AUSTRALIA DATA: Strong Domestic Demand Growth To Keep RBA Cautious

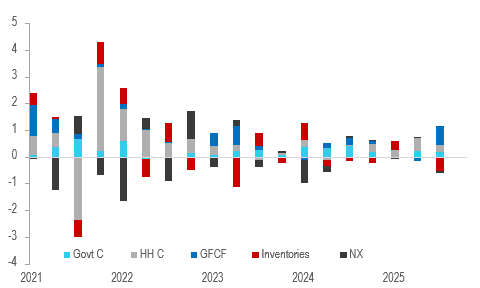

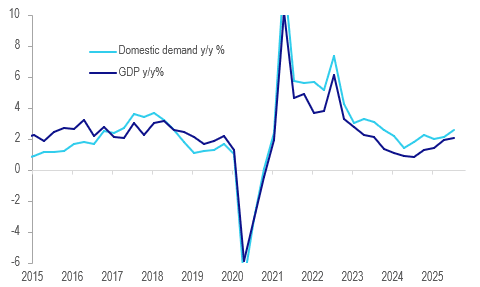

Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

Australia contributions to q/q GDP pp

Source: MNI - Market News/ABS

- In November, the RBA forecast Q4 GDP growth of 2.0% y/y. Excluding revisions, this would require a 0.5% q/q rise and so growth is developing as it expects. However, it has been around the bank’s estimate of trend and today Governor Bullock said that while the output gap size is uncertain, it probably has closed, which increases risks to inflation from stronger demand. Thus, rates are likely on hold for some time and domestic demand strength poses an upside risk to inflation.

- Private consumption rose 0.5% q/q, concentrated in essential spending, and contributed 0.3pp to quarter GDP. The savings rate rose 0.4pp to 6.4%. A 1.7% q/q increase in disposable income supported expenditure.

- Public consumption rose 0.8% q/q contributing 0.2pp.

- Investment was strong up 3.0% q/q contributing 0.7pp with 0.2pp from the public sector and 0.3pp from private machinery & equipment, which rose 7.6% q/q. Data centre development was a major driver.

- Strong import growth is consistent with stronger domestic demand and especially capex. Imports were up 1.5% q/q & 4.2% y/y after Q2’s 2.5% y/y. Exports were also solid at +1.0% & 3.6% but not enough to prevent net exports detracting 0.1pp.

- The statistical discrepancy made a -0.1pp contribution after Q2’s +0.2pp.

- GDP per capita was flat but up 0.4% y/y.

Australia GDP vs domestic demand y/y%

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNY at 7.0867 vs Estimate of 7.1192

The USD/CNY fix printed at 7.0867, versus prior outcome of 7.088. The fixing error widened to -325pips, from -201pips Friday. The fix has maintained a very stable bias over recent days, particularly given the Xi Trump meeting. USDCNH is at 7.1234, modestly weaker by -0.01%

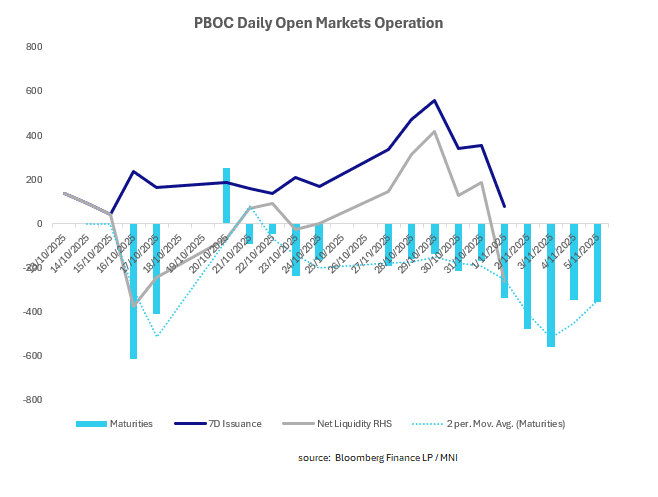

CHINA: Central Bank Withdraws CNY259bn via OMO

The stabilization of money markets and the grind lower in the 10-Yr was enough to bring about a withdrawal of liquidity via this morning's OMO despite a strong pipeline of maturities ahead.

- The PBOC issued CNY78.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY337.3bn.

- Net liquidity withdraws CNY259bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.45%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.35%.

The China 7-day interbank repo rate is at 1.42%, from the prior close of 1.46%.

MNI: CHINA PBOC CONDUCTS CNY78.3 BLN VIA 7-DAY REVERSE REPO MON

- CHINA PBOC CONDUCTS CNY78.3 BLN VIA 7-DAY REVERSE REPO MON