MNI US OPEN - France, Spain Flash HICPs Softer-Than-Expected

EXECUTIVE SUMMARY

- RUSSIA SAYS IT WANTS TO BALANCE RELATIONS WITH THE US AND CHINA

- GOODS AND ENERGY DROVE SOFTER-THAN-EXPECTED FRENCH CPI

- UK RETAIL SALES SEE STRONG FEB JUMP

- STRONGEST MYANMAR QUAKE IN A CENTURY ROCKS THAILAND, VIETNAM

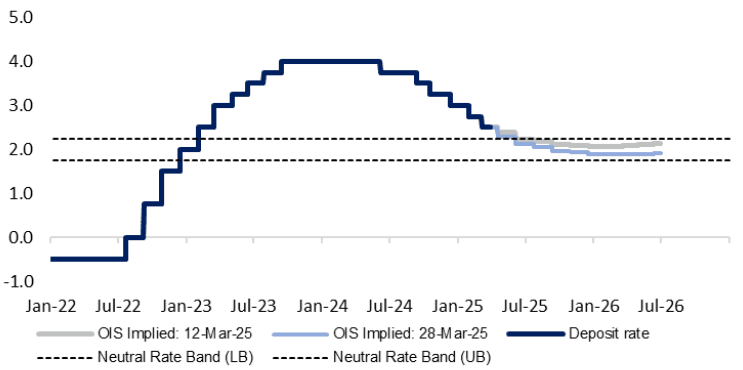

Figure 1: Dovish repricing in EUR STIRs on soft FR/SP flash HICP data

Source: MNI/Bloomberg

NEWS

US/RUSSIA/CHINA (BBG): Russia Says It Wants to Balance Relations With the US and China

Moscow must balance its ties with both Beijing and Washington, a top Russian official said, highlighting the emergence of a new geopolitical dynamic between President Vladimir Putin, China’s Xi Jinping and Donald Trump. “As to the relationship between Russia, China and the United States, we should not develop a relationship with one other country at the expense of another and vice versa,” Deputy Prime Minister Alexei Overchuk told an audience Friday at the Boao Forum in the southern Chinese province of Hainan.

US/IRAN (BBG): Iran Says It Responded to Trump Letter on Nuclear Talks

Iran’s foreign minister said his country responded to a letter from US President Donald Trump on the prospect of new talks over Tehran’s nuclear program, without giving detail on the contents. Abbas Araghchi told the state-run Islamic Republic News Agency that the reply was sent Wednesday via Oman, a longtime mediator between Iran and the US, two weeks after a top diplomat from the United Arab Emirates handed Trump’s letter to officials in Tehran.

US (WSJ): Trump Warned U.S. Automakers Not to Raise Prices in Response to Tariffs

When President Trump convened CEOs of some of the country’s top automakers for a call earlier this month, he issued a warning: They better not raise car prices because of tariffs. Trump told the executives that the White House would look unfavorably on such a move, leaving some of them rattled and worried they would face punishment if they increased prices, people with knowledge of the call said.

ASIA (BBG): Strongest Myanmar Quake in a Century Rocks Thailand, Vietnam

Myanmar was struck by its biggest earthquake in a century, shaking buildings and triggering evacuations in neighboring Vietnam and Thailand, with least one tower collapsing in Bangkok. The quake on Friday measured 7.7 in magnitude, according to the USGS, which said it was 16 kilometers northwest of Sagaing, Myanmar and at a depth of 10 kilometers. It struck at about 1:21 p.m. in Bangkok and was the strongest worldwide since 2023, according to the US Geological Survey data compiled by Bloomberg. There was a second temblor of 6.4 magnitude around the same area, the USGS said.

ECB (MNI): Tariff Inflation Impact Balances Out - ECB's Guindos

U.S. tariffs and potential retaliation in Europe would boost inflation in the short term but this would be balanced in the medium term by a hit to economic growth, European Central Bank Executive Board member Luis de Guindos said on Friday. De Guindos was confident in that the ECB is on its way to reaching its 2% inflation target, but stressed that it should remain cautious regarding future movements due to the great level of uncertainty.

ITALY (FT): Italy’s Giorgia Meloni Rejects ‘Childish’ Choice Between Trump and Europe

Giorgia Meloni has dismissed the idea that Italy will have to choose sides between the US and Europe as “childish” and “superficial”, insisting she would do whatever is necessary to defend her country’s interests. In her first interview with a foreign newspaper since coming to office in 2022, the Italian prime minister said it was “in the interests of everyone” to overcome severe strains in the transatlantic relationship, describing some European leaders’ reactions to Donald Trump as “a bit too political”. Italy’s nationalist conservative leader made clear she did not see the US president as an adversary and she would continue to respect Italy’s “first ally”.

BOJ (MNI): BOJ Board Split On Rate Hike; U.S. Concerns - Opinions

Bank of Japan board members were mixed over the next rate hike on the back of improved underlying inflation and the downside risk to the U.S. economy at the March 18-19 meeting, the summary of opinions released Friday showed. “During the phase of the next policy interest rate hike, underlying CPI inflation may be fairly close to the 2% price stability target," one member noted. "Therefore, the Bank will need to consider options including a shift from its current accommodative monetary policy stance to a neutral one.”

JAPAN (BBG) Ishiba Pledges Measures to Protect Jobs From Trump’s Car Tariffs

Japanese Prime Minister Shigeru Ishiba pledged to take thorough measures to protect local jobs from the Trump administration’s 25% tariff on US car imports, which he said will have a “very big” impact on the nation’s economy. Ishiba emphasized the need to consider measures to help Japanese companies with financing while the government tries to grasp the entire scope of the impact on the nation’s key industry.

AUSTRALIA (BBG): Australia’s PM Calls May 3 Election as Polls Show Tight Race

Australia’s Prime Minister Anthony Albanese has called an election for May 3, kicking off what’s expected to be a closely-fought campaign centered on cost-of-living pressures and a housing crisis in a sluggish economy. Albanese is campaigning to become the first Australian leader in more than two decades to win consecutive elections, a symptom of the long-running political fragmentation which has threatened the nation’s prized stretch of prosperity.

BANXICO (MNI): Dovish Banxico Indicates at Least One More 50bp Cut

The Central Bank of Mexico signaled Thursday it will deliver at least one more 50-basis-point cut at its next meeting in May, following the decision to reduce interest rates by a half point to 9.00%. The dovish move came amid significant improvement in inflation and weakness in economic activity. "The Board estimates that looking ahead it could continue calibrating the monetary policy stance and consider adjusting it in a similar magnitudes. It anticipates that the inflationary environment will allow to continue the rate cutting cycle, albeit maintaining a restrictive stance," the English version of statement said.

DATA

ECB DATA (MNI): 1/3-year Ahead Inflation Expectations Unchanged, Growth Expectations Fall

- ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

- ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.4%

The ECB's February consumer expectations survey saw 1- and 3-year ahead median inflation expectations unchanged at 2.6% and 2.4% respectively. Bloomberg consensus had expected 1-yer ahead expectations to fall slightly to 2.5%. The release notes that "uncertainty about inflation expectations over the next 12 months decreased slightly in February to its lowest level since January 2022". 1-year ahead economic growth expectations fell a tenth to -1.2%, but remain above December's -1.3%. It's worth noting that this survey will not capture any expected growth impulse from the recent step change in the EU (particularly German) fiscal/defence spending complex. That may be reflected in next month's release.

UK DATA (MNI): UK Retail Sales See Strong Feb Jump

- UK FEB RETAIL SALES +1% M/M, +2.2% Y/Y

UK retail sales volumes rose sharply in February 2025, up 1.0% m/m and building on a strong but downwardly revised 1.4% jump in January, the Office for National Statistics said Friday. Non-food store sales volumes grew strongl, with rises across all four sub-sectors (department, other non-food, clothing, and household goods stores), although supermarket sales volumes fell back following a strong rise in January 2025. Year-on-year, sales rose 2.2% in Feb.

UK Q4 GDP +0.1% Q/Q, +1.5% Y/Y (MNI)

UK JAN TRADE BALANCE GBP -0.6BN (MNI)

UK JAN VISIBLE TRADE BALANCE GBP -17.85BN (MNI)

UK JAN NON-EU TRADE BALANCE GBP -7.07BN (MNI)

FRANCE DATA (MNI): Goods and Energy Drove Softer-Than-Expected French CPI

- FRANCE MAR CPI +0.2% M/M, +0.8% Y/Y

- FRANCE MAR HICP +0.2% M/M, +0.9% Y/Y

- FRANCE FEB PPI -0.8% M/M, -1.4% Y/Y

Looking at the drivers of the national French March flash CPI (non-HICP) surprise (0.80% Y/Y vs 0.9% rounded cons), there were pullbacks in annual energy and non-energy industrial goods inflation. This was offset somewhat by accelerations in services and food inflation. Services inflation was 2.33% Y/Y (vs 2.23% in Feb, 2.45% in Jan). The press release highlights accelerations in insurance products, but no further details are available at this stage. Monthly NSA price growth was 0.06% M/M.

FRANCE FEB CONSUMER SPENDING -0.1% M/M, +0.1% Y/Y (MNI)

FRANCE FEB CONSUMER MANUF SPENDING -0.1% M/M, -0.3% Y/Y (MNI)

SPAIN DATA (MNI): Soft March HICP Data, Lower on Power, Fuels, Recreation

- SPAIN MAR FLASH CPI +0.1% M/M, +2.3% Y/Y

- SPAIN MAR FLASH CORE CPI +2% Y/Y

- SPAIN MAR FLASH HICP +0.7% M/M, +2.2% Y/Y

Spanish March preliminary HICP came in lower than expected on the yearly rate at +2.2% Y/Y (vs +2.5% cons; +2.9% prior) and the sequential reading at 0.7% M/M (0.9% cons; 0.4% prior). The national CPI also came in below expectations at +2.3% Y/Y (vs 2.6% cons; 3.0% prior) and 0.1% M/M (vs 0.4% cons; 0.4% prior). Core CPI came in below expectations, at +2.0% Y/Y (vs 2.1% cons; 2.2% prior). Core HICP was 2.0% Y/Y, also. The headline rate was driven lower by electricity prices, and, to a lesser extent, by auto fuels as well as leisure and culture prices, INE adds.

SWEDEN DATA (MNI): Retail Sales Momentum Remains Firm Despite Weak Consumer Confidence

Swedish retail sales momentum remains firm, which should provide a tailwind to Q1 household consumption even as consumer confidence indicators weaken. Since the strikingly large rise in December 2024, the retail sales index has pulled back a little, but remains above any level seen between December 2022- November 2024. In February, sales rose 2.8% Y/Y (vs 3.1% prior) and 0.1% M/M. The monthly NSA print appears broadly in line with seasonal norms over the past 10 years. That sees 3m/3m momentum at 2.2%, up from 1.4% in February for its highest since June 2021.

SWITZERLAND DATA (MNI): KOF Uptick Suggests Robust Economic Outlook

- SWISS KOF MAR ECONOMIC BAROMETER 103.9

The Swiss KOF Economic Barometer rose to 103.9 in March, 1.3 points above an upwardly revised February print which is now standing at 102.6 (from 101.7). This is the highest index value since May 2024, and points towards "the outlook for the Swiss economy remain[ing] robust". Detailed commentary from the KOF suggests to us that the March uptick was broad-based: "The production-side indicator bundles included in the Barometer reflect these positive developments. In particular, the indicator bundles for manufacturing, for other services, and for the construction industry indicate a more favourable outlook than before."

JAPAN DATA (MNI): Japan March Tokyo Core CPI Rises 2.4% vs. Feb 2.2%

- JAPAN MAR TOKYO CORE CPI +2.4% Y/Y; FEB 2.2%

- JAPAN MAR TOKYO CORE-CORE CPI +2.2% Y/Y; FEB 1.9%

- JAPAN MAR SERVICES PRICES +0.8% Y/Y; FEB +0.6%

The year-on-year rise in the Tokyo core inflation rate accelerated to 2.4% in March from February’s 2.2%, above the Bank of Japan's 2% target for the fifth straight month, data from the Ministry of Internal Affairs and Communications showed on Friday. Food prices excluding perishables (+5.6% vs. +5.0%) and households’ durable goods (+7.7% vs. +5.5%) boosted the index, despite lower energy prices (+6.1% vs. +6.9%). The core-core CPI (excluding fresh food and energy) – a key indicator in the underlying trend of inflation – rose 2.2% y/y in March, also accelerating from 1.9% in February and rose above 2% for the first time since March 2024.

FOREX: Softer Eurozone Inflation Prints Moderately Weigh on EUR

- Softer inflation prints from both France and Spain have moderately weighed on the Euro this morning, taking EURUSD around 30 pips lower from 1.0800 to 1.0770 at typing. Dampened sentiment for equities across APAC has spilled over to the major benchmarks, contributing to a leg lower for EURJPY, which sits 0.55% in the red on Friday.

- Despite USDJPY showing some tentative signs of a bullish breakout on Thursday, a reversal back below 151.00 during APAC today has seen this momentum stall. The renewed pessimism in the equity space has prompted an extension lower for USDJPY to the 150.50 region.

- Risk sensitive currencies are suffering the most in G10, and the New Zealand dollar is the weakest performer, as NZDUSD tracks back to 0.5710/20, off ~0.40% for the session. Overnight, weaker ANZ consumer confidence, along with barely positive filled jobs growth, has provided a headwind for the kiwi, combining with the slump in regional equities. For NZDUSD current levels are close to week to date lows and also the 50-day EMA support point. Earlier March lows were just under 0.5600. NZDJPY is one of the weakest crosses today, declining 0.67% ahead of the NY crossover.

- GBP trades more resiliently around 1.2950 following a constructive set of retail sales / activity data, consolidating some moderate gains on the week. Approaching yesterday’s value date month- and quarter end fixing window, GBP appeared to particularly benefit as the market shrugged off the bullish dollar signals, although 1.3000 has capped the GBPUSD topside for now.

- Moving average studies are in a bull-mode position highlighting a dominant uptrend for cable. A continuation higher and a breach of 1.3015, the Mar 20 high and bull trigger, would initially target 1.3048.

- Highlighting the Friday calendar is monthly GDP from Canada, is scheduled, the US PCE report and the U. of Mich index final read for March. Fedspeak from Barr and Bostic is also on tap.

BONDS: Gilts Display Resilience With Supply Weighing on EGBs

After opening 1bp wider, the 10-year Gilt/Bund spread now trades ~1.5bps tighter on the session at 200bps, with UK paper dispalying a little more resilience than EGB peers as the European session progresses.

- Heavy impending Italian supply is probably capping upside in EGBs, with E2.5-3.0bln of the on-the-run 5-year 2.95% Jul-30 BTP and E2.50-3.25bln of the on-the-run 10-year 3.65% Aug-35 BTP due at 1000GMT.

- That’s despite the French and Spanish March flash inflation prints coming in softer-than-expected earlier, helping the ECB-dated OIS implied probability of a 25bp cut on April 17 move to ~85% (vs 75% at yesterday’s close).

- The Eurozone-wide flash inflation reading is due on April 1, with German and Italian data due next Monday. MNI’s preview is here

- Bund futures are +45 ticks at 128.80, down from a high of 129.07. The Jan 14 low at 129.41 remains a key short-term resistance level.

- German yields are 2.5-5.0bps lower, with the curve bull flattening. 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels.

- Gilt futures are +49 ticks at 91.19. Yesterday’s high is unchallenged, with bearish technical intact. Initial support and resistance at 90.55/91.82, respectively.

- Gilt yields are 3.0-5.0bps lower, with the belly outperforming.

- While this morning’s UK retail sales data (firmer headline, negative revisions) was a net positive for the UK consumption outlook, we remain wary of interpreting too much from even a couple of positive UK retail sales prints.

- Global macro focus turns to the US PCE inflation report at 1230GMT.

EQUITIES: E-Mini S&P Extends Pullback From Tuesday's High

The medium-term trend direction in Eurostoxx 50 futures is up and recent short-term weakness - for now - appears corrective. Support to watch is the 50-day EMA, at 5296.44. It has been pierced. A clear break of it would highlight a stronger short-term bear threat and expose 5229.00, the Mar 11 low and a bear trigger. On the upside, the bull trigger is 5516.00, the Mar 3 high. Clearance of this level would resume the uptrend. S&P E-Minis have pulled back from Tuesday’s high. The trend condition is bearish and gains since Mar 13 are considered corrective. However, note that the 20-day EMA has recently been breached. A resumption of gains would open 5864.25, the Jan 13 low. Moving average studies are in a bear-mode set-up, highlighting a dominant downtrend. A stronger reversal lower would refocus attention on 5559.75, the Mar 13 low and bear trigger.

- Japan's NIKKEI closed lower by 679.64 pts or -1.8% at 37120.33 and the TOPIX ended 58.22 pts lower or -2.07% at 2757.25.

- Elsewhere, in China the SHANGHAI closed lower by 22.442 pts or -0.67% at 3351.307 and the HANG SENG ended 152.2 pts lower or -0.65% at 23426.6.

- Across Europe, Germany's DAX trades lower by 156.83 pts or -0.69% at 22527.52, FTSE 100 lower by 2.83 pts or -0.03% at 8668.93, CAC 40 down 43.47 pts or -0.54% at 7955.72 and Euro Stoxx 50 down 27.79 pts or -0.52% at 5353.62.

- Dow Jones mini down 102 pts or -0.24% at 42510, S&P 500 mini down 18.75 pts or -0.33% at 5720.75, NASDAQ mini down 107.5 pts or -0.54% at 19884.25.

Time: 08:50 GMT

COMMODITIES: WTI Futures Remain Above Key Resistance at 50-Day EMA

Despite recent gains, a bearish trend condition in WTI futures remains intact, and gains this month are considered corrective. However, a key resistance at $69.17, the 50-day EMA, has been pierced. The breach strengthens a bullish theme and opens $70.98, the Feb 25 high. For bears, a reversal lower would expose the bear trigger at $64.85, the Mar 5 low. Clearance of this level would resume the downtrend and open $63.73, the Oct 10 ‘24 low. The trend condition in Gold is unchanged, it remains bullish. Today’s strong gains have resulted in a clear breach of $3057.5, the Mar 20 high and a bull trigger. This confirms a resumption of the primary uptrend and also highlights fresh all-time highs for the yellow metal. Sights are on the $3100.0 handle and $3106.8, a Fibonacci projection. Support to watch lies at $2982.7, the 20-day EMA.

- WTI Crude down $0.11 or -0.16% at $69.62

- Natural Gas down $0.04 or -0.89% at $3.891

- Gold spot up $14.45 or +0.47% at $3068.66

- Copper down $4.65 or -0.91% at $508.05

- Silver up $0.04 or +0.12% at $34.3125

- Platinum down $3.16 or -0.32% at $987.14

Time: 08:50 GMT

| Date | GMT/Local | Impact | Country | Event |

| 28/03/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 28/03/2025 | 1100/1200 | ** | PPI | |

| 28/03/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 28/03/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 28/03/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 28/03/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 28/03/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 28/03/2025 | 1615/1215 | Fed Governor Michael Barr | ||

| 28/03/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 28/03/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 28/03/2025 | 1930/1530 | Atlanta Fed's Raphael Bostic |