NEW ZEALAND: Q4 Building Volume Work Falls, Below Forecasts, Q3 Rise Revised

New Zealand Q4 volume of buildings work fell -3.1%q/q, against a 1.9% forecast rise. The prior Q3 outcome was revised down to a 0.2% rise, originally reported as a 1.5% gain. The level of building work volume is now back to mid 2020 levels, although the rate of decline in y/y terms is moderating. We printed at -4.8%, from -6.7% prior for this series. At the margin, lack of upside momentum in the construction side of the economy should give the RBNZ confidence around core inflation pressures remaining contained. We will get more partials for NZ Q4 GDP next Thursday, when manufacturing activity is due. Note that Q4 GDP prints on March 19.

- Weakness was in both residential construction, down 1.1%, and non-residential construction, which fell by 6.5%/q/q.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Slightly Cheaper After A Heavy Session For US Tsys, ISM Strong

NZGBs are 1bp cheaper after a heavy session for US tsys. US tsys finished 4-5bps cheaper across the curve, reversing early Monday gains after a surge in ISM data.

- The ISM data was far stronger than expected in January as it jumped 4.7pts to 52.6 for its highest since Aug 2022, significantly above even the highest analyst estimate of 51.0. New orders and production both surged to their highest since early 2022 - unlike the final PMI survey released shortly beforehand, it doesn’t look linked to an inventory build.

- NZ’s home-building approvals fell 4.6% m/m in December, following a revised 2.7% gain in November.

- The local calendar will see Q4 Employment data on Wednesday.

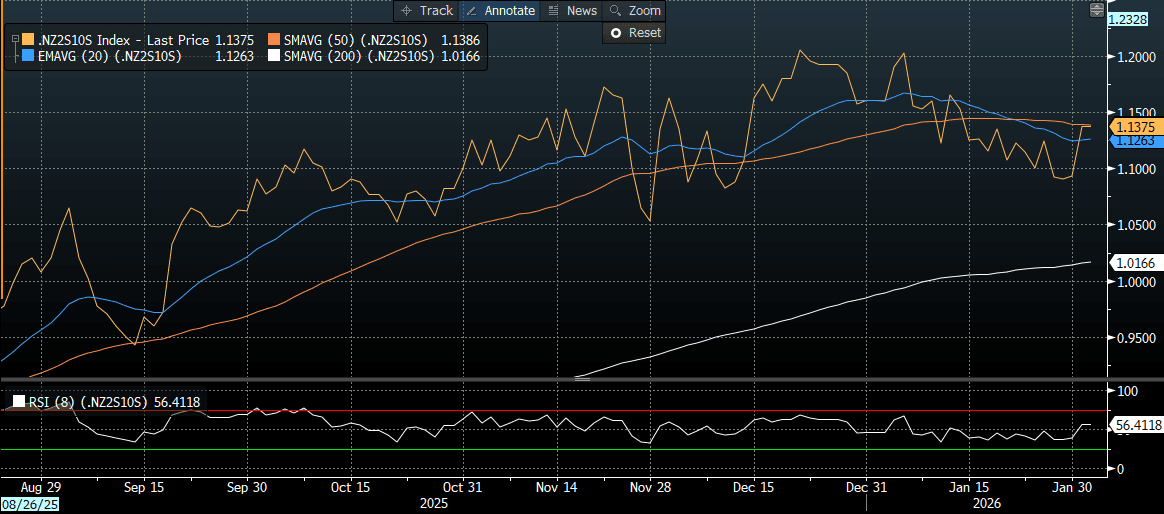

- Swap rates are flat to 2bps higher, with a steeper 2s10s curve. At the current level, it sits within its recent range, its steepest since 2021 (see chart).

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while December 2026 assigns 52bps.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

CNH: Outperforms, CNH v Key Crosses May Be Preferred Amid Higher US Yields

Spot USD/CNH tracks near 6.9410 in early Tuesday dealings, with dips under 6.9400 supported in Monday trade. CNH gained 0.25% for Monday's session though, significantly outperforming the BBDXY's +0.30% rise (while the DXY climbed 0.60%), as broader USD sentiment was mostly supported. Yesterday's lower than expected USD/CNY fix, combined with onshore media reporting China's desire for the yuan as a global reserve currency, were CNH positives and seen as tolerance for further gains. Spot USD/CNY finished up at 6.9453, while the CNY CFETS basket tracker surged 0.62% to 97.57, in line with yuan outperformance.

- Recent lows in USD/CNH at 6.9313 aren't too far away, while near term resistance remains around the 20-day EMA, close to 6.9625 (which acted as a cap through Jan/early Feb). Focus will be on the USD/CNY fixing today after yesterday's negative error term (the first since late Nov last year) aided CNH sentiment.

- We did see a positive US Tsy yield backdrop unfold during US trade on Monday, aided by the stronger than expected ISM print. US-CH yield differentials have drifted higher, the 10yr spread to +246bps, fresh highs since Sep last year.

- This may limit or slow USD/CNH downside, although there remains scope for CNH outperformance on key crosses amidst a more positive USD backdrop. CNH/JPY has bounced from the 22.00 region and is around 22.4160 in early dealings today, just above the 20-day EMA.

- The local data calendar is empty today, with the RatingDog Services PMI out for Jan tomorrow.

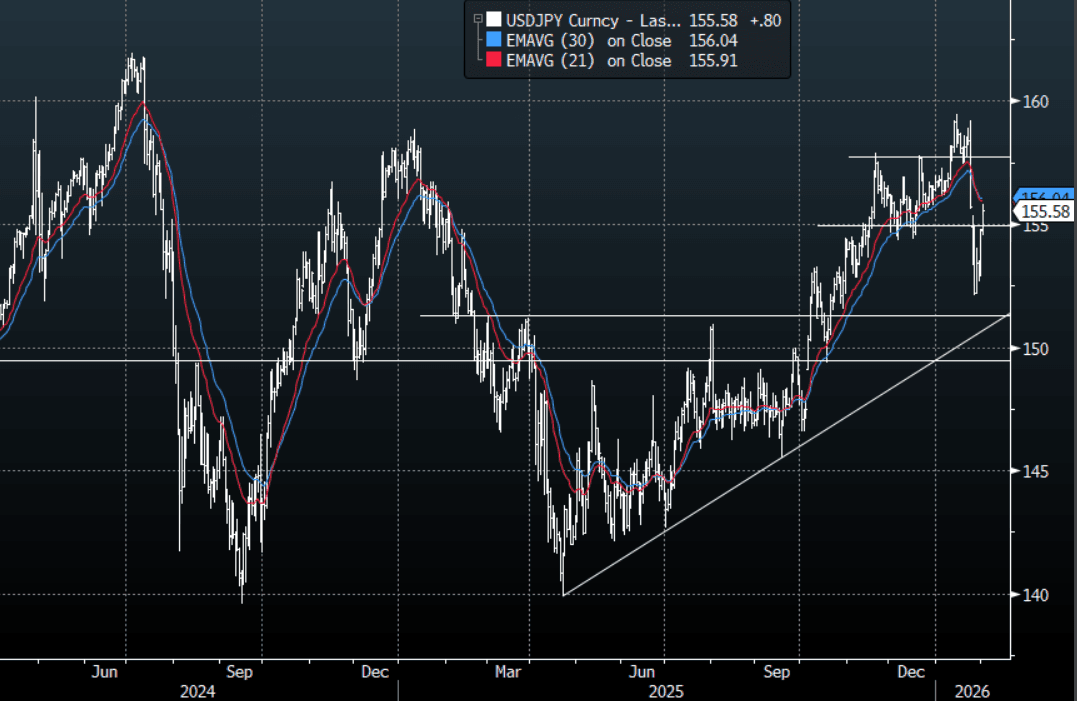

JPY: USD/JPY-Bounce Gives Overextended Yen Shorts The Chance To Pare Back

The USD/JPY overnight range was 154.58 - 155.79, Asia is currently trading around 155.60. USD/JPY has been doing some work between 154.50-156.00 as the USD continues to grind higher. CFTC data up until last Tuesday shows leveraged funds paring back large Yen shorts, this bounce back to 156 could provide decent levels to further reduce positioning for CTA/Momentum type players. In today's session, watch to see if these positions are further reduced into the 156.00 area. The juggernaut speed it was building to the topside looks to have been broken for now and we might need to consolidate and do some work before embarking on a clear trend again. What is clear though is that the price action had more to do with overextended positioning and after some consolidation the pressure against the Yen could be resumed at some point.

- “The US jobs report scheduled for Friday will be delayed.” - BBG

- MNI INTERVIEW: Fed To Keep Cutting On Jobs Weakness - Tilley. A weak labor market and improving inflation will prompt the Federal Reserve to keep cutting interest rates at its next few meetings, former Philadelphia Fed officer and economic adviser Luke Tilley told MNI.

- CFTC Data up to 27/01/2026 shows Asset Managers started to add back to their reduced JPY longs, +28695(Last +19404). The Leveraged community continued to pare back their large shorts after the BOJ, –70552(Last -89657).

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.75($876m), 158.50($442m). Upcoming Close Strikes : 153.00($1.59b Feb 5), 151.50($1.11b Feb 4) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 159 Points

- Data/Event : Monetary Base YoY

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P