MNI US OPEN - Equities Drift, AI Valuations Still a Concern

EXECUTIVE SUMMARY

- US BANKS SHELVE $20 BILLION BAILOUT PLAN FOR ARGENTINA – WSJ

- BOJ'S UEDA WARNS OF WEAK YEN IMPACT ON CPI

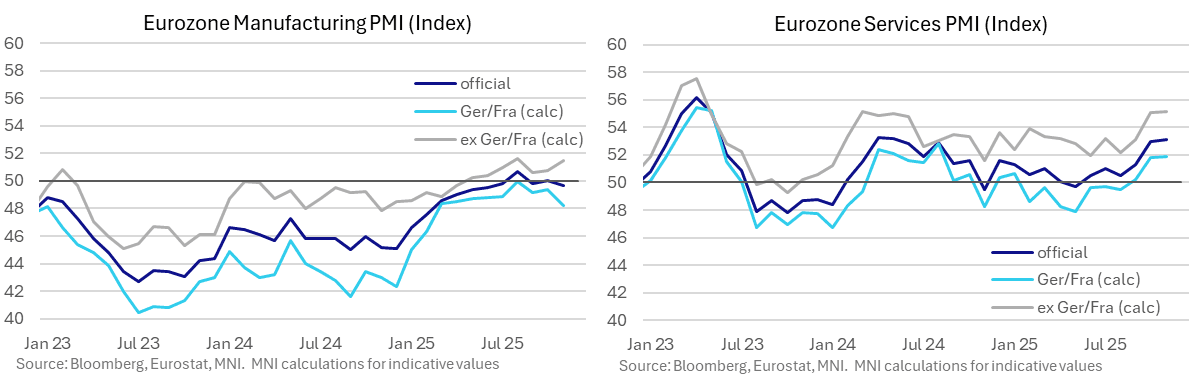

- EUROZONE PMIs EX-GERMANY AND FRANCE STILL OUTPERFORMING

- UK GOV'T OCT YTD BORROWING SECOND HIGHEST ON RECORD

Figure 1: Eurozone ex-Germany/France PMIs continue to stand out as an outperformer

NEWS

US/ARGENTINA (WSJ): U.S. Banks Shelve $20 Billion Bailout Plan for Argentina

A planned $20 billion bailout to Argentina from JPMorgan Chase, Bank of America and Citigroup has been shelved as bankers pivot instead to a smaller, short-term loan package to support the financially distressed government, people familiar with the matter said. Treasury Secretary Scott Bessent and the Trump administration had been seeking to bolster Argentine President Javier Milei’s pro-reform party when they announced a pair of financial lifelines this fall. The package included a $20 billion currency swap with the U.S. Treasury Department and plans for a separate $20 billion bank-led debt facility.

FED (MNI): Fed's Paulson Eyes Dec. Meeting With Caution

Philadelphia Federal Reserve Bank President Anna Paulson said Thursday she is taking a guarded approach to next month's decision on whether to keep cutting interest rates because borrowing costs are already close to neutral. "Each rate cut raises the bar for the next cut. And that’s because each rate cut brings us closer to the level where policy flips from restraining activity a bit to the place where it is providing a boost. So, I am approaching the December FOMC cautiously," she said in prepared remarks.

ECB (BBG): New ECB Outlook Unlikely to Differ Much From EU’s, Guindos Says

New European Central Bank projections next month will probably be similar to the latest forecasts from the European Commission, according to Vice President Luis de Guindos. The remarks suggest the ECB’s new outlook will also point to inflation near or at 2% in 2026 and 2027. The commission’s calculations, however, don’t include the effect of a likely delay in a new carbon-pricing system, which risks lowering the latter number.

ECB (MNI): Lagarde Stresses Need to Enhance Domestic Demand; No MonPol Signals

ECB President Lagarde's speech at the European Banking Congress is not focused on monetary policy. Rather it discusses pathways to enhance domestic demand as a driver of Eurozone growth performance. The title of the speech is "From resilience to strength: unleashing Europe's domestic market". Worth noting that ECB speakers have

recently been describing the economy as "resilient", even with downside risks still present.

EUROPE/UKRAINE (BBG): Germany’s Merz Holds Urgent Ukraine Call With Leaders

German Chancellor Friedrich Merz canceled his plans in order to join an urgent call with other leaders about a US-Russian plan to end the war in Ukraine. Merz had been scheduled to visit a school in Berlin Friday morning but changed his plans in order to formulate a response to the US-Russian plan, according to a German government official.

UK/CHINA (The Times): Keir Starmer to Approve Chinese Embassy Plan With Blessing of MI5

Sir Keir Starmer is expected to formally approve a new super-sized Chinese embassy in the heart of London next month after being given the green light by MI5 and MI6. The Times has been told that the Home Office and the Foreign Office will not raise any formal objections to the plan, providing that appropriate “mitigations” are put in place to protect national security.

SNB (BBG): Swiss Inflation Will Pick Up Moderately, SNB’s Tschudin Says

Swiss inflation will quicken moderately over the coming quarters, Swiss National Bank Board Member Petra Tschudin said, according to a slide presentation published by the central bank. Tschudin also said SNB expects growth in the world economy to be subdued over coming quarters, US tariffs are at a historically high level.

INDIA (MNI): RBI Loosen Grip on Rupee as Trade Uncertainty, Flows Continue to Weigh

Persistent intervention from the RBI is a key feature of Indian currency markets, and the 88.70-88.80 region for USDINR emerged as a key ‘line in the sand’ for RBI action since September. The surge higher in spot above this level today suggests that the central bank is loosening its grip on the currency as investor unease over the lack of a US-India trade agreement, persistent outflows from local assets, and the broad-based recovery for the USD Index off the September lows all weigh on sentiment. Reuters report that the RBI was seen stepping in today at higher levels, at around 89.50.

BOJ (MNI): BOJ's Ueda Warns of Weak Yen Impact on CPI

Bank of Japan Governor Kazuo Ueda on Friday warned that the weak yen could raise import costs and domestic prices, ultimately putting upward pressure on consumer prices. Speaking to lawmakers at an upper house panel, Ueda said the BOJ needs to monitor how the weak yen affects corporate wage- and price-setting behaviour, which are influenced by inflation expectations. He added that the bank is closely watching how currency movements could impact expected inflation and the underlying CPI, which is a key focus of the BOJ.

BOJ (MNI): BOJ Studying Wage Growth Pace - Ueda

Bank of Japan Governor Kazuo Ueda on Friday said the bank is collecting data to assess the initial momentum for wage growth in fiscal 2026 and intends to use this information in policy decisions at or after the next policy-setting meeting. Ueda told lawmakers that the probability of achieving the 2% inflation target is gradually increasing, as downside risks to the U.S. economy have eased somewhat. He added that the bank needs to monitor whether downward pressure from trade policy impacts on corporate profits is negatively affecting corporate wage- and price-setting behaviour.

JAPAN (MNI): Japan’s Govt Approves JPY21.3 Trln Economic Package

The Japanese government on Friday approved a comprehensive economic package worth JPY21.3 trillion ($135 billion) at a cabinet meeting, marking the first major economic policy move under Prime Minister Sanae Takaichi, who has advocated “responsible and proactive public finances,” the Nikkei reported. Of the total, JPY11.7 trillion – including tax cuts – will fund measures to ease the impact of rising prices on households, while JPY7.2 trillion is earmarked for growth-focused investments in sectors such as semiconductors, artificial intelligence, and shipbuilding.

CHINA (MNI INTERVIEW): China RatingDog PMI to Remain Above 50

The founder of RatingDog provides insight into China's private manufacturing purchasing managers index. On MNI Policy MainWire now, for more details please

contact sales@marketnews.com

RBA (MNI INTERVIEW): RBA at Risk of Q1 Hike - McKibbin

A former RBA board member shares his cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBNZ (MNI INTERVIEW): RBNZ Done Easing After Next Cut - Former Economist

A former RBNZ economist shares his OCR outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

G20 (MNI): Sherpas Reach Agreement on Leaders' Declaration Despite US Pushback

Daily Maverick reports that the 'G20 sherpas reached an agreement on a Leaders' Declaration at 8.30am on Friday after negotiating through the night' despite repeated pushback from the Trump administration, which has insisted that the bloc should not adopt and publish top-level communique in the absence of its delegation. South Africa has been pushing for the adoption of a full Leaders' Declaration instead of producing a more neutral and limited Chair's Statement, which is normally released if participating countries fail to reach consensus over joint communique.

DATA

EUROZONE DATA (MNI): November Flash PMIs: EZ ex-Germany and France Still Outperforming

- EUROZONE NOV FLASH MANUF PMI 49.7 (50.1 FCAST, 50.0 OCT)

- EUROZONE NOV FLASH SERV PMI 53.1 (52.8 FCAST, 53.0 OCT)

The Eurozone-wide composite PMI has now been expansionary for eleven consecutive months. The 52.4 November reading was essentially in line with consensus and October's 52.5, with a weaker-than-expected manufacturing print offset by stronger services. The Eurozone ex-Germany/France continues to stand out as an outperformer. We estimate the ex-Germany/France manufacturing PMI at 51.5 (vs 50.8 prior) and the Germany/France reading at 48.2 (vs 49.4 prior). Meanwhile, we see the ex-Germany/France services PMI at 55.2 (vs 55.0 prior), with Germany/France at 51.9 (vs 51.8 prior).

EUROZONE DATA (MNI): Q3 Negotiated Wages Surprise to the Downside

ECB negotiated wages pulled back to 1.87% in Q3, well below the 2.45% consensus (which had a wide range of estimates ranging from 1.7-3.6%) and 4.01% prior. We had flagged downside risks to consensus in recent days. The reading may have lent some fresh support to EUR STIRs, but broader cross-asset trends look to be dominating price action this morning. The outturn is below the 2.1% implied by the ECB's forward looking wage tracker with unsmoothed one-off payments. It's possible that recent data on German/French negotiated wages will have had an impact on the downside surprise to consensus and the ECB's tracker. The ECB's series points to a rebound back to 3% in Q4.

GERMANY DATA (MNI): Composite PMI Remains Expansionary Despite Miss vs Cons

- GERMANY NOV FLASH MANUF PMI 48.4 (49.8 FCAST, 49.6 OCT)

- GERMANY NOV FLASH SERV PMI 52.7 (54.0 FCAST, 54.6 OCT)

The German composite PMI printed below consensus at 52.1 (vs 53.5 cons, 53.9 prior), with both services and manufacturing lower-than-expected. We don't read into the services miss too much though - it's still the third consecutive month of expansion and the bar set by consensus was probably too high after a very strong October. Manufacturing trends meanwhile remain sluggish, with poor export order performance weighing.

GERMANY DATA (MNI): Labour Market Deterioration Accelerated in Q3

The German labour market deterioration accelerated in Q3, as employment declined by 41k on the quarter (-0.09% Q/Q), vs -11k (-0.02%) in Q2. Industrial, information & communication and corporate service provider sectors all declined at their sharpest rates since the pandemic. The industrial sector saw its saw its ninth consecutive quarter of declining employment, at -0.47% Q/Q after -0.34% in Q2 for the weakest rate since the pandemic.

FRANCE DATA (MNI): Strong Services PMI But Weak Employment Still Noted

- FRANCE NOV FLASH MANUF PMI 47.8 (49.0 FCAST, 48.8 OCT)

- FRANCE NOV FLASH SERV PMI 50.8 (48.5 FCAST, 48.0 OCT)

A return to expansion for the services sector helped the French composite PMI handily exceed expectations at 49.9 (vs 48.1 cons, 47.7 prior). That's the highest level in 15-months. Services returned to expansion for the first time since August 2024 at 50.8 (vs 48.5 cons, 48.0 prior). However, manufacturing disappointed despite an increase

in new export sales for the first time since February 2022 (47.8 vs 49.0 cons, 48.8 prior). Despite the improvement in new orders, employment fell in both monitored

sectors. This extends a recent run of soft labour market metrics in French hard data up to Q3.

FRANCE NOV MANUF SENTIMENT 98 (VS 101 OCT) (MNI)

UK DATA (MNI): UK Gov't Oct YTD Borrowing Second Highest on Record

- UK OCT PSNB-EX GBP+17.43 BN

- UK OCT CGNCR-EX GBP21.69 BN

- UK OCT PSNCR GBP20.82 BN

UK government borrowing was GBP17.4 billion in October 2025, almost GBP 2 billion less than last October but still the third-highest October borrowing since monthly records began in 1993, the Office for National Statistics said Friday. Borrowing in the financial year to October was £116.8 billion; this was GBP9.0 billion more than in the same period in 2024 and the second-highest Apr-Oct borrowing on record after that of 2020. It currently sits almost GBP10 billion above the OBR's March forecast, underlining the scale of the fiscal challenge facing the government ahead of the budget.

UK DATA (MNI): Underlying Details Softer in PMI Prints; Another Step Towards a Dec Cut

It was a mixed UK PMI with the flash November services PMI coming in softer than expected at 50.5 (52.0 consensus, 52.3 Oct) but the manufacturing PMI beating expectations and coming in at 50.2 (49.2 consensus, 49.7 Oct). The composite PMI was softer than expected at 50.5 (51.8 consensus, 52.2 Oct). Looking at the details, services reported a "decline in new work for the first time since July".

UK DATA (MNI): October Retail Sales Decline Expected Following Four Consecutive Rises

- UK OCT RETAIL SALES INC FUEL -1.1% M/M, +0.2% Y/Y

- UK OCT RETAIL SALES EX-FUEL -1.0% M/M, +1.2% Y/Y

A slight month-on-month slowdown is expected in October's retail sales data. Bloomberg consensus sees the including fuels measure at -0.2% M/M, following four consecutive months of growth including a 0.5% M/M rise in September. Risks appear to be skewed to the downside, with estimates as low as -1.1% M/M from the sell side, and the majority of estimates looking for a negative print.

UK NOV GFK CONSUMER CONFIDENCE INDEX -19 (MNI)

JAPAN DATA (MNI): Oct Inflation Ticks Up But Services Still Sub 2% Y/Y

- JAPAN OCT CORE CPI +3.0% Y/Y; SEPT +2.9%

- JAPAN OCT CORE-CORE CPI +3.1% Y/Y; SEPT +3.0%

Japan Oct CPI was in line with market forecasts across the three inflation metrics, and a slightly tick up from the Sep outcome. Headline printed at 3.0% y/y, as did the core ex fresh food measure (both measures were 2.9% in Sep). The ex fresh food, energy measure edged up to 3.1% y/y from 3.0% prior. In terms of the detail, all of the measures in m/m terms were up 0.4%, while goods prices rose 0.3% m/m. Services posted a 0.4% m/m gain but these are often revised away.

JAPAN DATA (MNI): Japan Oct Exports Post 2nd Straight Rise

- JAPAN OCT EXPORTS +3.6% Y/Y; SEPT +4.2%

Japan’s exports rose 3.6% y/y in October, marking a second consecutive increase after September’s 4.2% gain, supported by higher shipments of semiconductors and power-generating machinery, as well as a modest pickup in automobile exports, Ministry of Finance data showed Friday. Automobile exports increased 0.4% y/y, the first rise in 10 months, following a 0.6% decline in September. Imports rose 0.7% y/y in October, also the second straight increase after a 3.3% gain in September.

JAPAN DATA (MNI): Manufacturing PMI Higher, Still Sub 50.0, Detail Positive

Japan's manufacturing PMI for Nov improved but from a low base. The print went to 48.8, from 48.2. The detail on the manufacturing print showed output rose to 49.6 from 48.3 in Oct, while new orders were also up from Oct. This points to potential for further PMI headline improvement into year end.

AUSTRALIA DATA (MNI): Nov PMIs Up, Particularly Manufacturing, Services Jobs Moderates

Australian Nov preliminary PMIs saw improvement across the board, most notably for manufacturing. The manufacturing index rose to 51.6 from 49.7. We are still short of earlier 2025 highs around 53.0, but the the turn around from Oct levels under 50.0 is notable. On The services side, we edged up to 52.7, from 52.5 prior. Again we remain off recent cycle highs, but it broadly suggests reasonably economic momentum for Q4. The composite index was at 52.6 from 52.1 in Oct. The data is second tier, but reinforces the RBA's on hold backdrop in the near term.

FOREX: USD Supported by Risk Off Sentiment, JPY Outperforming

- An extension of equity weakness early Friday is providing support to the US dollar, as the DXY edges higher towards the recovery highs at 100.36. Ongoing concerns relating to AI valuations continue to permeate global markets, and waning sentiment across crypto markets and pressure on precious metals appear to finally be providing headwinds for Cross/JPY and pressuring the EM FX basket.

- JPY is the outperformer this morning, leading USDJPY to reverse around 120 pips from yesterday’s 157.89 cycle high. Overnight inline Japanese core CPI print likely did not move the needle for the December BoJ decision as opposed to recent price action in the yen. Some profit taking dynamics may be at play heading into the weekend, and there is the potential for verbal jawboning from Japanese authorities to pick up next week.

- This week’s rally fell short of the year’s highs at 158.87, however, it is worth noting the pair has entered overbought territory, and the latest dip is seen as corrective. The prior breakout at 155 now provides initial support.

- The most notable implication of this morning's Flash PMIs perhaps were parts of the UK press release which should facilitate BoE Governor Bailey's confidence to cut in December. GBPUSD has seen some downside in recent trade, hovering just above 1.3050, and a reversal through 1.3010, the Nov 4 / 5 low, would confirm a resumption of the downtrend. Focus for GBP is on Wednesday's UK budget.

- Michigan consumer sentiment and inflation expectations alongside US wholesale sales and Canada retail sales are on the data calendar for today. A set of speakers from the ECB, the BoE, the SNB and Fed are scheduled to appear.

EGBS: Bund Futures Narrow Gap to 50-day EMA Resistance on Healthy Volumes

Core FI markets have been supported by a renewed pullback in global risk sentiment. Bund futures have moved away from session highs, but pierced resistance at the 50-day EMA (129.05) earlier, currently +36 ticks at 128.98. A clear break of this EMA would expose key resistance at 129.40 (Nov 13 high). Volumes have been healthy, with around 450k lots traded this morning.

- The Eurozone November flash composite PMI was broadly inline with consensus at 52.4 (vs 52.5 cons and prior), with a solid services reading offsetting a more subdued manufacturing print. Meanwhile, ECB Q3 negotiated wages were lower-than-expected at 1.9% (vs 2.45% consensus). However, it’s not our preferred metric of Eurozone wage growth.

- German yields are 3-4bps lower across the curve, with the belly outperforming. Zooming out, German 5s30s has steeped to a fresh multi-week high of 106.5bps this week, narrowing the gap to the year-to-date high of 111bps.

- The EUR swap curve has seen a more pronounced steepening, with pre-positioning ahead of the Dutch pension fund transition gaining traction into year-end.

- That leaves Buxl ASWs (vs 6-month Euribor) close to a YTD high of -27bps. The safe haven bid in Bunds has promoted light widening in ASWs intraday.

- EGB/Bund spreads are little changed on the day, despite the previously flagged deterioration in wider risk sentiment.

GILTS: Bull Flattening Extends, Outperformance vs. Bunds After PMIs

Soft UK services PMI data, a deterioration in wider risk sentiment and lower oil prices have driven a rally in gilts this morning.

- Futures trade as high as 92.43, piercing the first couple of layers of resistance.

- Bulls now look to the November 18 high (92.60) and the 20-day EMA (92.74), with a break above the latter needed to cancel the recent bearish move.

- Yields 4-7bp lower, with the curve flattening accelerating after the move higher in 2s10s stalled at 80bp earlier this week.

- The soft PMIs drove outperformance vs. Bunds, with the 10-Year spread moving to 185bp after a failure above 190bp in recent sessions.

- Elsewhere, retail sales & PSNB data was disappointing, but had little impact at the open.

- BoE-dated OIS 0.5-3.0bp more dovish on the day, showing nearly 22bp of easing for December, 29.5bp through February, 38.5bp for March and 48.5bp through April.

- SONIA futures flat to +5.5. Implied terminal rate at ~3.35%.

- Comments from BoE’s Pill are due later (15:40 London). Don’t expect much market movement as he already spoke earlier in the week. He has already noted that he doesn’t think that his view (he voted for no change in rates) has shifted much since this month’s meeting.

- A reminder that we do not expect much market vol. to stem from any non-Bailey BoE comments in the lead up to the December decision, given the entrenched views of the other MPC members (Bailey is deemed the key swing voter).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.752 | -21.7 |

Feb-26 | 3.674 | -29.5 |

Mar-26 | 3.585 | -38.5 |

Apr-26 | 3.484 | -48.5 |

Jun-26 | 3.438 | -53.2 |

Jul-26 | 3.379 | -59.0 |

Sep-26 | 1.000 | -296.9 |

EQUITIES: Eurostoxx 50 Futures Below Key Support at 50-Day EMA

A medium-term bull trend in Eurostoxx 50 futures remains intact, however, the past week’s sell-off highlights a stronger corrective cycle. The contract has breached two key support points; 5600.89, the 50-day EMA, and 5621.00, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5427.01, a Fibonacci retracement. Initial firm resistance to watch is 5645.61, the 20-day EMA. S&P E-Minis remain in a short-term bear-mode condition and a steep sell-off yesterday reinforces current conditions. The breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the corrective cycle. Sights are on 6540.25 (pierced), the Oct 10 low and a key support. A break would open 6476.62, a Fibonacci retracement point. Initial firm resistance to watch is 6747.78, the 20-day EMA.

- Japan's NIKKEI closed lower by 1198.06 pts or -2.4% at 48625.88 and the TOPIX ended 1.84 pts lower or -0.06% at 3297.73.

- Elsewhere, in China the SHANGHAI closed lower by 96.16 pts or -2.45% at 3834.891 and the HANG SENG ended 615.55 pts lower or -2.38% at 25220.02.

- Across Europe, Germany's DAX trades lower by 244.09 pts or -1.05% at 23033.99, FTSE 100 lower by 53.09 pts or -0.56% at 9474.53, CAC 40 down 53.12 pts or -0.67% at 7927.95 and Euro Stoxx 50 down 70.82 pts or -1.27% at 5499.1.

- Dow Jones mini up 147 pts or +0.32% at 45973, S&P 500 mini up 1.75 pts or +0.03% at 6559.5, NASDAQ mini down 48 pts or -0.2% at 24085.5.

Time: 10:00 GMT

COMMODITIES: Move Down in WTI Futures This Week Strengthens a Bearish Theme

The move down this week in WTI futures strengthens a bearish theme. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction. The bearish phase in Gold between Oct 20 and 28 appears to have been a correction and has allowed a recent overbought condition to unwind. The recovery since Oct 28 does suggest the correction is over. Key support to watch lies at the 50-day EMA, at $3948.2. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude down $1.13 or -1.92% at $57.85

- Natural Gas up $0.08 or +1.74% at $4.551

- Gold spot down $26.19 or -0.64% at $4049.93

- Copper down $2.9 or -0.57% at $502.15

- Silver down $1.46 or -2.88% at $49.1803

- Platinum down $16.1 or -1.06% at $1501.56

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1400/0900 | Boston Fed's Susan Collins | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 22/11/2025 | 0800/0900 | ECB Lagarde in Roundtable at Austrian National Bank | ||

| 22/11/2025 | 1100/1200 | ECB Lagarde Keynote on Fiscal and MonPol |