NORWAY: January CPI-ATE Sees Broad-based Strength, Rents and Insurance Noted

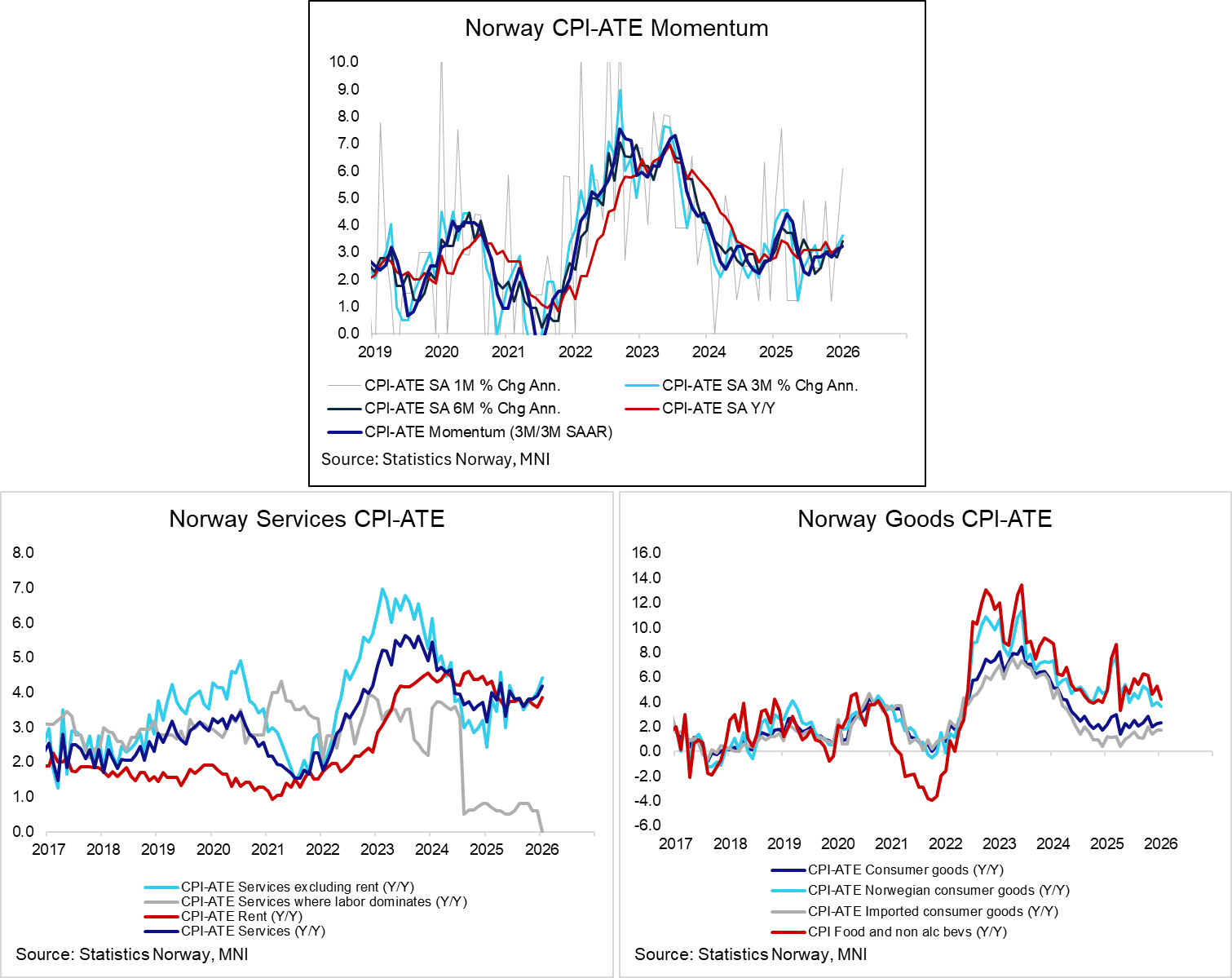

The January acceleration in Norwegian CPI-ATE inflation looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. There may be scope for some payback in February owing to a significant acceleration in airfares, but that won’t be enough to ease Norges Bank concerns around inflation persistence. On a seasonally adjusted basis using Statistics Norway data, CPI-ATE rose 0.49% M/M in January, the highest sequential reading since February 2025. That pulled 3m/3m inflation momentum up to 3.22% (vs 3.09% prior), a 9-month high.

- Statistics Norway notes that “It was particularly the development in rents and the prices of cars and electricity that lifted price inflation in January. The growth was nevertheless quite broad-based, with few goods and service groups where prices decreased. “

- Rent inflation was 3.86% Y/Y (vs 3.57% prior). As expected, rents now have a larger weight in the inflation basket, exacerbating their role in keeping CPI-ATE elevated.

- Services ex-rent inflation rose to 4.42% Y/Y (vs 4.02% prior), despite a base effect driven fall in services where labour dominates (0.00% Y/Y vs 0.61% prior). Insurance and financial services inflation was 8.45% Y/Y (vs 7.85% prior), while restaurants and hotels was 5.85% Y/Y (vs 5.11% prior). Note the volatile airfare categories saw annual inflation of 11.2% Y/Y, which may see some payback in February.

- Domestic goods inflation eased to 3.67% Y/Y (vs 3.94% prior) while imported inflation was steady at 1.73% Y/Y (vs 1.72% prior). There was a welcomed pullback in food and non-alcoholic beverages to 4.23% Y/Y (vs 5.92% prior), offset by accelerations in clothing and footwear and furniture and household equipment.

- Headline inflation was pushed higher by an expected increase in the EV VAT rate, alongside a rise in electricity prices. However, these do not filter into CPI-ATE (which excludes tax changes and energy).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore