MNI US OPEN - Longest Shutdown in US History Set to Conclude

EXECUTIVE SUMMARY

- GOVERNMENT REOPENS AS TRUMP SIGNS BILL TO END NATION’S LONGEST SHUTDOWN

- BRUSSELS AIMS TO ACCELERATE CRACKDOWN ON CHEAP CHINESE PARCELS

- BOJ'S UEDA SEES UNDERLYING CPI TOWARD 2% TARGET

- UK GDP DATA NOISY, NO CLEAR IMPLICATIONS FOR BAILEY'S DECEMBER VOTE

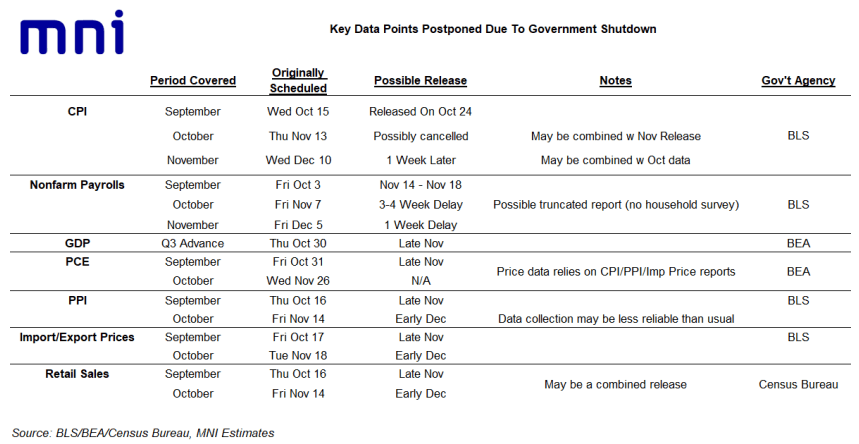

Figure 1: Potential release dates for postponed US data points

NEWS

US (NYT): Government Reopens as Trump Signs Bill to End Nation’s Longest Shutdown

The federal government began reopening Wednesday night after President Trump signed into law a spending package that narrowly passed the House, ending the longest shutdown in the nation’s history. “With my signature, the federal government will now resume normal operations,” Mr. Trump said as he signed the legislation alongside Republican House leadership and business executives. Earlier, the House voted 222 to 209 on Day 43 of the shutdown and days after eight senators in the Democratic caucus broke their own party’s blockade and joined Republicans in allowing the spending measure to move forward, prompting a bitter backlash in their ranks.

US (MNI): U.S. Federal Data Re-Opening 2025: FAQs

With the U.S. federal government shutdown that began Oct 1 set to end later this week, dozens of postponed government agency data reports are due to be rescheduled for release over the coming weeks and months. Some may be cancelled altogether. We go through the prospects for major data releases over the coming weeks in the attached PDF. MNI’s rough estimates are in the table included in the link – we will publish updates to the official calendar as and when they are announced in the coming days.

EU/CHINA (FT): Brussels Aims to Accelerate Crackdown on Cheap Chinese Parcels

Brussels has called for an EU-wide handling fee on small packages ordered online from platforms such as Shein, Temu and Alibaba to be imposed in early 2026, more than two years earlier than scheduled, in a bid to crack down on billions of cheap Chinese imports each year. The European Commission urged EU finance ministers meeting on Thursday to agree on the faster implementation to protect domestic retailers from unfair competition.

FRANCE (BBG): France’s Victory Over Inflation Looks Lasting, Villeroy Says

France’s success in bringing inflation down from a high of more than 7% looks sustainable, while the economy is also weathering political upheaval well, according to central-bank chief Francois Villeroy de Galhau. “If I had to sum up the view about the French economy, I would say two good news and they are that first, the victory against inflation — and I think it’s lasting,” Villeroy told an event Thursday in Paris. “Second, good French news which is the resilience of our growth.”

NORWAY (MNI): Cost-Driven Upward Revision to 2026 Oil and Gas Investment Expectations

Cost-Driven Upward Revision to 2026 Oil and Gas Investment ExpectationsNorwegian oil and gas investment is expected to be NOK249bln in 2026, according to Statistics Norway's Q4 oil and gas investment survey. That's an upward revision of 8.4% (NOK19bln) relative to last quarter, and suggests the Y/Y decrease in nominal investment next year will be smaller than previously assumed. However, Statistics Norway notes that most of the upward revision is due to higher costs on some field development projects. This suggests the Y/Y change in real investments is still likely to be negative, and drag on 2026 headline GDP growth.

SCOTLAND (BBG): Scotland Plans First National Bond After Getting Credit Ratings

Scotland plans to issue its first bond within about the next two years as the devolved government seeks to raise funds and develop relationships with financial institutions. “The issuance will be the first in a £1.5 billion bond program over the life of the next parliament, subject to the outcome of the Scottish Parliament election, in-year borrowing requirements and market conditions,” First Minister John Swinney said on Thursday.

BOJ (MNI): BOJ's Ueda Sees Underlying CPI Toward 2% Target

Bank of Japan Governor Kazuo Ueda said Thursday that underlying CPI inflation, excluding temporary factors, is gradually moving toward the bank’s 2% target, and that the mechanism in which wages and prices rise moderately in tandem will be maintained. Speaking to lawmakers, Ueda said prices – particularly for rice – remain influenced by cost-push factors, but noted that food prices overall are gradually increasing as companies pass on higher labour costs to consumers. Ueda made no reference to the outlook for monetary policy.

GLOBAL (BBG): Xi Joins Trump in Skipping G-20 Summit in Blow to South Africa

Chinese President Xi Jinping will not join the Group of 20 summit later this month, a move that will be a blow to host South Africa that’s already facing a boycott from US President Donald Trump. China’s Ministry of Foreign Affairs announced Thursday that Premier Li Qiang would represent the Asian nation at the leaders’ summit, which kicks off in Johannesburg on Nov. 22. The statement didn’t explain why Xi, who attended the event last year, will be absent this time.

OIL (BBG): IEA Boosts Forecast of Record Global Oil Glut for a Sixth Month

The International Energy Agency increased its estimates for a record global oil surplus next year for a sixth consecutive month, as OPEC+ continues to revive supplies and demand growth remains subdued. World oil supplies will exceed demand in 2026 by just over 4 million barrels a day, the IEA said a monthly report on Thursday, a slight increase from last month. The agency has made upward revisions every month since June. Any impact from recent trade tariff turmoil or new US sanctions on Russian producers remains unclear, it added.

MNI BCRP PREVIEW - NOVEMBER 2025: Hold Seen, Risk of Dovish Tilt

With the policy rate already very close to neutral and growth around its potential rate, the BCRP is widely expected to remain on hold at 4.25% this week. Previously, Governor Velarde has also said that there is no need to be aggressive with rate cuts. However, recent softer-than-expected CPI inflation data and mounting concerns about the impact of the continued appreciation of the Peruvian sol on the domestic economy keep the door open to a further cut in the coming meetings.

DATA

UK DATA (MNI): GDP Data Noisy, No Clear Implications for Bailey's December Vote

- UK Q3 PRELIM GDP 0.1% Q/Q, 1.3% Y/Y

- UK SEP GDP -0.1% M/M, +0.1% 3M/3M, +1.3% 3M Y/Y

- UK SEP SERVICES INDEX +0.2% M/M, +0.2% 3M/3M

- UK SEP IND PROD -2.0% M/M, -2.5% Y/Y

- UK SEP TRADE BALANCE GBP -1.09BN

It looks as though the majority of the weakness in GDP is driven by the Jaguar Land Rover shutdown in September (production was halted for the entire month). This was of course anticipated to some extent by sellside expectations but it looks as though the knock on effects to the rest of the supply chain were also larger than expected. Note that analysts had pointed to downside risks to this print from JLR. There was a 0.06ppt negative contribution with about 0.04ppt alone due to "manufacturing of transport

equipment". So without this quarterly GDP would have been roughly 0.14% rather than 0.10%. This is obviously still a small downside miss relative to the 0.2% consensus expectation, and as noted above some of this downside was already baked into consensus expectations. This is also the softest quarterly services contribution since Q3-24.

FRANCE DATA (MNI): Unemployment Rises Slightly Again, Broader Labour Market Loosening

France unemployment rose slightly again in Q3. The ILO mainland unemployment rate came in at 7.5%, up from 7.4% in Q2. This quarter's reading is 0.3ppt higher than Q3 2024. The mainland unemployment rate has been trending around 7.25% since 2021, with 2025 so far showing a very mild upward trend (increasing 0.2ppt since Q1). Last week, we noted French private sector wage growth slowing slightly (still positive in real terms) and showing signs of stability, broadly consistent with the latest unemployment data.

CHINA DATA (MNI): China Oct New Loans, Aggregate Finance Slow

- CHINA JAN-OCT NEW LOANS CNY14.97 TRLN VS MEDIAN CNY15.25 TRLN

- CHINA JAN-OCT TSF CNY30.9 TRLN VS MEDIAN CNY31.92 TRLN

- CHINA END-OCT M2 +8.2% Y/Y VS MEDIAN +8.1%; END-SEP +8.4% Y/Y

China's new yuan loans rose by CNY220 billion in October, declining from September's CNY1.29 trillion and marking the lowest growth in recent three months as credit demand weakened amid the government's "anti-involution" campaign and the continous property downturn, data released on Thursday by the People's Bank of China showed. Total social financing rose by CNY810 billion, falling from CNY3.53 trillion in September and hitting the lowest level since July 2024.

JAPAN DATA (MNI): Japan Oct CGPI Rises 2.7% Y/Y; Import Price Drops

Japan’s corporate goods price index (CGPI) rose 2.7% y/y in October, down slightly from September’s revised 2.8%, while import prices posted a ninth consecutive decline, Bank of Japan data showed Thursday. The index was supported by higher prices for nonferrous metals (+11.8% vs +9.6%) but dragged lower by electric power, gas, and water (-0.5% vs +0.6%). On a monthly basis, the CGPI rose 0.4% in October, extending gains after a revised 0.5% increase in September.

AUSTRALIA DATA (MNI): Aussie Labour Market Tightens Over October

Australia’s unemployment rate fell 20 basis points to 4.3% in October, 10bp better than expected, as the economy added 42,000 jobs – double forecasts – the Australian Bureau of Statistics reported Thursday. Full-time employment rose by 55,000, including 29,000 women and 26,000 men, while part-time employment declined by 13,000. The drop in part-time roles was driven by women, whose part-time employment fell by 21,000, partly offset by an 8,000 increase among men.

AUSTRALIA DATA (MNI): Q4 Inflation Expectations Above Q3

Melbourne Institute consumer inflation expectations for November moderated 0.3pp to 4.5% despite news that Q3 inflation increased more than expected and an increase in petrol prices at the end of October/start of November. Even though November moderated the Q4 average inflation expectations are higher than Q3 at 4.65% compared to Q2's 4.4%. Households may have been reassured by RBA Governor Bullock's message that inflation is expected to moderate towards the band's 2.5% mid-point. Inflation expectations peaked this year at 5.0% in June and have been unable to hold breaks below 4%.

FOREX: USD Fade Leads EURUSD Pierce Above 50-Day EMA

- The fade in the USD sees the USD Index dip below 99.20 for the first time since October 30. Price action keeps the short-term series of lower lows and lower highs in the dollar index intact. This put upward pressure on EURUSD, with the pair briefly piercing the 1.1622 50-day EMA (which also marks the 76.4% retracement for the Oct 28 - Nov 05 downleg). Key resistance remains into the 1.1669 Oct 28 high.

- USDJPY remains capped into the 155.0 handle, having tested the mark on three occasions over the past two days, potentially building a short-term resistance zone around that area. BoJ's Ueda appeared content overnight, saying underlying CPI is gradually moving toward the bank’s 2% target, and that the mechanism in which wages and prices rise moderately in tandem will be maintained.

- A resumption of the uptrend in USDJPY after dollar-driven weakness this morning would put sights on 155.53, a Fibonacci projection. Initial support to watch lies at 153.03, the 20-day EMA.

- AUD outperforms (+0.5%) following stronger-than-expected overnight labour market data, with jobs growth doubling consensus. The recent trend, if sustained, is likely to keep RBA rates on hold in the short-term given the Q3 increase in price pressures and uncertainty over policy restrictiveness. Today's price action in AUDUSD undermines the recent bearish theme and instead signals scope for a stronger short-term recovery. The move higher has exposed resistance at 0.6618, the Oct 29 high.

- With the reopening of the US government imminent, markets await any advisories or updates on release schedules for now much-delayed data. ECB's Elderson, BoE's Greene and SNB's Tschudin are scheduled to appear next to a set of speakers from the Fed.

GILTS: Little Impact From Soft GDP

GILTS: Gilts are little changed across the curve, with no lasting impact from the soft (but noisy) UK GDP data.

- The space drew limited support from a downtick in equities and has faded from session highs.

- Gilt futures +8 at 93.73, with bulls unable to close yesterday’s opening gap lower as of yet.

- Still, bulls remain in technical control, initial support and resistance located at 93.14 & 93.98, respectively.

- Yields within 0.5bp of yesterday’s closing levels.

- SONIA futures flat, market still pricing just over 80% odds of a cut through for the December MPC decision. SONIA-implied terminal rate pricing at ~3.30%.

- BoE MPC hawk Greene will speak on central bank independence today (12:00 London). The topic of the panel that she will speak on and the fact that she has already reaffirmed her hawkish views earlier in the week mean that we are unlikely to get a meaningful market reaction.

- A reminder that we currently expect all 4 dovish dissenters on the MPC to vote for a cut in December. At this stage, we expect Governor Bailey to join them (assuming we get in line CPI readings in the interim and this week’s soft labour market data isn’t revised away).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.764 | -20.5 |

Dec-25 | 3.655 | -31.5 |

Feb-26 | 3.559 | -41.0 |

Mar-26 | 3.448 | -52.1 |

Apr-26 | 3.400 | -57.0 |

Jun-26 | 3.348 | -62.1 |

Jul-26 | 3.330 | -63.9 |

Sep-26 | 3.303 | -66.6 |

EGBS: Passing Of Italian Supply Helps BTP Futures Back To Session Highs

- Smooth passing of today’s heavy Italian supply looks to be helping BTPs make a fresh push towards the bull trigger at 121.94 (Oct 17, 22 high). Futures are now +13 ticks at 121.68, lightly outperforming Bunds (RXZ5 +3 ticks at 129.34).

- OAT futures are also at session highs, now +18 ticks at 123.20. Cautious budget optimism appears to have factored into recent OAT outperformance versus Bunds, but we caution that negotiations on the Revenue section of the 2026 budget have only just restarted today.

- Curves trade a little flatter on the session, while 10-year EGB spreads to Bunds are up to 1.5bps narrower. The OAT/Bund and BTP/Bund spreads are each at ~71.5bps. The 70bp figure in both spreads are important supports to monitor.

- In data, Eurozone September industrial production was weaker-than-expected at 0.2% M/M (vs 0.7% cons, -1.1% prior). Meanwhile, the French mainland ILO unemployment rate was higher-than-expected at 7.5% (vs 7.3% cons, 7.4% prior).

- Developments in the US following the Government re-opening will be in focus this afternoon, particularly on the timings of shutdown-impacted data releases.

EQUITIES: Medium-Term Bull Trend in Eurostoxx 50 Futures Remains Intact

A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. The contract has traded through resistance at 5742.00, the Oct 29 high to confirm a resumption of the uptrend. Attention is on 5818.00 next, a Fibonacci projection. Clearance of this hurdle would open 5848.00, a bull channel top drawn from the Aug 1 low. On the downside, initial firm support is seen at 5669.13, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the bear leg since the Oct 30 high appears to have been a correction. The contract has managed to find support below the 50-day EMA, currently at 6728.13, and a key level. Activity on Nov 7 highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. Sights are on 6953.75, Oct 30 high and bull trigger.

