SWITZERLAND DATA: KOF Uptick Suggests Robust Economic Outlook

Mar-28 08:43

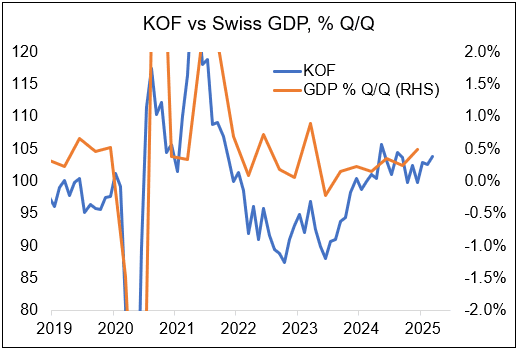

The Swiss KOF Economic Barometer rose to 103.9 in March, 1.3 points above an upwardly revised February print which is now standing at 102.6 (from 101.7). This is the highest index value since May 2024, and points towards "the outlook for the Swiss economy remain[ing] robust".

- Detailed commentary from the KOF suggests to us that the March uptick was broad-based: "The production-side indicator bundles included in the Barometer reflect these positive developments. In particular, the indicator bundles for manufacturing, for other services, and for the construction industry indicate a more favourable outlook than before. The demand-side indicator bundles for private consumption also increase, while the indicator bundles for foreign demand remain unaltered"

- The SNB last week reiterated its previous call for 1.0-1.5% real GDP growth in Switzerland - for 2026, it expects 1.5% growth. The median sellside forecast seen by MNI mirrors that view, seeing 2025 growth around the middle of the SNB's range, at 1.3% - the figure was unrevised during the last three months. Solid KOF figures should underpin these estimates going forward.

- Yesterday, we've reviewed Swiss (and CHF) exposure to potential pharmaceutical tariffs from the US administration - for our analysis, see 'Relatively Most Exposed to Potential Pharma Tariffs [1/2]' and 'Analysts Suggest Pharma Tariff Impact May Be Limited [2/2]'.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Feb26 NY cut 1000ET (Source DTCC)

Feb-26 08:42

- EUR/USD: $1.0400(E1.1bln), $1.0420-35(E2.6bln), $1.0440-50(E2.8bln), $1.0460-75(E1.6bln), $1.0495-00(E1.6bln), $1.0510-30(E5.0bln), $1.0550(E1.4bln)

- USD/JPY: Y149.00($956mln), Y150.00($833mln), Y150.20-25($780mln), Y151.00($1.4bln), Y151.95($1.0bln)

- EUR/JPY: Y155.00(E927mln)

- GBP/USD: $1.2675(Gbp619mln)

- AUD/USD: $0.6400(A$817mln)

- USD/CAD: C$1.3500($1.2bln), C$1.4300($784mln), C$1.4390-00($1.4bln)

- USD/CNY: Cny7.3500($1.2bln)

CROSS ASSET: A $3.3k bounce in Bitcoin

Feb-26 08:31

- Bitcoin has managed to bounce back above that 50% retracement noted Yesterday at $88,027.59, this is the retracement post the US Election rally.

- Bitcoin lost a whopping ~10.55k in just the last two sessions, and after bouncing some ~3.3k from Yesterday's low, it is drifting back down to that $88,027.59 level.

- Next supports are still seen at 85,133.12, followed by 83,021.19, 61.8% retracement of the US Election Rally.

(Chart source: MNI/Bloomberg).

GILTS: Flat Start, Global Cues Still Eyed

Feb-26 08:23

Gilts little changed with Bunds and Tsys off lows ahead of the UK open.

- Core global FI came under pressure in Asia on the back of increased odds of U.S. tax cuts.

- M5 futures -6 at 93.17, narrow 93.12-24 range to start.

- Initial resistance at the Feb 13 high (93.39), with the bullish technical theme intact in the contract.

- Roll completion stands at ~85% ahead of tomorrow’s first notice for H5.

- Yields little changed to 1bp lower across the curve.

- Little of note on the UK data calendar today,

- BoE dove Dhingra will speak on “Trade fragmentation and monetary policy” from 16:30 GMT, don’t expect a change in tone after she reaffirmed her dovish stance earlier in the week (pushing back against the idea of gradual cuts given her view on consumption).

Trending Top

Jan-30 21:43

Jan-30 21:11