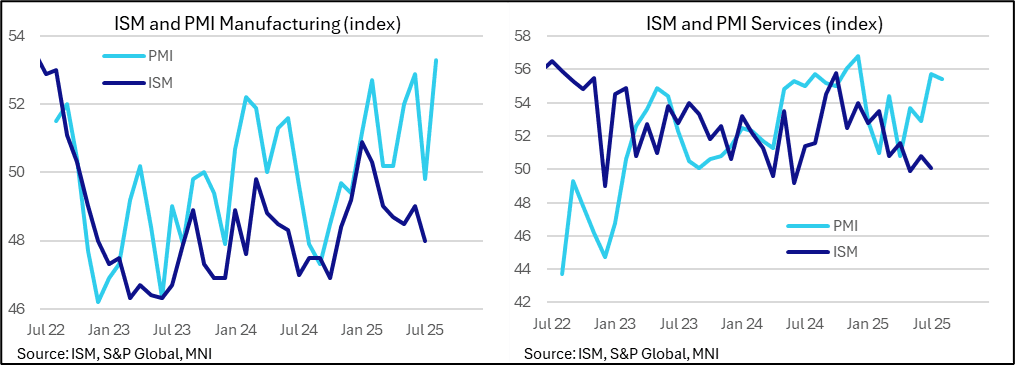

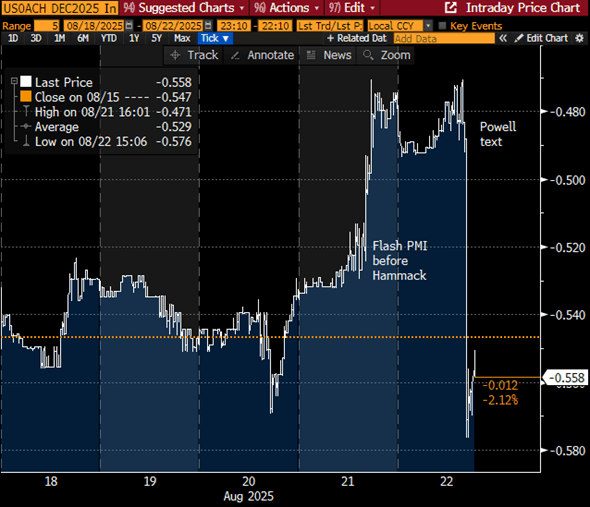

- The most notable data release of the week was a far stronger than expected flash PMI round for August, especially for manufacturing. That included composite service price inflation at a three-year high. There have however been large discrepancies with more subdued ISM readings in recent months.

- It was a relatively quiet week elsewhere for data. Weekly jobless claims data suggested a still “low fire” labor market but one that is arguably lower hire as continuing claims drift to fresh highs in recent weeks.

- Soft residential construction data point did however also drag latest GDPNow tracking for Q3, from 2.55% to 2.26% for real GDP growth.

- The CBO estimates that "changes in tariffs will reduce total deficits by $4.0 trillion altogether," over ten years. That compares to previous estimates from early June that it could decrease primary deficits by $2.5tn and interest outlays by $0.5tn.

- Powell’s remarks have seen Sept cut odds rise 3.5bp to 22bp and cumulative Dec cut odds rise 7.5bp to 55.5bp for little near-term change on the week after a hawkish shift mid-week. Dovish moves are more pronounced further out the curve however.

- Next week sees Q2 GDP/PCE revisions and the July PCE report in focus. Consumer spending is expected to see a reasonable increase for the start of Q3 whilst core PCE inflation should continue its above target stabilization.