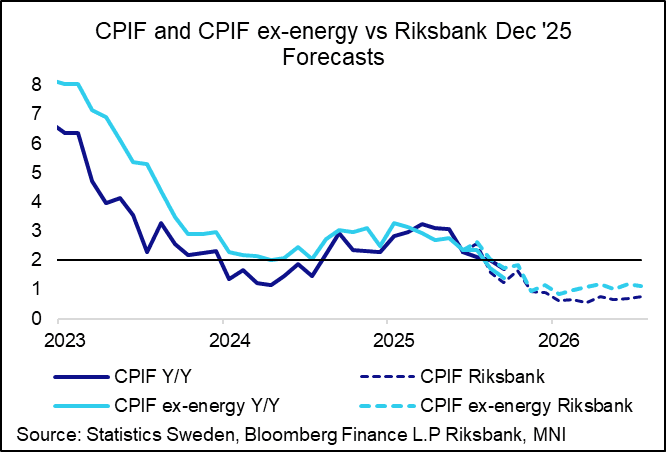

SWEDEN: Food and Goods Drive Downside Surprise, Jansson Likely To Support Cut

Looking at the details of the flash report – newly released as of February – goods and food were the primary downside driver of the soft CPIF ex-energy reading. It seems likely that Riksbank Deputy Governor Jansson will vote for a cut at the March decision, but we are less sure on the other members. We still think some activity weakness is likely needed for Thedeen/Seim to support another cut, for example. The recent developments in energy markets (and the impact it could have on inflation expectations) may provide another argument to hold steady on March 19. That said, the uncertainty shock stemming from the conflict could also be portrayed as a dovish development if the Riksbank becomes concerned about the household consumption outlook. The reaction in SEK FX to the inflation report has been fairly contained for now, with EURSEK still hovering just below 10.70.

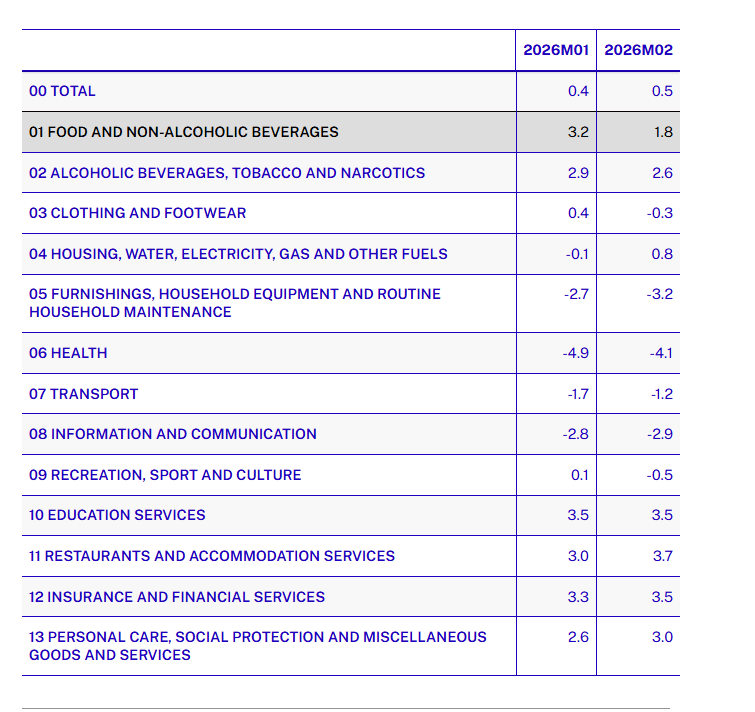

- Services excluding the capital stock ticked up to 2.1% Y/Y (vs 1.9% prior). A reminder that services was the main driver of the soft January reading.

- "Insurance and financial services" was 3.5% Y/Y (vs 3.3% prior), while "restaurants and accommodation" rose to 3.7% Y/Y (vs 3.0% prior).

- Capital stock unchanged at 3.8% Y/Y

- Food, alcohol and tobacco the main downside driver at 2.0% Y/Y (vs 3.1% prior).

- Energy rises to 6.3% Y/Y (vs 5.9% prior).

- Goods excluding food, alcohol and tobacco slips further into deflationary territory to -1.3% Y/Y (vs -0.7% prior).

- "Clothing and footwear" -0.3% Y/Y (vs 0.4% prior).

- "Furnishings and household equipments" -3.2% Y/Y (vs -2.7% prior).

- See table below for full COICOP breakdown (via Stats Sweden)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT TECHS: (H6) Trading Below Former Trendline Support

- RES 4: 92.95 High Jan and a key resistance

- RES 3: 92.51 High Jan 19

- RES 2: 92.13 High Jan 22

- RES 1: 91.39 20-day EMA

- PRICE: 90.99 @ Close Feb 2

- SUP 1: 90.48 Low Jan 29

- SUP 2: 90.00 Round number support

- SUP 3: 89.86 Low Nov 19 2025 and a key support

- SUP 4: 89.52 1.500 proj of the Jan 14 - 20 - 22 price swing

Gilt futures remain in a bear-mode condition. Recent weakness has resulted in a break of the 20-day EMA. Note too that price is trading below 91.29, a trendline support drawn from the Nov 19 low. The breach of the trendline undermines the recent bull theme and highlights potential for a deeper retracement with sights on the 90.00 handle next. Initial resistance is at 91.39, the 20-day EMA.

BTP TECHS: (H6) Support Remains Intact For Now

- RES 4: 121.87 2.000 proj of the Dec 10 - 17 - 22 price swing

- RES 3: 121.58 1.764 proj of the Dec 10 - 17 - 22 price swing

- RES 2: 121.37 High Nov 13

- RES 1: 121.31 High Jan 30

- PRICE: 120.95 @ Close Feb 2

- SUP 1: 120.39 Trendline drawn from the Dec 10 low

- SUP 2: 119.45 Low Dec 22

- SUP 3: 119.13 Low Dec 10 and the bear trigger

- SUP 4: 118.00 Round number support

A bullish theme in BTP futures remains intact and recent weakness has been a correction. This leaves 121.37, the Nov 13 high, exposed. Clearance of it would strengthen the bullish theme. On the downside, a reversal lower would instead pave the way for a move towards 120.39, a short-term trendline support drawn from the Dec 10 low. Clearance of this trendline would undermine the bull theme and signal scope for a deeper retracement.

MNI: TURKEY JAN CPI 4.84% M/M (0.89% DEC)

- MNI: TURKEY JAN CPI 4.84% M/M (0.89% DEC)