FOREX: USD Supported by Risk Off Sentiment, JPY Outperforming

Nov-21 10:34

- An extension of equity weakness early Friday is providing support to the US dollar, as the DXY edges higher towards the recovery highs at 100.36. Ongoing concerns relating to AI valuations continue to permeate global markets, and waning sentiment across crypto markets and pressure on precious metals appear to finally be providing headwinds for Cross/JPY and pressuring the EM FX basket.

- JPY is the outperformer this morning, leading USDJPY to reverse around 120 pips from yesterday’s 157.89 cycle high. Overnight inline Japanese core CPI print likely did not move the needle for the December BoJ decision as opposed to recent price action in the yen. Some profit taking dynamics may be at play heading into the weekend, and there is the potential for verbal jawboning from Japanese authorities to pick up next week.

- This week’s rally fell short of the year’s highs at 158.87, however, it is worth noting the pair has entered overbought territory, and the latest dip is seen as corrective. The prior breakout at 155 now provides initial support.

- The most notable implication of this morning's Flash PMIs perhaps were parts of the UK press release which should facilitate BoE Governor Bailey's confidence to cut in December. GBPUSD has seen some downside in recent trade, hovering just above 1.3050, and a reversal through 1.3010, the Nov 4 / 5 low, would confirm a resumption of the downtrend. Focus for GBP is on Wednesday's UK budget.

- Michigan consumer sentiment and inflation expectations alongside US wholesale sales and Canada retail sales are on the data calendar for today. A set of speakers from the ECB, the BoE, the SNB and Fed are scheduled to appear.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

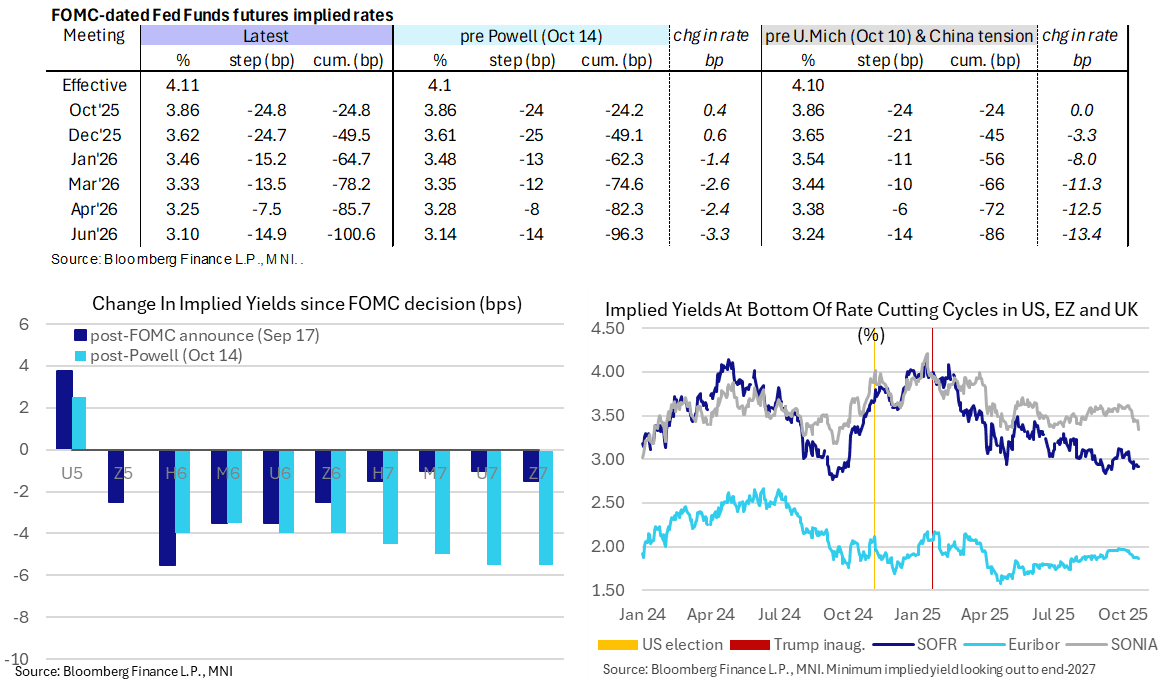

STIR: Back-to-Back Fed 25bp Cuts Still Eyed, Only Mild Impact From Soft UK CPI

Oct-22 10:27

- Fed Funds implied rates are little changed overnight, with back-to-back cuts seen for next week and December meetings before a quarterly pace thereafter to mid-2026.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49.5bp Dec, 64.5bp Jan, 78bp Mar, 85.5bp Apr and 100.5bp Jun.

- SOFR futures are little changed on the day, with only small intraday spillover from a sizeable rally in UK rates on softer than expected UK CPI inflation.

- The SOFR implied terminal yield of 2.915% (SFRH7) is unchanged on the day, close to last week’s lowest close of 2.89% in risk-off moves on regional bank fears. For context, cycle lows were 2.77% back in Sep 2024 in anticipation of an aggressive start to the Fed’s easing cycle at the time.

- It’s a particularly thin data docket today, with just MBA mortgage applications. More notable releases for the week are state-level jobless claims to be released from Thursday afternoon and then the highlight being the delayed September CPI report on Friday.

LOOK AHEAD: Wednesday Data Calendar: 20Y Bond Re-Open

Oct-22 10:26

- US Data/Speaker Calendar (prior, estimate)

- 10/22 0700 MBA Mortgage Applications (-1.8%, --)

- 10/22 1130 US Tsy $69B 17W bill auction

- 10/22 1300 US Tsy $13B 20Y Bond re-open (91210UN6)

- 10/22 1600 Pres Trump meets w/ Secretary General of NATO (closed Press)

- Source: Bloomberg Finance L.P. / MNI

US 10YR FUTURE TECHS: (Z5) Bull Cycle Intact

Oct-22 10:26

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-24 @ 11:15 BST Oct 22

- SUP 1: 113-03+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-22 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

Bullish conditions in Treasuries remain intact. The recent breach of key resistance at 113-29, the Sep 11 high, confirms a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 11303+, the 20-day EMA.