- Japan's NIKKEI closed higher by 218.52 pts or +0.43% at 51281.83 and the TOPIX ended 22.39 pts higher or +0.67% at 3381.72.

- Elsewhere, in China the SHANGHAI closed higher by 29.361 pts or +0.73% at 4029.501 and the HANG SENG ended 150.3 pts higher or +0.56% at 27073.03.

- Across Europe, Germany's DAX trades lower by 67.52 pts or -0.28% at 24312.88, FTSE 100 lower by 28.57 pts or -0.29% at 9883.03, CAC 40 up 41.56 pts or +0.5% at 8282.8 and Euro Stoxx 50 up 10.39 pts or +0.18% at 5797.7.

- Dow Jones mini up 9 pts or +0.02% at 48376, S&P 500 mini down 9.25 pts or -0.13% at 6865.75, NASDAQ mini down 49.75 pts or -0.19% at 25571.25.

Time: 10:00 GMT

COMMODITIES: Yesterday's Sell-Off Strengthens a Bearish Theme for WTI

A sell-off in WTI futures yesterday, strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. A breach of this hurdle would signal scope for a stronger correction. The downleg in Gold since Oct 20 appears to have been a correction and the move down has allowed an overbought condition to unwind. Recent gains suggest that correction is over. A key support at the 50-day EMA, at $3910.9, is intact. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is $4264.7, a Fibonacci retracement. A stronger recovery would open $4381.5, the Oct 20 high and bull trigger.

- WTI Crude down $0.28 or -0.48% at $58.21

- Natural Gas down $0.04 or -0.97% at $4.486

- Gold spot up $37.59 or +0.9% at $4233

- Copper up $2.1 or +0.41% at $512.5

- Silver up $0.88 or +1.66% at $54.1323

- Platinum up $9.73 or +0.6% at $1627.97

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 13/11/2025 | 1200/1200 | BOE Greene in Panel on Central Bank Independence | ||

| 13/11/2025 | - | *** | Money Supply | |

| 13/11/2025 | - | *** | New Loans | |

| 13/11/2025 | - | *** | Social Financing | |

| 13/11/2025 | - | ECB de Guindos at ECOFIN Meeting in Brussels | ||

| 13/11/2025 | 1300/1400 | ECB Elderson Moderates Climate and Banks Panel | ||

| 13/11/2025 | 1300/0800 | San Francisco Fed's Mary Daly | ||

| 13/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 13/11/2025 | 1530/1030 | Minneapolis Fed's Neel Kashkari | ||

| 13/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/11/2025 | 1700/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 13/11/2025 | 1700/1200 | ** | US DOE Petroleum Supply | |

| 13/11/2025 | 1715/1215 | St. Louis Fed's Alberto Musalem | ||

| 13/11/2025 | 1720/1220 | Cleveland Fed's Beth Hammack | ||

| 13/11/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/11/2025 | 1900/1400 | ** | Treasury Budget | |

| 14/11/2025 | 0001/0001 | KPMG/REC Report on Jobs | ||

| 14/11/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 14/11/2025 | 0200/1000 | *** | Retail Sales | |

| 14/11/2025 | 0200/1000 | *** | Industrial Output | |

| 14/11/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 14/11/2025 | 0700/0800 | ** | Unemployment | |

| 14/11/2025 | 0745/0845 | *** | HICP (f) | |

| 14/11/2025 | 0800/0900 | *** | HICP (f) | |

| 14/11/2025 | 0900/1000 | Foreign Trade | ||

| 14/11/2025 | 1000/1100 | * | Trade Balance | |

| 14/11/2025 | 1000/1100 | *** | EZ GDP 2nd (f) | |

| 14/11/2025 | 1030/1130 | ECB Elderson Keynote at ECB Banking Supervision Forum | ||

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic |