MNI US OPEN - House Republicans Move to Put Off Tariff Vote

EXECUTIVE SUMMARY

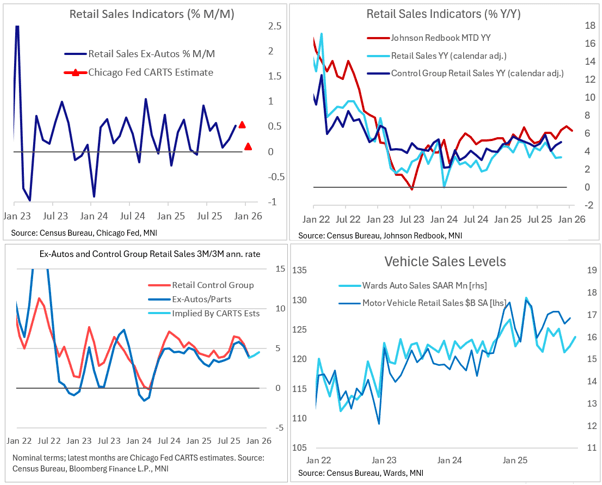

- RETAIL SALES SEEN CONFIRMING SOLID IF SLIGHTLY SLOWER Q4 PCE

- HOUSE REPUBLICANS MOVE TO KEEP PUTTING OFF VOTE ON TRUMP TARIFFS

- RUSSIA AIMS ONLY TO ‘BUY TIME’ IN PEACE TALKS, SPY REPORT SAYS

- KEIR STARMER LIVES TO FIGHT ANOTHER DAY AFTER CABINET RALLY

Figure 1: US retail sales indicators

NEWS

MNI US PAYROLLS PREVIEW: Watch the Forest, Not Just the Trees

Wednesday sees an unusual BLS nonfarm payrolls report after a brief delay following last week’s government shutdown, with January details released at 0830ET. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take. Consensus looks for a circa 70k increase in nonfarm payrolls coming almost entirely from private payrolls. The unemployment rate is expected to hold at 4.4% after last month’s surprise drop to 4.38% from 4.54%, leaving a profile of broad stabilization on net since Aug/Sept. In doing so it ruled out a more dovish base case that seven FOMC members had pencilled in at the December SEP.

MNI US DATA PREVIEW: Retail Sales Seen Confirming Solid if Slightly Slower Q4 PCE

The Census Bureau's delayed December advance retail sales report (Tuesday 0830ET release) is expected to see a deceleration in sequential headline growth with core remaining solid at end-year. Current Bloomberg consensus is for 0.4% M/M overall sales growth (0.6% prior), but ex-auto/gas at 0.4% (same as Dec) and the GDP-input Control Group rising 0.4% (again, same as prior). November retail sales data were largely in line with consensus and solid on all counts, though October's very strong report was revised down to slightly less robust (but still quite strong) levels. It kept Q4 private consumption estimates elevated with little indication of a meaningful retail consumption slowdown toward the end of the year.

US (BBG): House Republicans Move to Keep Putting Off Vote on Trump Tariffs

House Republicans on Monday advanced a procedural motion to block a vote on President Donald Trump’s tariff agenda, potentially delaying a politically uncomfortable vote on his most prominent economic policy until at least July. The motion will be voted on by the chamber this week. Republicans have a razor-thin majority, so even a few defections could wreck the chances of extending the block, which started last March as the president began a trade clash with Canada.

US (WSJ): Wall Street’s Hunt for Cheaper Stocks Goes Global

Last spring, it was “Sell America.” Now Wall Street’s hot trade is buy everywhere else. After years making outsize bets on the largest U.S. companies, investors are moving more money into international markets, wagering that America’s wide lead on the rest of the world will shrink. For years, money managers say, the U.S. stock market was viewed as the only game in town. Now that perception is starting to shift.

US/CANADA (WSJ): Trump Threatens to Block Opening of New Bridge Between Detroit and Canada

President Trump threatened on Monday to not allow the opening of a new bridge connecting Canada with Detroit, marking the latest source of political tension between the two countries. The Gordie Howe International Bridge is close to completion after nearly eight years of construction paid for by Canada. The cable-stayed bridge, running 1.5 miles, marks a new piece of trade infrastructure to alleviate congestion at the Detroit-Windsor, Ontario, gateway, the busiest commercial land crossing in North America.

RUSSIA/UKRAINE (BBG): Russia Aims Only to ‘Buy Time’ in Peace Talks, Spy Report Says

Russia is exploiting negotiations to end the war in Ukraine as a “tool for manipulation” as it aims to restore relations with the US, but has no intention of ending the invasion, according to an assessment by Estonian foreign intelligence. “Russia is setting long-term operational objectives in its war against Ukraine. This confirms that the recent uptick in peace-talk rhetoric is merely a tactic to buy time,” according to the annual report of the Estonian Foreign Intelligence Service published on Tuesday.

US/EUROPE (BBG): Macron Says Europe Needs to Stand Up to Trump on Trade and Tech

French President Emmanuel Macron said the European Union needs to get tougher with US President Donald Trump, who is pushing for the “dismemberment” of the bloc. Macron, speaking in an interview with newspapers including Le Monde and the Financial Times, said he expects a clash with the US president this year over the EU’s regulation of digital services, which could result in Washington imposing new tariffs on the EU. “The US will, in the coming months — that’s certain — attack us over digital regulation,” he said. Macron added that Spain and France may be targeted over their proposed social media bans for children.

UK (The Times): Keir Starmer Lives to Fight Another Day After Cabinet Rally

Sir Keir Starmer has insisted he will not “walk away” after surviving an attempt to force him from office as his allies were accused of trying to smear his leadership rival Wes Streeting. Anas Sarwar, the Scottish Labour leader, became the first leading party figure to call for Starmer to go as he warned that “failures at the heart of Downing Street” would cost the party the chance of returning to power in Scotland. He said that the “leadership in Downing Street has to change” and that while Starmer and his team had “promised they were going to be different, too much has happened” for him to stay in power.

UK (FT): Rising Share of UK Public in Favour of Tax and Spending Cuts

The latest British Social Attitudes report, published on Tuesday by the National Centre for Social Research, showed that 19 per cent of people said taxes and spending should be reduced, the highest since comparable data was first available in 1983, and more than three times the all-time average of 6 per cent.

CHINA (MNI EXCLUSIVE): China’s Property Market to Continue Decline Over 2026

Advisors and analysts share their outlook for China's property market. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CORPORATE (BBG): TSMC Revenue Jumps 37% in January as AI Spending Marches On

Taiwan Semiconductor Manufacturing Co.’s January sales grew at their fastest clip in months, a sign of sustained global AI spending even as concerns persist about an industry bubble. The contract chipmaker for Nvidia Corp. reported a 37% rise in January revenue to NT$401.3 billion ($12.7 billion), above the 30% revenue growth TSMC expects for the full year. The year-ago comparison, however, may have been affected by the Lunar New Year holidays, which in 2025 fell in January.

DATA

UK DATA (MNI): BRC Retail Sales See Strong Start to 2026, Especially Non-food Sales

- UK JAN BRC TOTAL RETAIL SALES 2.7% Y/Y

BRC retail sales jumped to 2.7% Y/Y in January (1.2% Dec), the strongest since last August, and ending a run of four consecutive slowdowns in the Y/Y rate. Retail sales saw broad-based growth, with both food and non-food sales growing notably. Although we have consistently noted high food inflation driving the headline rate here, the picture for January is more mixed with both food and non-food (where inflation is not as high) sales jumping significantly compared to last year. Food sales accelerated further to 3.8% Y/Y (3.1% Dec), now at the highest rate since last August.

FRANCE DATA (MNI): Unemployment Rate Rises 0.2ppt, Sharp Rise in Youth Unemployment

French mainland unemployment ticked up 0.2ppt to 7.7% in Q4, against consensus of a stable 7.5% print - this marks the highest level since Q3 2021. INSEE notes a sharp rise in youth unemployment which helped the move higher, though both the overall and youth activity rates also increased. The mainland unemployment rate had been within a 6.9-7.3% range between Q4-21 and Q1-25, but over the past year the rate has seen four consecutive quarterly rises to stand 0.4ppt above this range. The all-France (excl. Mayotte) unemployment rate (which has been almost perfectly correlated with the mainland rate) came in at 7.9%, also up 0.2ppt from Q3, and also 0.4ppt above the Q4-21 to Q1-25 range.

GERMANY DATA (MNI): Overall Capacity Utilization is Slowly Rising - IFO

The utilization of available production capacities (complete economy) in Germany rose to 83.6 percent in January 2026 according to IFO data. "This continues a positive trend that likely began in mid-2025 [...] the German economy has apparently left its low point behind and is beginning to recover", they conclude. Putting this into context, the institute's statement on the data seems quite broad and based on a longer-term view than the monthly business climate index, which can be prone to volatility at times.

NORWAY DATA (MNI): January CPI-ATE Sees Broad-Based Strength, Rents and Insurance Noted

- NORWAY JAN CPI +0.6% M/M, +3.6% Y/Y

- NORWAY JAN CPI-ATE +0.3% M/M, +3.4% Y/Y

The January acceleration in Norwegian CPI-ATE inflation looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. There may be scope for some payback in February owing to a significant acceleration in airfares, but that won't be enough to ease Norges Bank concerns around inflation persistence. On a seasonally adjusted basis using Statistics Norway data, CPI-ATE rose 0.49% M/M in January, the highest sequential reading since February 2025. That pulled 3m/3m inflation momentum up to 3.22% (vs 3.09% prior), a 9-month high.

SWEDEN DATA (MNI): Consumption Eases in December But Quarterly Growth Still Positive

This morning's Swedish activity data provides some context to the weaker-than-expected Q4 flash GDP reading (0.2% Q/Q vs 0.4% Riksbank, 0.5% consensus). It doesn't call into question the Riksbank's expectations for growth to continue to strengthen through this year. Focus remains on the final Q4 GDP report on February 27, given the flash release is often sensitive to revisions. After growing solidly in October and November, household consumption pulled back 3.7% M/M in December. That left 3m/3m growth at 0.5% (vs 1.6% in Nov, 1.3% in Oct, 1.1% in Sep).

AUSTRALIA DATA (MNI): Business Conditions Ease, Trend Steady, Labour Costs Lower

The Australia Jan NAB business survey saw conditions moderate to +7 from +9 in Dec last year. Business Confidence was at +3 for Jan, slightly up from a revised +2 reading for Dec last year. The conditions index, which has a reasonably relationship with GDP y/y (see the chart below, the NAB conditions index is the the white line), has largely gone sideways since the middle of last year. It is still suggesting better y/y growth momentum, but to be confident in expecting growth beyond +3%y/y.

AUSTRALIA DATA (MNI): Consumer Sentiment Falls, Household Spending May Soften Further

The Feb Westpac Consumer Sentiment Index print fell 2.6% to 90.5 (from 92.9). This puts the index back close to lows from 2025, and comfortably off Nov highs of 103.8. The index spent a lot of late 2022 to late 2024 in a rough 80-85 region, so we remain above these levels. Westpac notes in terms of today's result: "Muted response compared to previous rate hikes. Current conditions and medium term outlook weaken; year-ahead views stable. Over 80% expect interest rates to rise further in the next 12 months."

FOREX: Japanese Yen Extends Post-Election Recovery

- The Japanese yen has strengthened after Finance Minister Katayama calmed markets on the timing and financing of the sales tax cut for food. Downside momentum for USDJPY has picked up pace, extending the reversal from yesterday’s post-election high to around 1.6%, and printing a pullback low of 155.09.

