MNI US OPEN - Narrow Margin in TN Adds to Dem's Optimism

EXECUTIVE SUMMARY

- KREMLIN SPOX DELIVERS MIXED MESSAGES ON OUTCOME OF PUTIN-WITKOFF TALKS

- TENNESSEE SPECIAL ELECTIONS ADDS TO DEMOCRATS' MIDTERM OPTIMISM

- AUSTRALIA Q3 GDP GROWTH BELOW EXPECTATIONS, BUT UNDERLYING DETAILS STRONG

- FARAGE TELLS DONORS HE EXPECTS REFORM UK TO DO AN ELECTION DEAL WITH TORIES

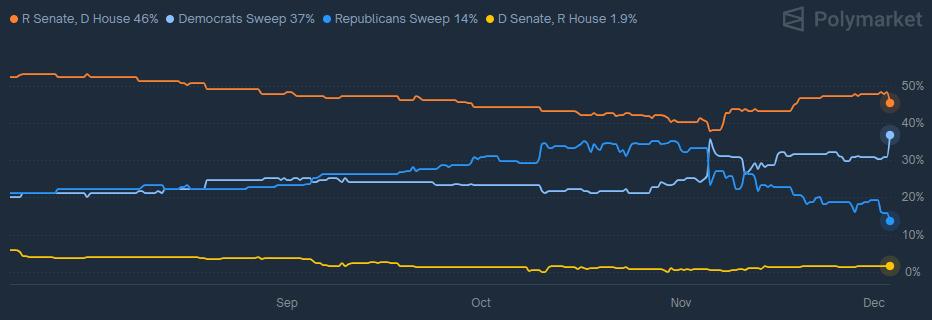

Figure 1: 2026 Midterms balance of power betting market odds

Source: Polymarket

NEWS

US/RUSSIA/UKRAINE (MNI): Kremlin Spox Delivers Mixed Messages on Outcome of Putin-Witkoff Talks

Reuters reporting comments from Kremlin spox Dmitry Peskov in which he appears to rule out any swift Ukraine peace deal, but also claim progress has been made. Says Ukraine peace plan talks "have a better chance of being productive if they are carried out without public commentary". Peskov repeats previous comments that Russia does not favour "megaphone diplomacy" [notable given President Vladimir Putin's very public sabre-rattling comments.

US/BRAZIL (BBG): Trump Says Brazil’s Lula Discussed Sanctions, Trade in Call

President Donald Trump said he spoke with his Brazilian counterpart, Luiz Inacio Lula da Silva, about sanctions the US imposed on officials from the South American country, a signal that relations between the two nations continue to improve. “We had a great talk. We talked about trade. We talked about sanctions, because, as you know, I sanctioned them having to do with certain things that took place. But we had a very good talk. I like him,” Trump told reporters on Tuesday at the White House.

US (MNI): Tennessee Special Elections Adds to Democrats' Midterm Optimism

Republican Matt Van Epps won a special election in Tennessee's 7th Congressional District. While the GOP avoided a shock loss - which appeared possible following a Democratic overperformance at off-year elections in November - the narrow margin of victory will increase Democratic optimism of flipping the House in 2026. Van Epps defeated Democratic state Rep. Aftyn Behn by a reported margin of 9 percentage points - considerably closer than the 20-plus percentage points margin of former Republican Rep. Mark Green and President Trump in 2024.

US/VENEZUELA (BBG): Rubio Casts Doubt on Maduro’s Ability to Honor Any Deal With US

Secretary of State Marco Rubio cast doubt on the possibility that the US could negotiate a deal with Nicolas Maduro to get him to stop drug traffickers, saying the Venezuelan leader has repeatedly broken commitments over the years. “If you wanted to make a deal with him, I don’t know how you do” that, Rubio said in an interview with Sean Hannity on Fox News on Tuesday night. “He’s broken every deal he’s ever made. Now, that doesn’t mean that you shouldn’t try.”

NATO (MNI): Foreign Mins Meet to Discuss Ukraine Peace Deal, Rubio Noticable Absentee

A meeting of NATO foreign ministers is underway in Brussels to discuss for the first time the nascent 20-point peace plan, which was put to Russian President Vladimir Putin on 2 December. Since the first leaks of the initial 28-point peace plan (seen as heavily favouring Russia), NATO has been largely sidelined from the negotiation process, with the US and Russia (and eventually Ukraine) the prime interlocutors.

UK (FT): Nigel Farage Tells Donors He Expects Reform UK to Do an Election Deal With Tories

Nigel Farage has told donors he expects a deal or merger between his Reform UK party and the Conservatives ahead of the next general election, suggesting he does not believe he can sweep to power alone. One donor said Farage told them he expected to do a deal with the Tories, whether it be a merger or an agreement on co-operation between the two parties, to ease Reform’s route to election victory. The person added that the Reform leader said such a deal could only be done on his terms, in part because Farage felt betrayed after the pact he made with the Tories at the 2019 election.

EU/RUSSIA (BBG): EU Finalizes Deal to Phase Out Russian Gas Imports by 2027

The European Union has reached a deal to phase out Russian gas faster than originally planned, a move that aims to finally sever ties between the bloc and its once-primary energy supplier. In the aftermath of the invasion of Ukraine, traders and energy companies have closely monitored the EU’s shift away from Russia toward alternative suppliers such as the US and the Middle East. But while Europe halved purchases after the war began in 2022, Russian gas has continued to account for roughly a fifth of imports.

RBA (MNI): RBA Says Still Needs to Work On Bringing Inflation “Sustainably” to Target

RBA Governor Bullock and Assistant Governor (Financial Markets) Kent have appeared before the Senate Economics Committee. There was little added to the November meeting's message that the persistence of Q3 inflation is being monitored but the RBA expects the quarterly CPI changes to moderate over coming quarters. Bullock did note that if the rise proves more persistent then it would signal higher demand pressures and that there would be implications for monetary policy.

JAPAN (BBG): Japan Metal Union Aims for Record Wage Hike as BOJ Watches Trend

A Japanese labor union group will push in annual negotiations for a salary hike that exceeds the record gain obtained in the previous round of talks, in the latest sign that pay momentum is holding up. The Japan Council of Metalworkers’ Unions called for a monthly base pay increase of at least ¥12,000 ($77) in negotiations that will run through March, according to a plan approved by its board on Wednesday. It’s the same initial target the group set a year ago as it began talks that culminated in a deal to increase pay this year by ¥10,169, the highest since it started setting a target for base salaries in 1998.

RUSSIA/CHINA (BBG): Russia Sells Debut Domestic Yuan Bonds to Fund Deficit

Russia sold its debut yuan-denominated sovereign bonds as the Kremlin continues to retool the sanctions-hit economy and seeks funding for a record fiscal shortfall this year. The Finance Ministry sold a total of 20 billion yuan ($2.8 billion) in two tranches of domestic, fixed-coupon bonds, according to a statement published late Tuesday.

DATA

EUROZONE NOV FINAL SERV PMI 53.6 (53.1 FLASH, 53.0 OCT) (MNI)

EUROZONE NOV FINAL COMP PMI 52.8 (52.4 FLASH, 52.5 OCT) (MNI)

GERMANY NOV FINAL SERV PMI 53.1 (52.7 FLASH, 54.6 OCT) (MNI)

FRANCE NOV FINAL SERV PMI 51.4 (50.8 FLASH, 48.0 OCT) (MNI)

SPAIN DATA (MNI): Services PMI Downside From External Sector; Rather Bright Elsewhere

- SPAIN NOV SERV PMI 55.6 (56.3 FCAST, 56.6 OCT)

That is a downside surprise for the Spain November Services PMI (at 55.6, vs 56.3 cons) after October's 56.6 which was the highest reading since December 2024. However, the release remains quite positive, seemingly assigning the main downside in November to international demand while the overall picture remains on the brighter side.

ITALY DATA (MNI): Services PMI Highest for 2 and a Half Years

- ITALY NOV SERV PMI 55.0 (53.9 FCAST, 54.0 OCT)

A strong Italian services PMI (in contrast to the weaker-than-expected Spanish number earlier), with the press release noting that this is the highest print for 2 and a half years. Other highlights from the npress release: "The improvement in total new order intakes was domestic-led, as export business returned to contraction in November following a month of growth."

UK DATA (MNI): MPC Doves Will Be Encouraged by Services PMI as Firms Don’t Pass On Costs

- UK NOV FINAL SERV PMI 51.3 (50.5 FLASH, 52.3 OCT)

There has been an upward revision to the services (and composite) UK PMIs, but the key thing for the MPC in our opinion will be that despite cost increases, services firms feel that they are constrained regarding their ability to pass on price increases so November prices charged were at their lowest increase in "just under five years." The doves will be encouraged by this, and it is another roadblock cleared ahead of the December MPC meeting. Tomorrow we will see DMP data.

SWITZERLAND DATA (MNI): CPI Details Confirms Downside Centred Around Housing/Hotels

- SWISS NOV CPI -0.2% M/M, +0.0% Y/Y

- SWISS NOV CORE CPI +0.4% Y/Y

- SWISS NOV SERVICES CPI +1.0% Y/Y

Looking at the details of the Swiss CPI print shows the following: Unrounded headline CPI was 0.02% (down from 0.10% in October, a 0.08ppt slowdown); housing rentals contributed -0.05pp to the change in headline CPI (this only updates quarterly and is likely to remain persistent); hospitality also contributed -0.05ppt to the change in headline CPI (coming from hotels, volatile package holidays playing only a minor part); food and energy both contributed around +0.02ppt each, to partially offset this.

AUSTRALIA DATA (MNI): Strong Domestic Demand Growth to Keep RBA Cautious

- AUSTRALIA Q3 GDP +2.1% Y/Y

- AUSTRALIA Q3 GDP +0.4% Q/Q

Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

CHINA DATA (MNI): Services PMI Moderates Again

After declining in October, the RatingDog PMI Services fell again in November. November's reading takes the index to mid-year levels. Within the release some positives were an uptick in employment to 49.2 from 49, yet remains in contraction for the fourth consecutive month. Prices charged were up relative to last month. When coupled with the RatingDog PMI Manufacturing, the PMI Composite fell to 51.2, the lowest since July.

TURKEY DATA (MNI): First Sub-1% Month-on-Month CPI Reading Since May 2023

- TURKEY NOV CPI +0.87% M/M

CPI inflation data for November came in well below expectations. M/M CPI moderated to +0.87% from +2.55% in October – below the +1.35% expected and the first sub-1% reading since May 2023 – while the annual figure came in at +31.07% Y/Y (Est: +31.60%; Prior: +32.87%). Core softened to +31.65% Y/Y from +32.05% (Est: +31.45%). As expected, softer fruit and vegetable prices drove much of the decline in inflation, with food and non-alcoholic beverages prices down 0.69% compared to October, contributing -0.17ppts to the total M/M figure.

FOREX: Greenback Tilts Lower Amid Risk Optimism/Hasset Chair Expectations

- The risk backdrop remains stable Wednesday, allowing the major indices and crypto markets to edge higher and provide a negative tilt to the US dollar. The greenback tone was also set late last night as President Trump’s nod towards Kevin Hassett potentially becoming the next Fed Chair confirms the dovish bias to market Fed pricing for 2026.

- These dynamics have prompted GBP and the Scandies to outperform on the session. For GBPUSD specifically, spot has edged to a fresh recovery and post-budget high, with momentum building on the better-than-expected PMI print. Prices are now meeting an uptrendline drawn off the Nov 13 high on the 15min candle chart - meaning further strength here could trigger more on the follow through. A close back above the 50-day EMA for cable would also be the first since early October. Mirroring the move, EURGBP has firmly rejected the test of 0.88 overnight, erasing the majority of Monday's rally.

- For EURUSD, we are currently testing above key resistance and the bull trigger at 1.1656. The moves come despite the latest Kremlin commentary pouring cold water on the prospects of a peace deal, with prediction markets' odds for a ceasefire by the end of '26 falling below 50%.

- Despite a weaker-than-expected Q3 GDP print, stronger domestic demand growth is likely to keep the RBA in cautious mode, underpinning the firm AUD recovery. Elsewhere, softer-than-expected Swiss CPI figures did little to move the Swiss needle.

- A wide set of US data is scheduled for today, including weekly MBA Mortgage Applications, November ADP, September import / export prices, September IP, and ISM Services.

BONDS: Off Early Highs

Core global FI markets have eased from early session highs, with firmer-than-expected services PMI data out of Europe & the UK noted.

- Bund futures +4 at 128.57. Initial support and resistance located at 128.12 & 128.72.

- German yields little changed to 1bp higher, curve marginally steeper.

- The 10-Year BTP/Bund spread threatens to break below 70bp, a level that has not been closed below since January ’10. Firmer than-expected Italian PMI data has factored into BTP outperformance.

- OATs hold yesterday’s widening.

- Gilt futures briefly rallied more than 60 ticks from yesterday’s low, topping out at 91.50 before fading back to ~91.30 last, still ~15 ticks higher on the day.

- Bulls remain in technical control, with our technical analyst deeming the recent pullback to be corrective. Initial support and resistance in the contract remain located at 90.87 & 91.93, respectively.

- Yields 1bp higher to 1bp lower, front end underperformed into the GBP4.75bln 4.00% May-29 gilt auction, which ultimately provided average results.

- SONIA futures within 1bp of yesterday’s closing levels, BoE-dated OIS still pricing over 80% odds of a rate cut later this month.

- Comments from ECB’s Lagarde, Lane & Dolenc are due today, with BoE’s Mann also due to speak (albeit with a focus on reserve currencies as opposed to outright monetary policy matters).

- U.S. ADP employment and ISM services data headline the macro calendar today.

EQUITIES: Climb Higher for Eurostoxx Futures Undermining a Bearish Theme

Recent gains in Eurostoxx 50 futures undermine a recent bearish theme and the contract is holding on to its gains. Price has cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. A continuation would open 5742.40 next, a Fibonacci retracement point. For bears, a reversal lower would instead expose the key short-term support and bear trigger at 5475.00, the Nov 21 low. First support lies at 5609.26, the 50-day EMA. S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed higher by 561.23 pts or +1.14% at 49864.68 and the TOPIX ended 6.74 pts lower or -0.2% at 3334.32.

- Elsewhere, in China the SHANGHAI closed lower by 19.712 pts or -0.51% at 3878 and the HANG SENG ended 334.32 pts lower or -1.28% at 25760.73.

- Across Europe, Germany's DAX trades higher by 98.65 pts or +0.42% at 23810.01, FTSE 100 lower by 3.13 pts or -0.03% at 9698.64, CAC 40 up 17.5 pts or +0.22% at 8092.11 and Euro Stoxx 50 up 32.34 pts or +0.57% at 5718.51.

- Dow Jones mini up 104 pts or +0.22% at 47648, S&P 500 mini up 12.25 pts or +0.18% at 6852.5, NASDAQ mini up 29.75 pts or +0.12% at 25634.75.

Time: 10:00 GMT

COMMODITIES: Recent Gains for WTI Futures Still Considered Corrective

Recent gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold is unchanged and remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4009.2. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.63 or +1.07% at $59.25

- Natural Gas up $0.11 or +2.21% at $4.946

- Gold spot down $4.55 or -0.11% at $4200.94

- Copper up $10.35 or +1.97% at $534.75

- Silver down $0.34 or -0.57% at $58.129

- Platinum down $5.14 or -0.31% at $1639.75

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services PMI (f) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies | ||

| 04/12/2025 | 0030/1130 | ** | Trade Balance | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0800/0900 | ** | Unemployment | |

| 04/12/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/12/2025 | 0930/0930 | BOE Decision Maker Panel Data | ||

| 04/12/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/12/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1700/1200 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending |