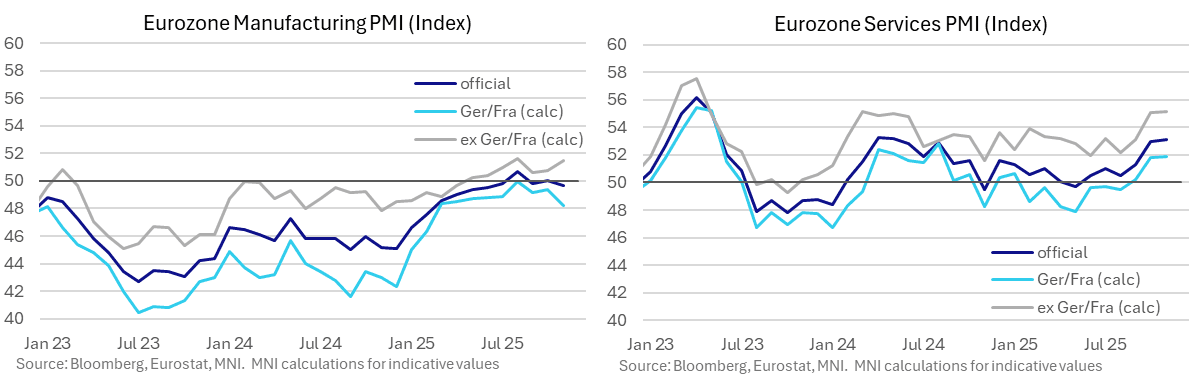

EUROZONE DATA: Nov Flash PMIs: EZ ex-Germany and France Still Outperforming

The Eurozone-wide composite PMI has now been expansionary for eleven consecutive months. The 52.4 November reading was essentially in line with consensus and October’s 52.5, with a weaker-than-expected manufacturing print offset by stronger services.

There's been little net reaction in EUR STIRs to the data, with OIS still pricing 10bps of easing through year-end. The combination of output/new order growth and easing output charge inflation will be considered an ideal combination for the ECB.

The Eurozone ex-Germany/France continues to stand out as an outperformer. We estimate the ex-Germany/France manufacturing PMI at 51.5 (vs 50.8 prior) and the Germany/France reading at 48.2 (vs 49.4 prior). Meanwhile, we see the ex-Germany/France services PMI at 55.2 (vs 55.0 prior), with Germany/France at 51.9 (vs 51.8 prior).

Key notes from the Eurozone-wide release:

- "Germany continued to record growth of output in November, albeit with the pace of expansion easing from October. Meanwhile, France saw a near-stabilisation of business activity, helped by a return to growth in the service sector. The best performance in November, however, was seen in the rest of the eurozone, where output rose solidly, and at the fastest pace since April 2023."

- "New orders rose for a fourth consecutive month, however, as an expansion in services outweighed a renewed fall in manufacturing. The ability of firms to secure new business continued to be hampered by weakness in international demand. New export orders (which include intra-eurozone trade) decreased slightly again in November, and at the same pace as seen in October".

- "After rising in October, staffing levels were unchanged in November. A slower, and only slight increase in services

employment was registered, and this was cancelled out by a faster fall in manufacturing workforce numbers. ...Staffing levels decreased slightly in both Germany and France, but continued to increase across the rest of the eurozone." - Despite a "sharp" increase in input costs, "the pace of output price inflation eased in November, slowing to the weakest in just over a year". The report notes that "charges increased in Germany and across the eurozone excluding the largest two economies, while French firms kept their selling prices unchanged.".

- "Sentiment improved across Germany, France and the rest of the eurozone, the latter of which saw optimism hit a nine-month high."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Outright 10yr Call seller

TYZ5 114c, sold at '35 in 2.4k.

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 1.47bn at 1.1595/1.1600.

NZDUSD 1.15bn at 0.5700.

EURUSD 1.26bn at 1.1575 (thu).

AUDUSD 1.6bn at 0.6450 (fri).

AUDUSD 1.79bn at 0.6490 (mon).

- EURUSD: 1.1595 (631mln), 1.1600 (839mln), 1.1620 (354mln), 1.1625 (425mln), 1.1700 (449mln).

- EURGBP: 0.8740 (498mln).

- USDJPY: 151.00 (944mln), 152.00 (1.26bn).

- AUDUSD: 0.6535 (516mln).

- NZDUSD: 0.5700 (1.15bn).

GERMAN AUCTION PREVIEW: 2.50% Nov-32 Bund

This morning, Germany will reopen its on-the-run 7-year 2.50% Nov-32 Bund (ISIN: DE000BU27014) for the second and final time this year.

- The launch auction of the line on August 27 was very soft with only E3.170bln of bids received for the intended E4.0bln transaction. However, ahead of the first reopening came the release of the Q4 issuance plan in which it was announced today's auction would be the sole auction of the quarter for the 7-year Bund with a smaller E3bln size. That probably helped the first re-open of the line fare a little better, with a 1.48x bid-to-cover / 1.13x bid-to-offer combination and the lowest accepted price at the auction coming in above the secondary market mid-prices.

- Domestically in Germany, Finance Minister Klingbeil is scheduled to update the government's tax projections tomorrow, with current revenues likely running a little ahead of the previous plan. For detailed considerations see our post at 08:19 BST.

- The next German auction will be E4bln of the 2.20% Oct-30 Bobl (ISIN: DE000BU25059) on October 28.

- Timing: Results will be available shortly after the bidding window closes at 10:30BST / 11:30CEST.