- Price action increasingly blurs the technical picture for USDJPY as spot is cleanly below through the 50-day EMA which may bolster the short-term bearish outlook. The 100-day MA intersects at 154.52.

- The January acceleration in Norwegian CPI-ATE looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. Any scope for payback in February won't be enough to ease Norges Bank concerns around inflation persistence, which leads EURNOK 0.35% lower with initial support at the Jan 29 low of 11.3610.

- Last week’s stabilisation and then subsequent recovery for risk have spurred an impressive 2.9% AUDUSD rebound from Friday’s low. This culminated in AUDUSD printing a fresh cycle high late Thursday, at 0.7099, the highest level since February 2023. While the 0.71 handle has capped the price action overnight, the session range has remained narrow, allowing the pair to consolidate the solid bounce.

- GBP consolidates its recovery seen yesterday afternoon following PM Starmer securing the public support of every cabinet minister after his future came under threat for his involvement with former ambassador Mandelson. Any market caution around Starmer's future has two legs as the fiscal angle adds to political instability. 1.37 has been capping short-term gains for GBPUSD.

- Separately, downside momentum for EURCHF has extended on Tuesday, resulting in fresh lows at 0.9120 today, the lowest level since the removal of the peg in 2015.

- US retail sales, ECI, import and export prices, redbook retail sales, and business inventories are on the calendar ahead of US payrolls (Wed) and CPI (Fri).

EGBS: Supply Limiting Downside in EGB Yields Today

Downside in German yields has been contained by sovereign and corporate supply, with the latest mandates from Slovakia (20Y) and France (30Y) reinforcing that theme. Intraday, the curve still leans bull flatter, with EGBs taking cues from global peers as opposed to any regional driver.

- 5s30s is down 0.5bps to 111.5bps, though we assess that medium-term steepening pressures remain intact.

- Bund futures are +4 ticks at 128.35, having traded in a tight 16 tick range so far today.

- 10-year EGB spreads to Bunds are marginally narrower on the session, with the 10-year OAT/Bund spread off lows following the syndication mandate.

- The EU is holding a dual tranche syndication today, with conventional supply coming from the Netherlands, Austria and Germany.

- In data, the French mainland unemployment ticked up 0.2ppt to 7.7% in Q4, against consensus of a stable 7.5% print - this marks the highest level since Q3 2021.

- ECB’s de Guindos re-iterated the Governing Council’s “good place” stance. His comments carry less weight given his term ends in a few months.

- The remainder of today’s calendar includes US retail sales.

GILTS: Bull Flattening, Albeit With Bears Remaining in Technical Control

Gilts have firmed, initially benefitting from the bid in wider core global FI markets (with focus on U.S. NEC Chair Hassett’s warning re: the upcoming labour market report and a bid in JGBs amid ongoing digestion of the fiscal situation in post-election Japan).

- Swelling global issuance has capped the rally to some degree.

- Gilts & swap spreads have recovered after Monday’s ministerial support for PM Starmer (albeit with questions over how long such support will ultimately last), trimming UK political & fiscal risk premia established in recent sessions. 10-Year swap spreads are less than 1bp off year-to-date highs.

- Gilt futures +32 at 90.83 vs. highs of 90.96, closing Monday’s opening gap lower.

- The contract has broken through downtrend resistance drawn off the January 15 high. Still, the 20-day EMA (91.09 today) remains unchallenged and presents initial resistance. That leaves bears in technical control, with yesterday’s cycle low (89.76) providing initial support.

- Yields 0.5-3.0bp lower, curve flatter. 2s10s sub-90bp after the first close above since ’18. Next upside level of note at the ’18 closing high (94.63bp).

- Gilt/Bunds traded as wide as ~175bp during yesterday’s gilt sell off but has narrowed to ~166bp at typing.

- The DMO’s GBP3.75bln sale of the 4.125% Mar-31 gilt generated decent demand.

- There is focus on U.S. tech giant Alphabet’s debut GBP deal (across 3-, long 6-, long 15-, 32- & 100-Year maturities). Watch for activity around pricing.

- Front end pricing steady on the day, showing 17bp of easing for March, 23bp for April, 32bp through June and 45bp through November.

- Little of note on the UK economic calendar today.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.557 | -17.1 |

Apr-26 | 3.498 | -23.0 |

Jun-26 | 3.409 | -31.9 |

Jul-26 | 3.346 | -38.2 |

Sep-26 | 3.311 | -41.7 |

Nov-26 | 3.275 | -45.3 |

Dec-26 | 3.285 | -44.2 |

EQUITIES: E-Mini S&P Trading Just Below the Late-January Highs

The medium-term trend condition in EuroStoxx 50 futures remains bullish and the latest pullback through the 50-day EMA appears corrective. A clear break below this average would undermine the bull theme and signal scope for a deeper retracement. The bull trigger is at 6086.00, the Jan 3 high. A move through this hurdle would resume the primary uptrend. A short-term bearish theme in S&P E-Minis resulted in a break last week of 6814.50, the Jan 21 low and a bear trigger. This proved short-lived, however, with prices rising swiftly back above to begin this week. Note this puts the contract back above the 20- and 50-day EMAs. Any continuation lower would open 6691.56, a Fibonacci retracement point. The contract has recovered today. Initial firm resistance now is 7025.43, the 1.0% 10-dma envelope. A break of this hurdle would be bullish.

- Japan's NIKKEI closed higher by 1286.6 pts or +2.28% at 57650.54 and the TOPIX ended 71.71 pts higher or +1.9% at 3855.28.

- Elsewhere, in China the SHANGHAI closed higher by 5.285 pts or +0.13% at 4128.373 and the HANG SENG ended 155.99 pts higher or +0.58% at 27183.15.

- Across Europe, Germany's DAX trades higher by 36.91 pts or +0.15% at 25050.61, FTSE 100 lower by 30.41 pts or -0.29% at 10355.56, CAC 40 up 46.43 pts or +0.56% at 8368.9 and Euro Stoxx 50 up 12.06 pts or +0.2% at 6070.71.

- Dow Jones mini up 34 pts or +0.07% at 50254, S&P 500 mini up 2.5 pts or +0.04% at 6986.25, NASDAQ mini down 5.5 pts or -0.02% at 25352.25.

Time: 10:30 GMT (05:30 ET)

COMMODITIES: WTI Futures Bull Cycle Intact, Remains Above 20-, 50-Day EMAs

A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.16. The 50-day EMA lies at $60.50. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude down $0.12 or -0.19% at $64.25

- Natural Gas down $0.04 or -1.27% at $3.098

- Gold spot down $10.5 or -0.21% at $5047.96

- Copper down $6.05 or -1.01% at $590.2

- Silver down $1.14 or -1.37% at $82.1695

- Platinum down $21.59 or -1.02% at $2102.21

Time: 10:30 GMT (05:30 ET)

| Date | GMT/Local | Impact | Country | Event |

| 10/02/2026 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 10/02/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 10/02/2026 | - | *** | New Loans | |

| 10/02/2026 | - | *** | Money Supply | |

| 10/02/2026 | - | *** | Social Financing | |

| 10/02/2026 | 1330/0830 | *** | Employment Cost Index | |

| 10/02/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/02/2026 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 10/02/2026 | 1800/1300 | Dallas Fed's Lorie Logan | ||

| 10/02/2026 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/02/2026 | 0130/0930 | *** | CPI | |

| 11/02/2026 | 0130/0930 | *** | Producer Price Index | |

| 11/02/2026 | 0900/1000 | * | Industrial Production | |

| 11/02/2026 | 1020/1120 | ECB's Cipollone In Digital Finance Conference Fireside Chat | ||

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack |