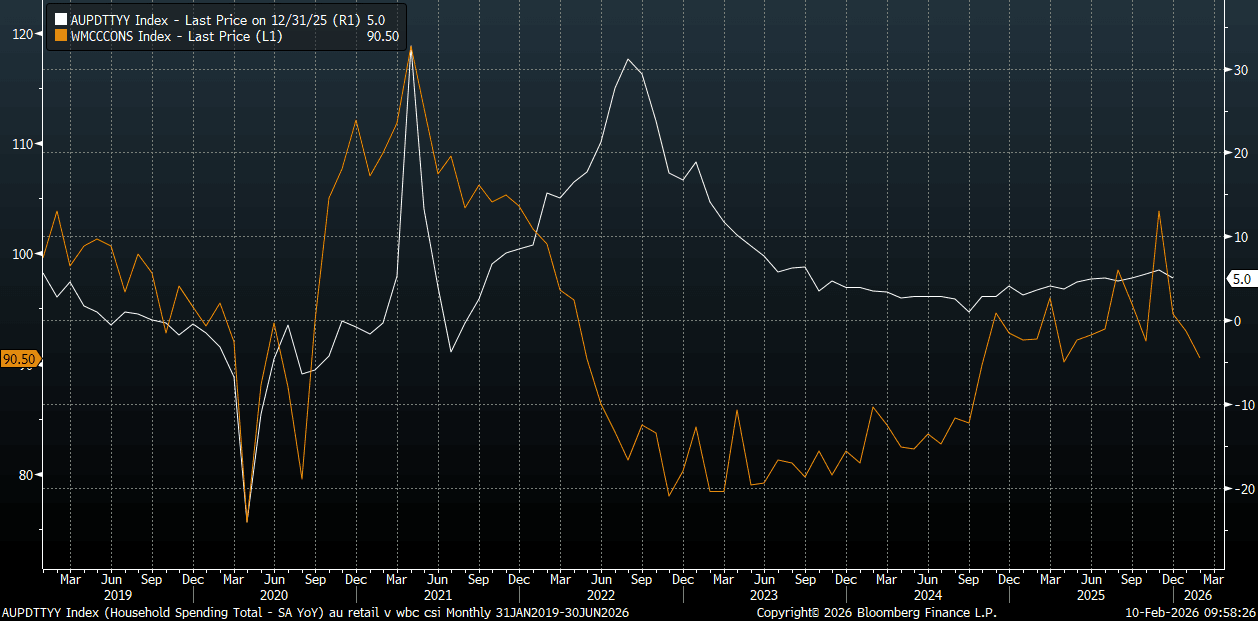

AUSTRALIA DATA: Consumer Sentiment Falls, Household Spending May Soften Further

The Feb Westpac Consumer Sentiment Index print fell 2.6% to 90.5 (from 92.9). This puts the index back close to lows from 2025, and comfortably off Nov highs of 103.8. The index spent a lot of late 2022 to late 2024 in a rough 80-85 region, so we remain above these levels. The chart below plots the consumer sentiment reading against the Australian household spending measure, y/y (which came yesterday and moderated to 5%y/y). The m/m correlation between the two series' is soft but the general trends can follow each other. Spending started to improve as sentiment lifted late in 2024 from very depressed levels. The move off recent highs for sentiment points to some downside risks in household spending, but arguably the RBA needs this to aid the return of inflation to target.

- Westpac notes in terms of today's result: "Muted response compared to previous rate hikes. Current conditions and medium term outlook weaken; year-ahead views stable. Over 80% expect interest rates to rise further in the next 12 months."

- It adds: "The RBA has already signalled that the volatility of the new monthly CPI means it will continue to focus more closely on the quarterly price data, particularly for trimmed mean inflation. With the next quarterly update due in late April likely to show inflation still uncomfortably high, this points to the next 25bp rate hike coming in May."

Fig 1: Westpac Consumer Sentiment Index & Household Spending Y/Y

Source: Westpac/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore