MNI US OPEN - Markets Remain Highly Sensitive to Iran Newsflow

EXECUTIVE SUMMARY

- PRO-AMERICAN KURDISH FORCES ARE PREPARING POSSIBLE IRAN INCURSION: NYT

- IRAN TO CHOOSE NEW SUPREME LEADER ‘AS SOON AS POSSIBLE’

- CHINA SETS LOWEST ANNUAL GDP TARGET SINCE 1991

- BOJ IS SAID TO KEEP APRIL HIKE ON TABLE WITH EYES ON IRAN CRISIS: BBG

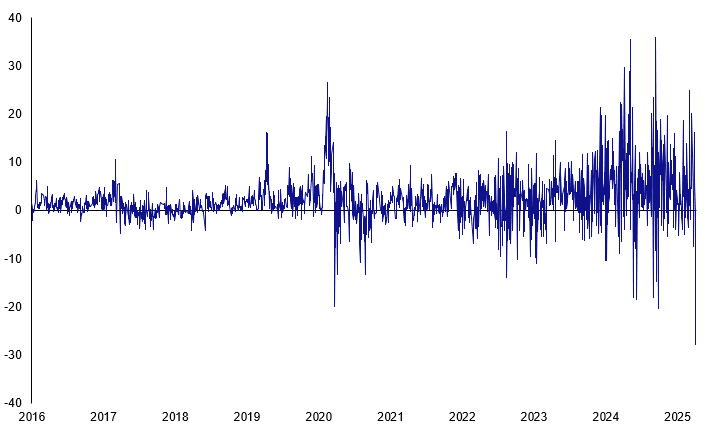

Figure 1: Net Daily China-Hong Kong Stock Connect Southbound Flows (HK$)

Source: MNI, Bloomberg Finance L.P.

NEWS

US/IRAN (NYT): Pro-American Kurdish Forces Are Preparing Possible Iran Incursion

Pro-American, Iranian Kurdish forces based in Iraq are preparing armed units that could enter Iran, creating a potential new front in an already expanding conflict, according to Iraqi officials and senior members of Iranian Kurdish groups. The C.I.A. has previously given small arms to the Iranian Kurdish forces as part of a covert program to destabilize Iran, an effort that began before the current war, according to people familiar with the effort. But in a briefing on Wednesday, Karoline Leavitt, the White House press secretary, said reports that President Trump had agreed to any plan for the Kurds to launch an insurgency in Iran were “completely false.”

US/IRAN (MNI): Markets React to Potentially Misinterpreted Headline on Iran Abandoning Nuclear Program

Sky News Arabia's official X account (translated from Arabic): "Iranian Deputy Foreign Minister: Iran is ready to abandon its nuclear program on condition that the United States presents a satisfactory alternative offer." That was not confirmed by any other wires or sources - but it triggered some upside in bonds and downside in oil prices. Bloomberg then ran the following headline citing a "deputy minister", presumably the same individual as the Sky Arabia report: “Iran had sought 'something good in return': state-run IRNA”. The key part here is timing: numerous networks are running the Sky News Arabia report which, when translated, appears to be referring to proposals made AFTER the attack, but these very similar IRNA headlines seem to be referring to the pre-attack talks. It may therefore be the case that markets moved on a misinterpretation of the Sky News Arabia headlines.

US/IRAN (BBG): Iran Says It Struck US Oil Tanker in Persian Gulf: State TV

The oil tanker was struck in the northern Persian Gulf early Thursday by the Islamic Revolutionary Guard Corps navy, Iran’s state-run TV reports. IRGC claims the tanker is on fire. Says Iran previously warned that military and commercial vessels belonging to the US, Israel and European countries, as well as their supporters, would not be allowed to transit and would be struck if detected.

IRAN (BBG): Iran to Choose New Supreme Leader ‘as Soon as Possible’: Mehr

Iran’s Assembly of Experts is carrying out its duty to choose a new supreme leader “as soon as possible,” Iran’s semi-official Mehr cites assembly member Mohsen Qomi as saying. “The process of selecting the new leader is being completed according to constitutional principles.” Says speculation circulating online about the process is “unfounded,” without elaborating.

ECB (BBG): ECB’s Villeroy Sees No Reason Now to Raise Interest Rates

The European Central Bank has no reason to raise interest rates as of today in response to higher oil prices due to the war in Iran, Governing Council member Francois Villeroy de Galhau said. The Bank of France governor said policymakers are following energy prices and developments on financial markets very closely and will have a much more detailed economic assessment at their next rate-setting meeting in two weeks. “Everything will depend on the duration of the conflict, whether it’s a temporary phenomenon or a lasting phenomenon of rising prices,” he said on France Inter radio on Thursday.

ECB (MNI): Gulf Crisis Has Raised Uncertainty - ECB's Guindos

Financial markets have so far behaved in an "orderly" way following the outbreak of conflict in the Middle East, ECB Vice President Luis de Guindos said at an event in Brussels Thursday. But the crisis has "raised the level of uncertainty" from a sitiuation where the balance of risks on inflation had been balanced and the ECB had been in a "good place", adding that he now thinks "you have to go to a different approach". The baseline scenario of the ECB was for a short-lived conflict, he said, but it could also prove to be more protracted, in which case there was a danger that inflation expectations could start to rise.

ECB (BBG): Length, Extent of War to Determine Knock-on Effects - ECB's Rehn

European Central Bank Governing Council member Olli Rehn says the duration, as well as the “extent and breadth,” of the Iran war will determine the effect on Europe’s economy. Conflict could boost inflation in the short term while weighing on economic growth. Reiterates that cool heads are needed to assess impact on Europe’s economy.

UK (The Times): You’ve Failed Us on Iran, Middle East Allies Tell UK

Britain’s allies in the Gulf and Cyprus have accused Sir Keir Starmer of failing to do enough to protect the region and UK citizens from Iranian missile strikes. The Times has been told that Bahrain and the United Arab Emirates have concerns about the UK’s response to the Middle East conflict. At the same time Cyprus’s high commissioner to the UK said the “least” his country expected was for the government to provide a robust defence of the island that is home to two British bases.

CHINA (MNI): China Sets Lowest Annual GDP Target Since 1991

MNI (Beijing) China has set its 2026 economic growth target range at 4.5% to 5%, marking the weakest expansion goal since 1991 and aligning with MNI’s earlier report as well as market expectations. The lower target signals policymakers’ greater tolerance for slower growth as they prioritise economic restructuring over short-term stimulus. Chinese economists told MNI that, amid persistent downward pressure, 2026 GDP growth is likely to come in around 4.8% year-on-year.

CHINA (BBG): China Tells Top Refiners to Halt Diesel and Gasoline Exports

China’s government has told the country’s largest oil refiners to suspend exports of diesel and gasoline as an escalating conflict in the Persian Gulf disrupts the arrival of crude from one of the world’s largest producing regions. Officials from the National Development and Reform Commission, the country’s top economic planner, met refinery executives and verbally called for a temporary suspension of refined product shipments that would begin immediately, according to people familiar with the matter. They asked not to be named as the discussions are not public.

CHINA (MNI): PBOC to Maintain Accommodative Policy Stance - NPC

MNI (Beijing) China will maintain a moderately accommodative monetary stance, take measures to stabilise inflation, and implement structural innovations in key sectors, according to the Government Work Report delivered by Premier Li Qiang during the opening session of the National People's Congress in Beijing on Thursday. The central bank will use a variety of tools “flexibly and efficiently,” including required reserve ratio (RRR) cuts and interest rate reductions, while maintaining ample liquidity and expanding structural facilities, Li said. Authorities aim to keep social financing costs low and maintain the basic stability of the yuan at a “reasonable and balanced level.”

CHINA (MNI): China Keeps Fiscal Expansion Similar to 2025 - NPC

MNI (Beijing) China will continue to implement a more proactive fiscal policy in 2026, keeping fiscal expansion roughly in line with last year though falling short of market expectations. The deficit-to-GDP ratio is set at around 4%, allowing for a government deficit of CNY5.89 trillion, CNY230 billion higher than last year, according to the Government Work Report delivered by Premier Li Qiang during the opening session of the National People's Congress in Beijing on Thursday.

BOJ (BBG): BOJ Is Said to Keep April Hike on Table With Eyes on Iran Crisis

Bank of Japan officials are still on track to raise interest rates, with the possibility of April not ruled out, as they continue to monitor the implications of Middle East tensions for Japan’s economy, according to people familiar with the matter. While officials see little chance of a rate hike at the policy meeting ending March 19, they have so far not altered their stance of proceeding with rate increases if the economic outlook evolves as expected, the people said. Officials view the duration of the conflict as the key variable in assessing risks to Japan’s economic outlook and the trajectory of interest rates, the people said.

BOJ (MNI EXCLUSIVE): BOJ's Tightrope Walk Complicates Rate Strategy

MNI discusses the BOJ's challenges ahead as it navigates an impending oil supply shock. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (MNI): Rengo Tables Firm Wage Hike Request

Japan's largest labour union body, Rengo, has noted that member unions are seeking an average wage hike of 5.94% in this year's Shunto wage negotiations, just below the 6.09% it started with last year. Unions representing smaller companies demanded a 6.64% raise, the largest request since at least '24 (6.57% last year). According to Rengo, the weighted average of wage increases in the 2025 shunto round was 5.25%, topping 5% for the second consecutive year. Policymakers use the outcome as a key input for policy settings.

RBA (MNI EXCLUSIVE): Behind-Curve RBA to Wait Till May Before Hike - Ex Staffers

Former RBA staffers look at its reaction to the oil price surge and its likely next moves. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

UK DATA (MNI): Little in the DMP Data to Swap Any MPC Member's Vote

- UK BOE DMP FEB 1-YEAR WAGE EXP 3M AVG 3.56% (3.60% JAN); SGL MO 3.52% (3.49% JAN)

The big picture in the DMP data is that it paints a very similar picture to last month's report. There isn't likely to be anything in here that will sway any MPC member's vote. Wages: UK 1-year ahead wage expectations were broadly in line with last month while realised wage growth was higher on the single month (but showed a marginal slowdown on the 3-month average measure. Employment: Both expected and realised a bit higher than previously on the 3-month measure, but the single month realised measure was still low at -0.71%Y/Y. CPI expectations: Both 1/3-year ahead lower than previously on the 3-month measure (but the single month measures are both marginally higher than in Jan).

FRANCE DATA (MNI): IP Positive Almost Solely Due to Transport Equipment Rebound

- FRANCE JAN IND PROD 2.4% Y/Y (1.6% DEC, REV FROM 1.7%)

- FRANCE JAN IND PROD 0.5% M/M (-0.5% DEC, REV FROM -0.7%)

- FRANCE JAN MANUF PROD 2.7% Y/Y (2.1% DEC)

- FRANCE JAN MANUF PROD 0.6% M/M (-0.7% DEC, REV FROM -0.8%)

France IP rebounded in Jan at 0.5% M/M (0.4% cons, -0.5% prior, revised up 0.2ppt), but almost entirely due to a strong rebound in transport equipment (all other manufacturing categories saw negative growth M/M). INSEE notes "Over the course of a month, manufacturing output rebounded solely due to the recovery in the manufacture of transport equipment. In January 2026, manufacturing output rebounded, driven solely by the sharp increase in the manufacture of transport equipment (+9.9% after -12.8%), particularly in other transport equipment (+19.1% after -20.1%) and more specifically in the aerospace industry."

SWEDEN DATA (MNI): Food and Goods Drive Downside Surprise, Jansson Likely to Support Cut

- SWEDEN FEB FLASH CPIF 1.71% (2.00% JAN)

- SWEDEN FEB FLASH CPIF-XE 1.38% (1.72% JAN)

Looking at the details of the flash report - newly released as of February - goods and food were the primary downside driver of the soft CPIF ex-energy reading. It seems likely that Riksbank Deputy Governor Jansson will vote for a cut at the March decision, but we are less sure on the other members. We still think some activity weakness is likely needed for Thedeen/Seim to support another cut, for example. The recent developments in energy markets (and the impact it could have on inflation expectations) may provide another argument to hold steady on March 19. That said, the uncertainty shock stemming from the conflict could also be portrayed as a dovish development if the Riksbank becomes concerned about the household consumption outlook.

JAPAN DATA (MNI): Offshore Inflows Continue Into Local Bonds & Stocks

Offshore investors continue to shift funds into both Japan bonds and equities, continuing recent trends. Year to date net inflows into Japan bonds are now over 7.6trln, while for equities we near 6.4trln, but we haven't had a negative week of net selling (in equities) since mid Dec 2025. Elevated yields may continue to be appealing to offshore investors in the JGB space, while local equities have dipped sharply since the end of last week (post the Iran conflict and oil price spike). This week's flow update should provide guidance on whether offshore investor sentiment has been shaken.

AUSTRALIA DATA (MNI): Jan Household Spending Lower Than Forecast, Y/Y Back Under 5%

Australia household spend for Jan was a little weaker than forecast. The m/m print rose 0.3%m/m versus 0.4% forecast, while the Dec outcome was to a -0.5% fall (after originally reported as a -0.4% decline). This saw the y/y outcome print at 4.6%, versus 5.1% forecast and 5.0% prior. This comes after yesterday's national accounts, which showed some slowing in household consumption growth.

AUSTRALIA JAN TRADE BALANCE A$+2631 (MNI)

NEW ZEALAND DATA (MNI): Q4 Building Volume Work Falls, Below Forecasts, Q3 Rise Revised

New Zealand Q4 volume of buildings work fell -3.1%q/q, against a 1.9% forecast rise. The prior Q3 outcome was revised down to a 0.2% rise, originally reported as a 1.5% gain. The level of building work volume is now back to mid 2020 levels, although the rate of decline in y/y terms is moderating. We printed at -4.8%, from -6.7% prior for this series. At the margin, lack of upside momentum in the construction side of the economy should give the RBNZ confidence around core inflation pressures remaining contained. We will get more partials for NZ Q4 GDP next Thursday, when manufacturing activity is due. Note that Q4 GDP prints on March 19.

FOREX: US Dollar Maintaining Bullish Tilt

- Some renewed pressure on risk sentiment and upside for crude futures Thursday is assisting the US dollar to maintain its bullish tone this week. A moderate bump higher for the DXY today keeps the week’s advance at 1.35%, with the index hovering just below the 99.00 mark. A strike on a Kuwait tanker may still be weighing on risk overall, despite an offsetting boost surrounding an unclear headline on Iran abandoning its nuclear program.

- AUDUSD has continued to exhibit notable volatility on Thursday, already trading in a 1.11% range on the session, and currently down 0.44% on the session. Despite this, bullish conditions remain intact after support at the 50-day EMA held Tuesday, intersecting at 0.6931. Short-term parameters for the pair are well defined, with a cluster of significant resistance building between 0.7125-50. Potential positive news around the Strait of Hormuz may be required for a convincing move above that cluster as AUD's risk sensitivity would add to Australia's significant exposure to flows through the straight in such a case.

- EURCHF continues to trade with a bearish tilt on Thursday, slipping to a session low of 0.9050 in recent trade, and eroding the week’s prior rally that was assisted by SNB commentary on a higher readiness to intervene. The phrasing of ‘would jeopardize’ perhaps places a greater emphasis on the importance of this week's cycle lows at 0.9025, with moves below this level likely to be met with additional central bank rhetoric, or active intervention.

- Both EUR and JPY are trading in line with the adjustments for the dollar, with EURUSD remaining steady just above the 1.16 handle. GBP is a small underperformer, sliding back towards the 1.33 mark.

- The US data calendar is heavy today, with Challenger Job Cuts, import / export prices, nonfarm productivity and weekly claims scheduled ahead of tomorrow's payrolls. From the ECB, we will see the minutes from the February meeting ahead of Lagarde comments. Fed's Bowman and Goolsbee are also scheduled.

EGBS: German Curve Bear Flattens, Middle East Headlines Generate Vol

The German curve has bear flattened today, with developments in the Middle East still dominating intraday price action. 2-year yields are up 5.5bps to 2.18%, with oil/gas benchmarks broadly consolidating this week's surges. Meanwhile, 10-year yields are up 4bps to 2.79%. That leaves 2s10s at 60bps, a little above Tuesday’s 59.5bp multi-month low.

- ECB officials continue to push back on the need for an immediate policy reaction to the energy price moves, but stress that it is the length and severity of the conflict that will be key to monitor. EUR 5y5y inflation expectations remain broadly well anchored for now, currently at 2.12%.

- Bund futures are -45 ticks at 127.79 on very heavy cumulative volumes of over 600k. The largest burst of activity came amid a Sky News Arabia post suggesting “Iran is ready to abandon its nuclear program on condition that the United States presents a satisfactory alternative offer”. There remains little clarity on the timing and context of the comments, and Bunds have since pared knee-jerk gains.

- Spain and France have sold bonds today. The 3.50% Nov-35 OAT saw poor results, attracting a 2.19x bid-to-cover ratio for the E6.455bln issued (vs 2.43x prior cover). The lowest accepted price of 100.81 was also below the 100.858 pre-auction mid-price. The secondary price of the OAT has weakened following publication of the results.

- In data, Eurozone January retail sales were weaker than expected at -0.1% M/M (vs 0.3% cons), though December sales were revised up to 0.1% (vs -0.5% initial). French January IP was broadly in line (0.5% M/M vs 0.4% cons), while Spain was weaker than expected (-0.4% M/M vs 0.5% cons).

GILTS: Off Lows, Energy Prices Remain Key

Commodity price swings continue to dominate, with the Iran conflict remaining front and centre.

- An earlier reduction of geopolitical risk premia has faded, with bonds and equities back from recovery highs and crude oil off pullback lows as markets question the timing of comments made by the Iranian Deputy Foreign Minister, noting that “Iran is ready to abandon its nuclear program on condition that the United States presents a satisfactory alternative offer”.

- Elsewhere, ongoing attacks on tankers in the Gulf underscore energy supply issues, presenting inflationary risks.

- Gilt futures -45 at 91.76, in a 91.46-92.15 range.

- Initial support and resistance located at 91.14 and 92.34, respectively, with this week’s sharp reversal lower cancelling a bullish technical backdrop.

- Yields 3.5-5.0bp higher, bear flattening resumes alongside the inflationary risks.

- The GBP3.5bln 4.00 May-29 gilt auction was well-received, with relatively firm pricing vs. secondary levels, albeit with a slightly wider price tail vs. the prior auction (reflective of current vol.).

- Week-to-date yields highs went untested across the curve during the early sell off, although 10s briefly traded through 4.50%.

- BoE-dated OIS showing ~27bp of cuts through year-end vs. ~34bp late yesterday and hawkish extremes of ~16bp earlier in the week.

- Market pricing still looks overly cautious when it comes to the degree of rate cuts showing, particularly given risks to the labour market. We believe the next move lower in Bank Rate could come as soon as April (~13.5bp of easing priced through that event at present).

- There was little in the DMP survey to sway any MPC member's vote.

- Geopolitics and cross-market inputs will continue to dominate today.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.681 | -4.8 |

Apr-26 | 3.594 | -13.5 |

Jun-26 | 3.550 | -17.9 |

Jul-26 | 3.508 | -22.1 |

Sep-26 | 3.491 | -23.8 |

Nov-26 | 3.461 | -26.7 |

Dec-26 | 3.458 | -27.1 |

EQUITIES: E-Mini S&P Continues to Trade Within a Relatively Tight Range

A strong short-term reversal in EuroStoxx 50 futures has resulted in a breach of both the 20- and 50-day EMAs. This highlights potential for a deeper near-term pullback and Tuesday’s sell-off confirmed this threat. Sights are on 5689.00 next, the Dec 18 ‘25 low. On the upside, initial firm resistance is 5964.14, the 50-day EMA ahead of 6023.56, the 20-day EMA. For now, gains would likely be corrective. S&P E-Minis have recovered from their most recent lows. For now, the contract continues to trade inside a range. Attention is on the base of this range at 6751.50, the Feb 6 low. This support has been pierced, a clear break of it would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

- Japan's NIKKEI closed higher by 1032.52 pts or +1.9% at 55278.06 and the TOPIX ended 69 pts higher or +1.9% at 3702.67.

- Elsewhere, in China the SHANGHAI closed higher by 26.092 pts or +0.64% at 4108.567 and the HANG SENG ended 71.86 pts higher or +0.28% at 25321.34.

- Across Europe, Germany's DAX trades higher by 37.89 pts or +0.16% at 24242.32, FTSE 100 higher by 34.96 pts or +0.33% at 10602.63, CAC 40 up 17.5 pts or +0.21% at 8185.23 and Euro Stoxx 50 up 13.11 pts or +0.22% at 5884.03.

- Dow Jones mini down 90 pts or -0.18% at 48705, S&P 500 mini down 3.5 pts or -0.05% at 6871.5, NASDAQ mini down 7.25 pts or -0.03% at 25113.75.

Time: 10:10 GMT (05:10 ET)

COMMODITIES: WTI Futures Bull Cycle Intact, $80 the Next Target

A volatile bull cycle in WTI futures remains intact. Despite being in overbought territory, the contract traded higher Tuesday to confirm a resumption of the current uptrend. The move higher paves the way for a climb towards the $80.00 handle next. The first key support to monitor is $66.75, the 20-day EMA. A pullback would allow the overbought condition to unwind. Gold continues to trade below Monday’s intraday high. For now, a short-term bullish theme remains intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $5083.1, the 20-day EMA.

- WTI Crude up $1.73 or +2.32% at $76.37

- Natural Gas up $0.04 or +1.51% at $2.962

- Gold spot up $10.87 or +0.21% at $5150.53

- Copper down $4.55 or -0.77% at $586.2

- Silver up $0.38 or +0.45% at $83.9415

- Platinum up $5.58 or +0.26% at $2166.29

Time: 10:10 GMT (05:10 ET)

| Date | GMT/Local | Impact | Country | Event |

| 05/03/2026 | - | National People's Congress | ||

| 05/03/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/03/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/03/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 05/03/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 05/03/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/03/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/03/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/03/2026 | 1700/1800 | ECB Lagarde Lecture on Global Risk | ||

| 05/03/2026 | 1815/1315 | Fed's Michelle Bowman | ||

| 06/03/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 06/03/2026 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 06/03/2026 | 1000/1100 | ECB Lagarde Lecture at Politecnico di Milano | ||

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/1430 | ECB Cipollone Presentation at European Banking Federation Meeting | ||

| 06/03/2026 | 1330/0830 | *** | Retail Sales | |

| 06/03/2026 | 1500/1000 | * | Ivey PMI | |

| 06/03/2026 | 1500/1000 | * | Business Inventories | |

| 06/03/2026 | 1515/1015 | San Francisco FEd's Mary Daly | ||

| 06/03/2026 | 1515/1015 | Philadelphia Fed's Anna Paulson | ||

| 06/03/2026 | 1700/1800 | ECB Schnabel Keynote at Booth School of Business Policy Forum | ||

| 06/03/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/03/2026 | 1820/1320 | Boston Fed's Susan Collins | ||

| 06/03/2026 | 1830/1330 | Cleveland Fed's Beth Hammack | ||

| 06/03/2026 | 2000/1500 | * | Consumer Credit |