MNI US OPEN - Modi and Putin Tout Closer Economic Ties

EXECUTIVE SUMMARY

- SCOTUS RULES IN FAVOUR OF NEW TEXAS CONGRESSIONAL MAP

- MODI AND PUTIN TOUT CLOSER ECONOMIC TIES

- BOJ IS SAID LIKELY TO HIKE THIS MONTH, STAY OPEN TO MORE MOVES: BBG

- STRONGER-THAN-EXPECTED FRANCE AND SPAIN IP, ENERGY THE KEY DRIVER

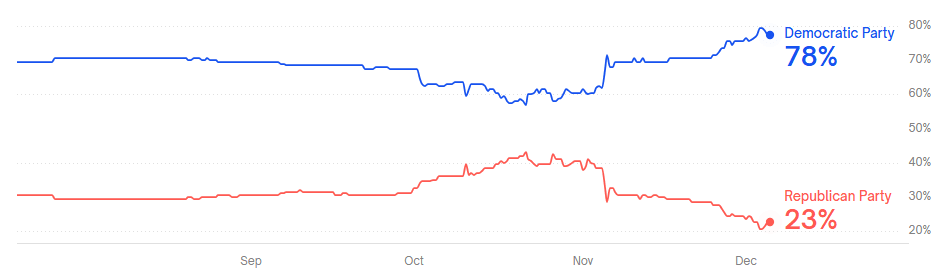

Figure 1: Which party will win the House in 2026?

Source: Polymarket

NEWS

US (MNI): SCOTUS Rules in Favour of Texas Congressional Map

The Supreme Court has ruled 6-3 in favour of a new Texas Congressional map that could net the GOP an additional five House seats at the 2026 midterm elections, overturning a lower court ruling blocking the map for racial gerrymandering. The decision, the first of the 'redistricting war,' suggests the Supreme Court is likely to defer to states in other pending cases, including a Republican challenge to a California map that was passed like a ballot initiative last month.

US (BBG): US Urged Europeans to Oppose EU Plan for Loan to Support Ukraine

The US lobbied several countries in the European Union in an effort to block EU plans to use frozen Russian central bank assets to back a massive loan to Ukraine, according to European diplomats familiar with the matter. US officials argued to member states that the assets are needed to help secure a peace deal between Kyiv and Moscow and should not be used to prolong the war, said the diplomats, who spoke on the condition of anonymity.

US/MEXICO (BBG): Trump, Sheinbaum to Meet for First Time at World Cup Event

Mexico President Claudia Sheinbaum said she will hold a short in-person meeting with Donald Trump this week in Washington, as they continue to negotiate over US tariffs on her nation’s goods. Their first face-to-face encounter will take place Friday, Sheinbaum confirmed during her daily press briefing Thursday. Sheinbaum will also meet with Canadian Prime Minister Mark Carney in Washington, where the leaders are set to attend the draw for the 2026 FIFA World Cup hosted by the three North American nations.

RUSSIA/INDIA (MNI): Modi and Putin Tout Closer Economic Ties

Reuters reporting comments from Russian President Vladimir Putin on day two of his first trip to India since the start of the Ukraine war. The trip appears primarily designed to bolster Russia's decades-long strategic relationship with India amid efforts by the Trump administration to curb Russia's oil exports to India and a long-standing strategy by successive US administrations to bring India closer to the West. Putin described talks with Indian colleagues and a meeting with Prime Minister Narendra Modi as "useful," adding that "numerous agreements [were] signed today aimed [at] strengthening cooperation with India." Putin said, "Russia is ready to provide uninterrupted fuel supplies to India."

GERMANY (BBG): Merz’s Coalition on Edge Ahead of Crunch German Pension Vote

Chancellor Friedrich Merz’s ruling coalition with the Social Democrats faces a key vote in parliament on Friday that could precipitate its demise only seven months into its four-year term. A group of about 18 younger lawmakers from the conservative leader’s own party has rebelled against the government’s pension bill, which is due to go to a final ballot in the Bundestag at around 12:30 p.m. in Berlin. Although it’s unclear how many of them might reject the law, it threatens to wipe out the coalition’s majority of just 12 seats and deal another blow to Merz’s credibility.

FRANCE (MNI): National Assembly to Vote on Revenue Section of PLFSS Today

The French National Assembly will vote on the revenue section 2026 Social Security (PLFSS) bill today. This will be an important barometer ahead of next Tuesday's vote on the full PLFSS. If the PLFSS fails, the more controversial draft State Financing Bill (PLF) will be seen as effectively defeated as well. Uncertainty around the outcome of budget negotiations has kept a political risk premium embedded in OATs, with the 10-year OAT/Bund spread unable to test 70bps during recent narrowing episodes.

BOJ (BBG): BOJ Is Said Likely to Hike This Month, Stay Open to More Moves

Bank of Japan officials are ready to raise interest rates at a policy meeting later this month, provided there’s no major shock to the economy or financial markets in the meantime, according to people familiar with the matter. The central bank will also indicate it will continue to raise rates if its economic outlook is realized while remaining cautious on how far they will eventually push rates up, the people said.

BOJ (MNI EXCLUSIVE): Concerns Grow Over Takaichi's BOJ Board Picks

MNI discusses PM Takaichi's future BOJ board picks. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI EXCLUSIVE): China's Positive 2026 Policy Tone Aimed at 5% GDP

Policy advisors explain China's 2026 GDP growth strategy. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI EXCLUSIVE): China to Target City Specific Near-term Housing Stimulus

Advisors share their China property outlook ahead of next week's CEWC meeting. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBA (MNI EXCLUSIVE): Future RBA Adjustments Seen as Minor Tweaks to 3.6% Rate

Former RBA economists share their cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBI (MNI): RBI Cuts Rates by 25bps, Announces Plans to Support Liquidity

The Reserve Bank of India (RBI) announced that it has cut the repo rate by 25 basis points to 5.25% to support economic growth, particularly in light of global uncertainties. This marks the first rate reduction following pauses in August and October 2025 with the stance going forward now neutral. In a bid to support liquidity, the RBI announced a bond purchase of up to INR1 trillion and a 3-year USD/INR FX swap of $5 billion. The announcements come as a broader approach to improving liquidity and rupee stability. The additional aim is to reduce borrowing costs for the Modi government as it follows with its aggressive growth plans.

DATA

EUROZONE Q3 GDP +0.3% Q/Q, +1.4% Y/Y (VS +0.1% Q/Q, +1.6% Y/Y Q2) (MNI)

EUROZONE DATA (MNI): Stronger Than Expected France and Spain IP, Energy the Key Driver

Both French and Spanish industrial production came in firmer than expected, with energy (specifically electricity and gas in France) driving growth in both. In France, the "Other transport equipment" category again saw strong growth to help the headline rate, offsetting a decline in the automobile industry. France IP came in at 0.2% M/M for October (-0.1% cons, 0.7% prior, revised down 0.1ppt) and 1.7% Y/Y (1.3% cons, 1.3% prior). Spain IP grew 0.7% M/M (0.5% cons, 0.4% prior, revised down 0.1ppt), and 1.2% Y/Y (0.5% cons, 1.5% prior, revised down 2ppts).

FRANCE OCT INDUSTRIAL PRODUCTION 1.7% Y/Y (MNI)

FRANCE OCT INDUSTRIAL PRODUCTION 0.2% M/M (MNI)

FRANCE OCT MANUFACTURING PROD 1.5% Y/Y (MNI)

FRANCE OCT MANUFACTURING PROD -0.1% M/M (MNI)

GERMANY DATA (MNI): October Factory Orders Helped by Large One-Off; Sep Revision

- GERMANY OCT FACTORY ORDERS +1.5% M/M (VS +2.0% SEP)

October German factory orders come in above consensus, helped by a (seemingly domestic, transport/military) one-off as the core reading also sees some gains but is a little more contained. An upward September revision is also a net-positive. "When large-scale orders are excluded, new orders were 0.5% higher than in the previous month. The less volatile three-month on three-month comparison showed that new orders in the period from August 2025 to October 2025 were 0.5% lower than in the previous three months; when large-scale orders are excluded, new orders were down 0.1%.", Destatis comments.

UK DATA (MNI): Pre-Budget Caution, Wet Weather Drive Seventh Straight Footfall Decline

UK footfall decreased 0.8% Y/Y in November, after -0.7% in October, per the BRC's footfall monitor. This marks the seventh consecutive year-on-year decline, with the BRC highlighting wetter weather and pre-Budget caution causing consumers to hold off purchases in November. However, this may have been at least partly offset if it drove up online purchases (which would impact headline retail sales measures), and it may be that the Budget delayed some Christmas shopping into December. This release covers 2-29 November, the same four weeks as the upcoming BRC retail sales (9 Dec) and the ONS's retail sales data (19 Dec). It therefore includes Black Friday and the following Saturday but the Sunday and Cyber Monday will be covered by December data.

NORWAY DATA (MNI): Manufacturing IP Momentum Fading In Line With Surveys

Manufacturing industrial momentum has fallen in line with the signals from Statistics Norway's industrial confidence survey. There are other data that are more consequential for Norges Bank than industrial production, but it still fits with the theme of a modest softening in domestic demand. Next week's data are very important, with November CPI and the Q4 Regional Network Survey due. Manufacturing IP fell 0.9% M/M in October, with a 3m/3m growth at -0.4% for two consecutive months. Although headline IP fell 2.8% M/M (vs +3.7% prior), 3m/3m growth is still positive at 3.4% (vs 2.7% prior).

RATINGS: DBRS on Austria Headlines After the Close

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Fitch on Austria (current rating: AA; Outlook Stable), Belgium (current rating: A+; Outlook Stable), Estonia (current rating: A+; Outlook Stable) & Hungary (current rating: BBB; Outlook Stable)

- Moody’s on Norway (current rating: Aaa; Outlook Stable) & South Africa (current rating: Ba2; Outlook Stable)

- S&P on Germany (current rating: AAA; Outlook Stable), Malta (current rating: A-; Outlook Stable) & Sweden (current rating: AAA; Outlook Stable)

- Morningstar DBRS on Austria (current rating: AAA, Negative Trend), Estonia (current rating: AA (low), Stable Trend) & Hungary (current rating: BBB, Stable Trend)

- Scope Ratings on Slovakia (current rating: A; Outlook Negative)

FOREX: USDJPY Prints Pullback Lows, AUD Extends Higher Highs Streak

- USDJPY saw renewed volatility overnight, setting fresh pullback lows at 154.35 before recovering back up around the 155.0 handle. This came despite weak Japanese household spending data being a sign of fragile domestic demand, with consolidating expectations for a BoJ hike at the Dec 18-19 meeting holding sway in the short term.

- The current retracement in USDJPY is allowing a recent overbought condition to unwind. The recent extension lower exposes the 50-day EMA, currently intersecting at 153.41. USD1.94b of options expire today at 155.0, which could act as a magnet as we approach the NY cut.

- AUDUSD continues its slow but steady ascent, trading further above the late October highs of 0.6618 to reach an intra-day peak of 0.6635. The pair has now posted 10 consecutive sessions of higher highs, as the bullish impulsive wave extends. With a number of resistance points being cleared, targets on the topside are now found at 0.6660 (Sep 18 high) and 0.6723, the Oct 21 2024 high.

- German Chancellor Merz is travelling to Belgium today to push for the backing of a loan to the Ukraine with frozen Russian assets. While the US has reportedly lobbied against such a setup, an agreement between European countries on the deal would strengthen Ukraine's position in current negotiations, and hence be EUR-supportive. EURUSD will be monitoring a weekly close above 1.1656 resistance, that has been pierced this week.

- September PCE data will headline the data calendar for today, with Michigan sentiment to be published simultaneously. Canadian November employment data is also due, while ECB's Villeroy and Lane are scheduled to speak.

EGBS: Bund Futures in Bear-Mode Cycle, Important Bundestag Vote Due Soon

- Bund futures remain in a bear-mode cycle. Futures are -7 ticks today at 128.33, off lows of 128.29. Initial support is 128.18, a Fibonacci projection level.

- There will be interest in the outcome today’s German pension system vote, expected in the next hour. Chancellor Merz's coalition holds a very narrow majority, and 18 younger CDU lawmakers have voiced opposition to the reforms. Merz may still be able to get the vote through the Bundestag, but is reliant on an abstention from Die Linke.

- 10-year Bund yields briefly tested 2.78% earlier, clearance of which would expose the 2.80% figure. Bund yields are now in line with our linear fair value model, while analyst views are tilted in favour of further increases through next year. Intraday, the German curve has seen a horizontal 0.5bp shift higher.

- 10-year EGB spreads to Bunds are biased a touch narrower, with BTP/Bund consolidating below the 70bp figure. 10-year OAT/Bund is at 74.5bps, with focus on today’s National Assembly vote on the Revenue section of the 2026 Social Security budget.

- The final read of Eurozone Q3 GDP was revised up a tenth on a rounded basis to 0.3% Q/Q. Underlying domestic demand details look solid, while compensation per employee growth also surprised to the upside. The market impact was limited, but it’s a hawkish set of data for the ECB.

- French/Spanish industrial production and Italian retail sales also surprised to the upside today.

- In North America, US PCE and Canadian labour market data are due this afternoon.

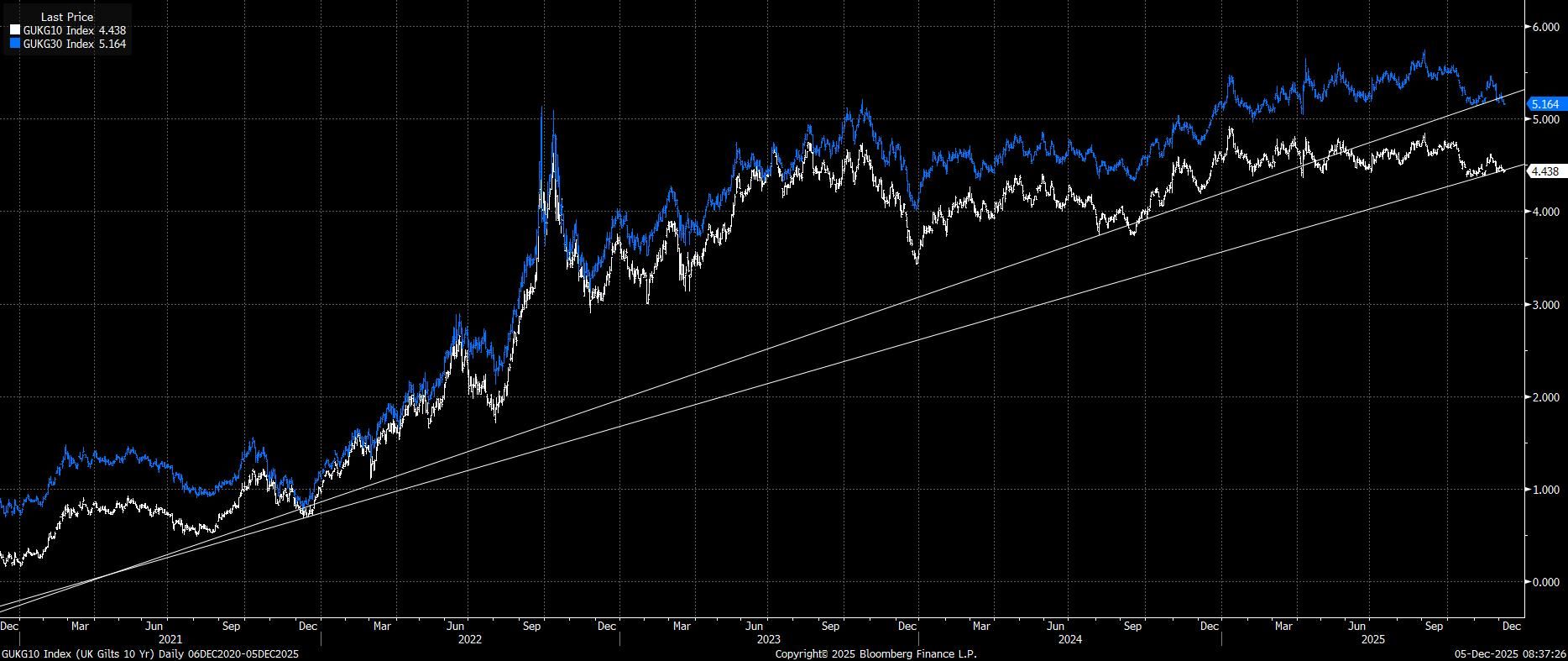

GILTS: Little Changed, Long End Yields Eying Clean Break Below M-Term Supports

Gilts initially opened a little lower on ongoing bearish cues from EGBs, before wider stabilisation in core global FI markets limits losses.

- Futures last -3 at 91.69 vs. session lows of 91.63.

- Bulls remain in technical control with the recent pullback deemed corrective by our technical analyst.

- Initial support and resistance in futures located at 90.87 & 91.93.

- Yields essentially unchanged across the curve.

- November lows are intact across benchmark yields.

- Note that both 10- and 30-Year yields are threatening clean breaks below uptrend support drawn off their December ’21 lows (see chart below).

- Ongoing skew away from long end issuance by the DMO, a wider-than-expected fiscal buffer and the reduction in UK fiscal and political risk premia has promoted curve flattening post-Budget.

- This has also generated outperformance vs. Bunds, with the 10-Year spread now nearly 25bp below mid-November closing highs, threatening a break below 165bp. Next support located at the September ’24 low (162.01bp).

- The release of the DMO’s FQ4 operation schedule generally matched our expectations (see previous bullets for greater detail).

- Little of note on the UK calendar ahead of the weekend.

Figure 2: UK 10- & 30-Year Yields (%)

Source: MNI, Bloomberg Finance L.P.

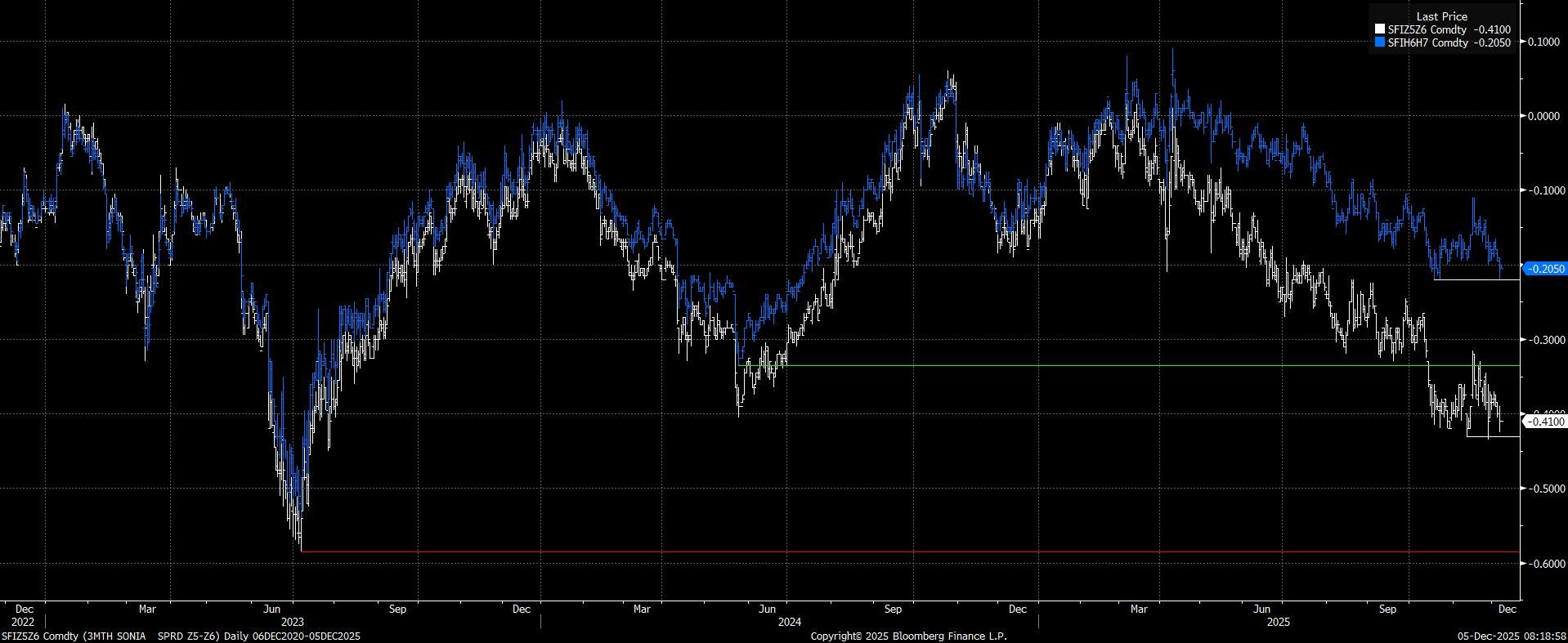

STIR: Recent Lows Holding in Front SONIA 12-Month Spreads

Pre-existing cycle lows in SFIZ5/Z6 and SFIH6/H7 (-43.0 & -22.0, respectively) continue to provide support despite the recent flattening of the strip amid firmer odds of a Dec BoE rate cut, with any breaches proving short-lived and limited in nature.

- A break lower would expose ’23 lows in SFIZ5/Z6 (-58.5) & ’24 lows in SFIH6/H7 (-33.5)

- Potential catalysts for a fresh dovish move include dovish messaging alongside the almost fully discounted December BoE rate cut, further deterioration in labour market data (as seen in yesterday’s BoE DMP survey) and swifter than envisaged progress towards the Bank’s inflation target.

Figure 3: SONIA Dec ‘25/Dec ’26 (SFIZ5/Z6) & Mar ‘26//Mar ’27 (SFIH6/H7) Spreads

Source: MNI, Bloomberg Finance L.P.

EQUITIES: Bullish E-Mini S&P Theme Intact, Contract Above 20-, 50-Day EMAs

A bull cycle in Eurostoxx 50 futures remains intact. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), the 76.4% retracement of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5617.30, the 50-day EMA. A bullish theme in S&P E-Minis is intact and the contract continues to appreciate. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6788.55, the 20-day EMA.

- Japan's NIKKEI closed lower by 536.55 pts or -1.05% at 50491.87 and the TOPIX ended 35.65 pts lower or -1.05% at 3362.56.

- Elsewhere, in China the SHANGHAI closed higher by 27.015 pts or +0.7% at 3902.808 and the HANG SENG ended 149.18 pts higher or +0.58% at 26085.08.

- Across Europe, Germany's DAX trades higher by 98.49 pts or +0.41% at 23980.46, FTSE 100 higher by 17.23 pts or +0.18% at 9727.86, CAC 40 up 20.89 pts or +0.26% at 8142.92 and Euro Stoxx 50 up 15.44 pts or +0.27% at 5733.52.

- Dow Jones mini down 13 pts or -0.03% at 47903, S&P 500 mini up 11.5 pts or +0.17% at 6878.25, NASDAQ mini up 91.75 pts or +0.36% at 25715.25.

Time: 10:00 GMT

COMMODITIES: Gold Key Resistance and Bull Trigger Marked at $4381.52

Short-term gains in WTI futures appear corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend needle in Gold continues to point north. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4024.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.06 or +0.1% at $59.74

- Natural Gas down $0.03 or -0.53% at $5.034

- Gold spot up $17.27 or +0.41% at $4225.63

- Copper up $8.25 or +1.54% at $545.35

- Silver up $1.06 or +1.86% at $58.21

- Platinum up $14.68 or +0.89% at $1660.81

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit | |

| 08/12/2025 | 2330/0830 | ** | Average Wages (p) | |

| 08/12/2025 | 2350/0850 | Balance of Payments | ||

| 08/12/2025 | 2350/0850 | *** | GDP |