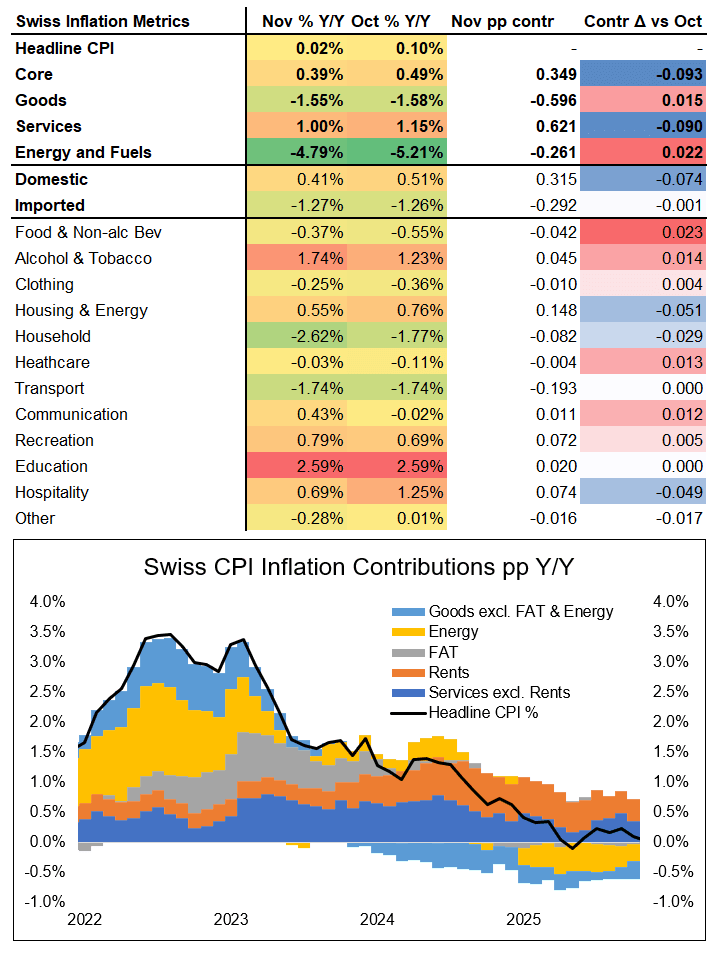

SWITZERLAND DATA: CPI Details Confirms Downside Centred Around Housing / Hotels

Looking at the details of the Swiss CPI print shows the following:

- Unrounded headline CPI was 0.02% (down from 0.10% in October, a 0.08ppt slowdown).

- Housing rentals contributed -0.05pp to the change in headline CPI (this only updates quarterly and is likely to remain persistent)

- Hospitality also contributed -0.05ppt to the change in headline CPI (coming from hotels, volatile package holidays playing only a minor part)

- Food and energy both contributed around +0.02ppt each, to partially offset this.

- These were the major drivers, for detailed calculations, see chart / table below.

What remains on net is a soft print which, while by itself is very unlikely to prompt an SNB cut into negative territory, warrants further monitoring. This applies especially as the downside this time was centred around domestic categories - which the SNB has flagged previously when looking at underlying inflationary pressures. Having said that, what's not quite so clear is their stance on the housing slowdown, with some previous comments suggesting that they merely view it as a lagged function of headline which may imply less feedthrough to policy. Also, we don't know what number they had pencilled in for rentals, either. So it's hard to know if this is the driver of the surprise, or if it is more broad based.

CHF saw a limited reaction to the release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: SPAIN OCT MANUF PMI 52.1 (51.9 FCAST, 51.5 SEP)

- MNI: SPAIN OCT MANUF PMI 52.1 (51.9 FCAST, 51.5 SEP)

EGBS: Bund Futures Slightly Weaker Through Open; Busy Week for Data

Bund futures trade slightly weaker through the European open, ahead of a notably busier week with ample data and, in particular, speakers. Technically, the main initial support is unchanged at 129.13, this was a resistance gap that held through mid September into October and is now marked as support. This level coincides with the 50-day EMA at the start of this week.

- Although not a technical level, the first upside area of interest is at circa 129.52 which would represent a reversal of the less dovish FOMC meeting last week - any break above the latter would see 129.73 as the next target, followed by 130.07.

- Today's manufacturing PMIs will be the final readings for France, Germany, EU, US and the UK, while the main focus will be on the US ISM Manufacturing. This print may take on additional importance given the persistence of the government shutdown and a lack of official US data.

- SUPPLY: EU 2031, 2035, 2054 (would equate to 56.4k Bund) could weigh into futures.

- SPEAKERS: ECB's Simkus, Lane, Escriva & Kocher. Fed's Daly & Cook.

SILVER TECHS: Trading Above Support

- RES 4: $56.153 2.500 proj of the Aug 20 - Sep 16 - 17 price swing

- RES 3: $55.444 2.382 proj of the Aug 20 - Sep 16 - 17 price swing

- RES 2: $55.000 - Round number resistance

- RES 1: $49.456/54.480 - High Oct 23 / 17 and the bull trigger

- PRICE: $49.052 @ 08:10 GMT Nov 3

- SUP 1: $45.963 - 50-day EMA

- SUP 2: $41.135 - Low Sep 17

- SUP 3: $40.000 - Round number support

- SUP 4: $38.087 - Low AUg 27

Trend signals in Silver are bullish and recent weakness is considered corrective. Note that the trend condition has recently been in overbought territory and the deeper retracement is allowing this to unwind. Support to watch is at the 50-day EMA, at $45.963. It remains intact, however, a break would signal scope for a deeper retracement. Key resistance has been defined at $54.480, the Oct 17 high. Initial resistance is $49.456, Oct 23 high.