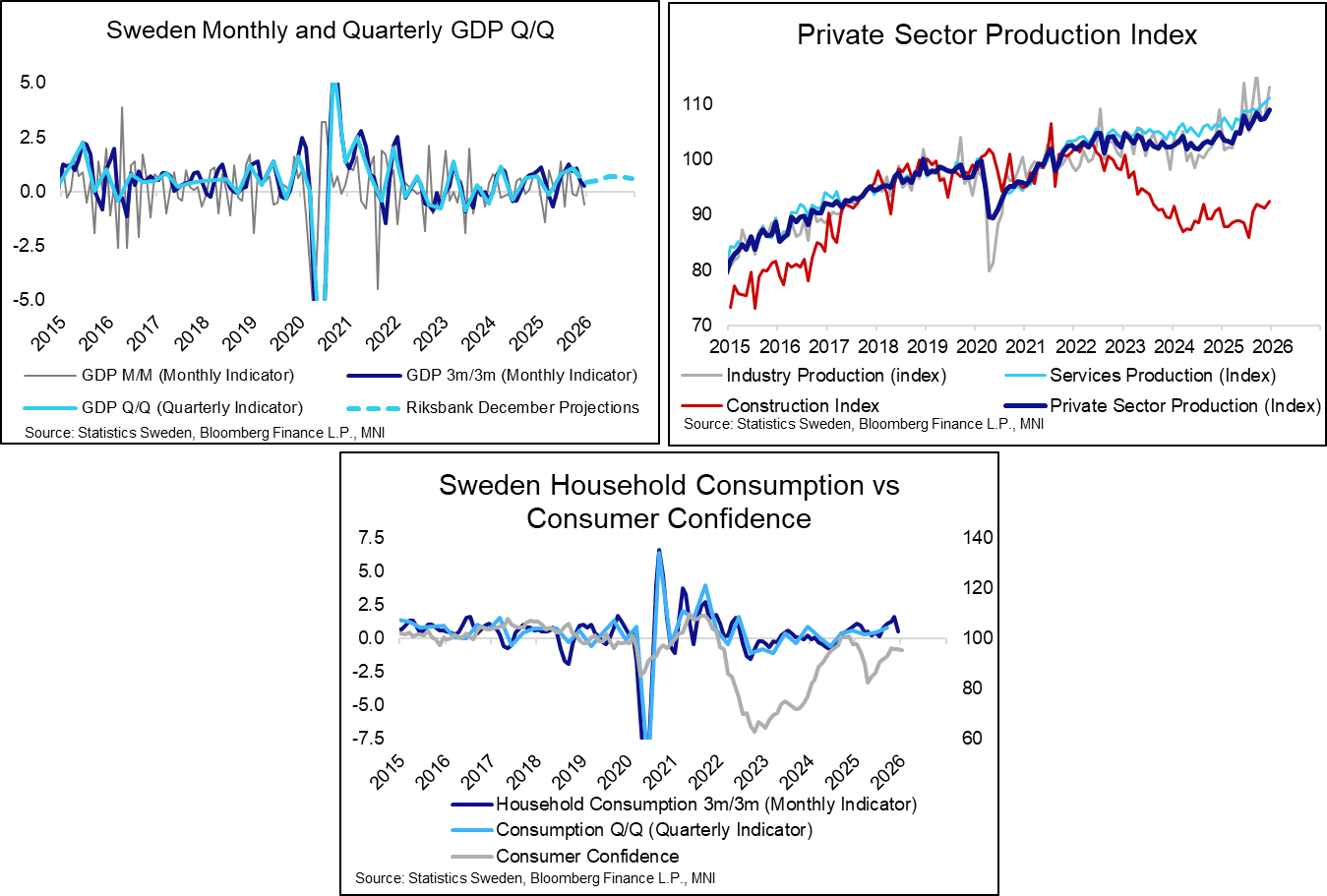

SWEDEN: Consumption Eases In December But Quarterly Growth Still Positive

This morning’s Swedish activity data provides some context to the weaker-than-expected Q4 flash GDP reading (0.2% Q/Q vs 0.4% Riksbank, 0.5% consensus). It doesn’t call into question the Riksbank’s expectations for growth to continue to strengthen through this year. Focus remains on the final Q4 GDP report on February 27, given the flash release is often sensitive to revisions.

- After growing solidly in October and November, household consumption pulled back 3.7% M/M in December. That left 3m/3m growth at 0.5% (vs 1.6% in Nov, 1.3% in Oct, 1.1% in Sep).

- Private sector production rose 1.6% M/M in December, leaving 3m/3m growth steady at 0.8%. Across sectors, industry looks to have made a negative contribution to total production in Q4 (-0.9% 3m/3), offset by growth in services (1.3% 3m/3m) and the rate-sensitive construction (2.6% 3m/3m).

- The positive on the industrial production side is that despite a 7.9% M/M fall in December, the volatile industrial orders series still registered 8.2% 3m/3m growth into year-end. Orders are generally considered a leading indicator of actual production outcomes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore