MNI US OPEN - Clarity in US CPI Report May Prove Elusive

EXECUTIVE SUMMARY

- MNI US CPI PREVIEW: CLARITY MAY AGAIN PROVE ELUSIVE

- MIRAN SAYS FED IS BIGGEST RISK TO U.S. GROWTH

- TRUMP TRADE TEAM WORKING TO NARROW SCOPE OF METALS TARIFFS: BBG

- PARTIAL GOVERNMENT SHUTDOWN LOOMS AS CONGRESS LEAVES TOWN WITHOUT A DEAL

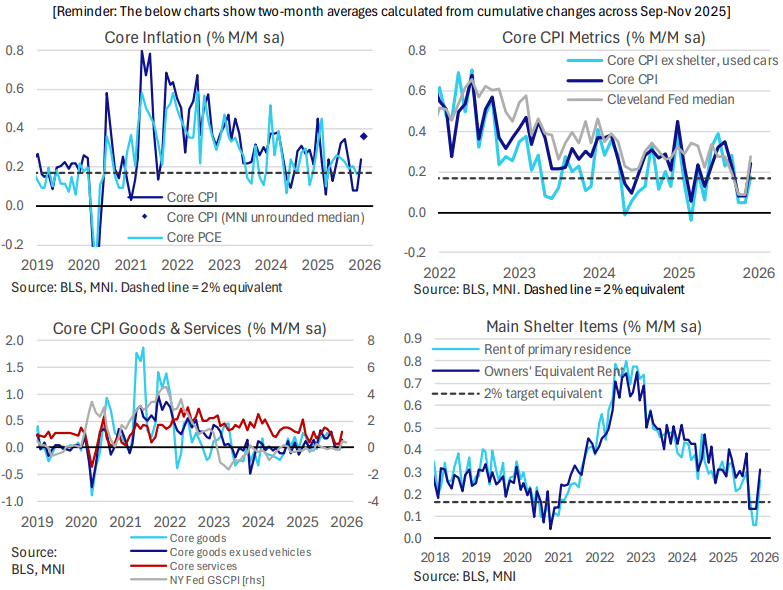

Figure 1: Recent US inflation developments

NEWS

MNI US CPI PREVIEW: Clarity May Again Prove Elusive

Consensus looks for an acceleration in core CPI following recent soft prints, helped by typical start‑of‑year price resets and the ongoing normalization from the shutdown‑distorted Oct/Nov data. Core is seen rising to 0.36% M/M after December’s 0.24% (based on unrounded estimates), with headline 0.29% after 0.31%. Several technical factors mean any acceleration should be interpreted with caution. January is prone to residual seasonality effects and this report brings new relative‑importance CPI weights, both of which may subtly reshape monthly dynamics and make it difficult to make a clean read.

FED (MNI): Miran Says Fed Is Biggest Risk to U.S. Growth

Federal Reserve Governor Stephen Miran said Thursday the biggest risk to growth in the United States is the Fed and interest rates need to be lower, additionally because there is a role for the central bank to help reduce pockets of slack that remain in the labor market. "I think it's us," Miran said in Q&A at a Dallas Fed event, when asked about the biggest risk to growth. "The biggest risk I think to the economy is that we're misconstruing just how tight monetary policy is." Miran also said there are some remaining signs of slack in the labor market, with people working part time for economic reasons, longer time spent on unemployment, and some who are marginally attached to the labor force.

US (BBG): Trump Trade Team Working to Narrow Scope of Metals Tariffs

The Trump administration is working to narrow its broad tariffs on steel and aluminum products that companies find difficult to calculate and the European Union wants reined in as part of its pending trade deal with the US, a person familiar with the matter said. The US Trade Representative’s Office is scrambling to resolve complications spawned last year by the Commerce Department’s efforts to rush out President Donald Trump’s tariff agenda, the person said. The White House has communicated to companies that adjustments are in the works, but details and timing remain unclear, the person said.

US (WaPo): Partial Government Shutdown Looms as Congress Leaves Town Without a Deal

Large swaths of the Department of Homeland Security are set to shut down Saturday after Senate Democrats on Thursday blocked two funding bills because the legislation did not include new restrictions on federal immigration agents. Democrats demanded a long list of changes to DHS after federal immigration agents killed Alex Pretti last month in Minneapolis, including tighter rules on warrants and a ban on agents wearing face masks. President Donald Trump appeared open to some of them, but Democrats rejected a proposal the White House made Wednesday night, all but ensuring a partial government shutdown.

US/JAPAN (BBG): Japan, US Far Apart on $550 Billion Fund Projects, Akazawa Says

The US and Japan remain far apart over which projects should be funded first under the framework of a $550 billion investment vehicle even as the two sides made progress in their latest round of talks, Japanese Trade Minister Ryosei Akazawa said. Akazawa met for 85 minutes with US Commerce Secretary Howard Lutnick on Thursday in Washington to discuss establishing the initial projects. He didn’t announce any projects or elaborate on the details of the private discussion. “It is premature to say what exactly we will be able to introduce to everyone as the first batch,” Akazawa said to reporters in Washington. “I have stated that despite the tremendous efforts made by staff, a significant gap remains.”

US/MIDEAST (NYT): U.S. Aircraft Carrier Will Be Sent to the Middle East From Venezuela, Officials Say

The aircraft carrier U.S.S. Gerald R. Ford and its escort ships deployed to the Caribbean will be sent to the Middle East and are not expected to return to their home ports until late April or early May. The ship’s crew was informed of the decision on Thursday, according to four U.S. officials who spoke on the condition of anonymity because they were not authorized to speak publicly about the decision. The Ford strike group’s new orders will have it joining the U.S.S. Abraham Lincoln carrier strike group in the Persian Gulf as part of President Trump’s resurgent pressure campaign against Iran’s leaders.

RUSSIA/UKRAINE (MNI): Kremlin Confirms New Russia-US-Ukraine Talks Next Week

State-run Tass reports comments from Kremlin spox Dmitry Peskov. Says that a new round of peace talks on Ukraine will take place next week. On 12 Feb, Ukrainian President Volodymyr Zelenskyy had raised the prospect of tripartite talks between the US, Ukraine, and Russia taking place in the US on 17 or 18 Feb, but said it was unclear if Russia would accept. Peskov said, "There's an agreement that it will indeed take place next week. We'll let you know the location and exact dates. But it will indeed be next week,"

GLOBAL (MNI): Key Speakers on First Day of Munich Security Conference

The Munich Security Conference is underway at the Hotel Bayerischer Hof in the Bavarian capital. We outline the key political speakers on day one of the event, with timings and livestreams, in the link above. German Chancellor Friedrich Merz, French President Emmanuel Macron and Japanese Defence Minister Shinjir Koizumi are among the speakers today.

ECB (BBG): ECB Has Yet to See Full Impact of Euro Appreciation, Kazaks Says

The European Central Bank is still waiting to see how severely the economy will be affected by the ascent of the euro that started in 2025, according to Governing Council member Martins Kazaks. With estimates suggesting that it takes approximately 12 months for currency shifts to trickle through, “we will likely see the full impact of the euro’s strengthening last year toward late spring,” Kazaks said in an interview in Riga.

UK (FT): Nigel Farage’s Popularity Dips as Reform UK Surges in Polls

Nigel Farage’s popularity has dipped in recent months even as Reform UK has surged ahead of Labour and the Conservatives in opinion polls, signalling challenges ahead as he seeks to convince voters his insurgent party is fit to govern. Sixty-four per cent of the UK public view the Reform UK leader unfavourably, up from 59 per cent in June 2025, according to new favourability ratings published by polling company YouGov. Some 27 per cent approve of Farage, down from a peak of 32 per cent in May and August last year. The same data, published on Thursday, suggested Sir Keir Starmer had enjoyed a slight uptick in public support over the past month, but his popularity has plummeted since he took office in July 2024 and he remains deeply unpopular.

UK (FT): Keir Starmer Set to Call for Multinational Defence Initiative to Cut Rearmament Costs

Sir Keir Starmer is set to make the case for the UK and its western allies to forge a multinational defence initiative that could oversee joint weapons procurement and drive down the costs of rearmament. The British prime minister is expected to raise the idea at the Munich Security Conference this weekend, according to UK government officials. He is poised to call for closer defence co-operation with allies in a speech on Saturday, as well as in private discussions with other leaders at the three-day event.

BOJ (MNI): BOJ's Tamura See Higher Rate; No Timeframe

The Bank of Japan will continue raising policy interest rates to adjust the degree of monetary easing, said Board Member Naoki Tamura Friday, without committing to a specific timeframe. “As for the future conduct of monetary policy, given that real interest rates are at significantly low levels, if the outlook for economic activity and prices presented in the January Outlook Report is realised, the Bank, in accordance with improvement in economic activity and prices, will continue to raise the policy interest rate and adjust the degree of monetary accommodation,” Tamura, the BOJ’s most hawkish member, told business leaders in Yokohama.

BOJ (RTRS): Japan PM Adviser Plays Down Need for Reflationists to Fill BOJ Board

Japan's government does not necessarily need to pick reflationists to fill seats opening up in the central bank board as the economy has exited deflation, Etsuro Honda, an economic adviser to premier Sanae Takaichi, told Reuters. The Bank of Japan may see scope to raise interest rates this year as rising inflation and bond yields suggest the economy is normalising, said Honda, who was also an economic aide of former Prime Minister Shinzo Abe.

JAPAN/CHINA (BBG): Japan Seizes Chinese Fishing Boat, Adding to Strained Ties

Japan said it seized a Chinese fishing vessel and arrested its captain after the ship entered the nation’s exclusive economic zone and sought to avoid inspection, adding a fresh complication to strained ties between the two Asian giants. The captain was arrested around 12:23 p.m. on Thursday after the vessel entered Japan’s EEZ off the coast of Nagasaki prefecture and tried to flee to avoid questioning, Japan’s Fisheries Agency said in a statement. The seizure was the first of a Chinese fishing vessel since 2022, the agency said.

CHINA (BBG): PBOC’s Rising Focus on Overnight Rate Spurs Talk of Policy Shift

The Chinese central bank’s heightened focus on the overnight money market rate is fueling speculation that it may eventually move toward adopting this tenor as its primary policy target. The People’s Bank of China re-ordered its monthly report published late Wednesday by moving money market conditions to the first section before bonds, a structure unseen in at least two decades. It also added an analysis of the interest-rate levels of pledged bond repurchases, highlighting the comparison of the overnight repo cost to its seven-day reverse repo rate.

CHINA (MNI EXCLUSIVE): China PPI to Turn Positive in Q3 - Analysts

Local analysts provide insight into China's PPI this year. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI EXCLUSIVE): China’s Fixed-Asset Investment to Stabilise in 2026

Advisors share their outlook on China's fixed-asset investment. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBNZ (MNI EXCLUSIVE): RBNZ to Hold, Hikes Not Likely Until H2 - Former Officials

Former RBNZ officials share their OCR outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

EUROZONE FLASH Q4 GDP 1.3% Y/Y (1.3% PRELIM FLASH) (MNI)

EUROZONE FLASH Q4 GDP 0.3% Q/Q (0.3% PRELIM FLASH) (MNI)

SPAIN DATA (MNI): HICP Revised 0.1ppt Lower vs Flash, Core CPI Unrevised

- SPAIN JAN FINAL HICP 2.4% Y/Y (2.5% FLASH, 3.0% DEC)

- SPAIN JAN FINAL HICP -0.8% M/M (-0.7% FLASH, 0.3% DEC)

Spain final Jan HICP printed at 2.42% Y/Y, 0.1ppt lower than the flash reading when rounded (vs 3.0% Dec). The M/M rate was also revised down 0.1ppt on a rounded basis to -0.8% M/M (vs 0.3% Dec) but unrounded was -0.75%. Core HICP (ex unprocessed foods and energy - not the Eurostat definition) was 2.77% Y/Y (flash was also 2.8% Y/Y). Headline CPI (non-HICP) was also revised a tenth lower than flash at 2.3% Y/Y (vs 2.9% Dec), while core CPI was unrevised at 2.6% Y/Y.

SWITZERLAND DATA (MNI): Swiss January CPI Won’t Move the Needle for SNB

- SWISS JAN CPI -0.1% M/M, 0.1% Y/Y (0.0% M/M, 0.1% Y/Y DEC)

- SWISS JAN CORE CPI 0.5% Y/Y (0.5% DEC)

Swiss CPI inflation printed in line consensus on the yearly measure at 0.1% in January (vs 0.1% cons and prior), and -0.058% M/M (0.0% cons). Core CPI was also in line with consensus, at 0.5% Y/Y (vs 0.5% cons and prior). This means Q1 inflation starts off in line with the SNB forecast, confirming that the most probable path for SNB policy ahead is a hold for the foreseeable future. Despite this, a more material undershoot with repeated readings below 0% would likely be needed for the SNB to cut into negative territory.

CHINA DATA (MNI): China Jan M2 Rises to Over Two-Year High

- CHINA JAN NEW LOANS CNY4.71 TRLN VS MEDIAN CNY5 TRLN

- CHINA END-JAN M2 +9.0% Y/Y VS MEDIAN +8.3%; END-DEC +8.5% Y/Y

- CHINA END-JAN M1 +4.9% Y/Y VS +3.8% Y/Y END-DEC

- CHINA END-JAN M0 +2.7% Y/Y VS +10.2% Y/Y END-DEC

- CHINA JAN TSF CNY7.22 TRLN VS MEDIAN CNY7.09 TRLN

MNI (Beijing) China's M2 money supply grew by 9.0% y/y in January, he highest growth rate since December 2023, beating both forecasts of 8.3% growth and December's 8.5% gain, data released on Friday by the People's Bank of China showed. New yuan loans increased for the third month running, up by CNY4.71 trillion in January, surging from the previous CNY910 billion and hitting a one-year high. Total social financing rose by CNY7.22 trillion, up from CNY2.21 trillion in December, setting a new high. While M1 rose by 4.9% y/y, accelerating from December's 3.8% growth. M0 grew by 2.7% y/y, down from the previous 10.2% reading.

NEW ZEALAND DATA (MNI): Inflation Expectations Edge Up But From Low Levels

New Zealand 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This is highs back to Q1 2024 for the print, but the trend rise has been very modest over this period. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%. The data point to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term (the RBNZ meets next Wed, Feb 18).

RATINGS: Austria’s Negative Outlook at Moody’s Set for Review After Close

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Moody’s on Austria (current rating: Aa1; Outlook Negative), Estonia (current rating: A1; Outlook Stable), Luxembourg (current rating: Aaa; Outlook Stable), the Netherlands (current rating: Aaa; Outlook Stable) & Switzerland (current rating: Aaa; Outlook Stable)

- Morningstar DBRS on Latvia (current rating: A, Stable Trend)

Please use this link to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings). Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

FOREX: DXY Consolidates Ahead of US CPI

- FX markets await US CPI later today with major pairs consolidating recent ranges. More attention may be on equities after yesterday's sharp selloff which also filtered through to precious metals, and slightly extended overnight.

- JPY underperforms moderately on the session after PM Takaichi's advisor Honda stated there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. This keeps USDJPY set to close the week sharply lower with a 2.2% loss since last Friday at typing.

- With next week's inauguration of PM Takaichi incoming, a major focus point for JPY will be on any additional intel on financing of the food tax suspension, with higher usage of FX account proceeds likely not sufficient to cover the funding gap. From a technical standpoint, a bearish tone in USDJPY remains intact, with key short-term support at 152.10, the Jan 27 low and bear trigger, in close range with trendline support at 151.78. Initial resistance to watch is at 155.62, the 20-day EMA.

- Weaker risk sentiment pressured AUDUSD after the pair came within 11 pips of the 0.7158 2023 highs yesterday. AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are in scope. Clearance of the 2023 highs would put attention on 0.7208, a Fibonacci projection.

- In an otherwise light data calendar, US CPI is a key test of whether tariff-related pressures, early‑year price adjustments, and lingering category‑specific normalization are beginning to exert more persistent influence—an issue several FOMC participants have highlighted as central to judging the underlying inflation trajectory.

- BoE's Pill, ECB's Guindos and BoJ's Tamura are scheduled to speak. For Pill, we will be watching for any indication on the neutral rate in his comments today.

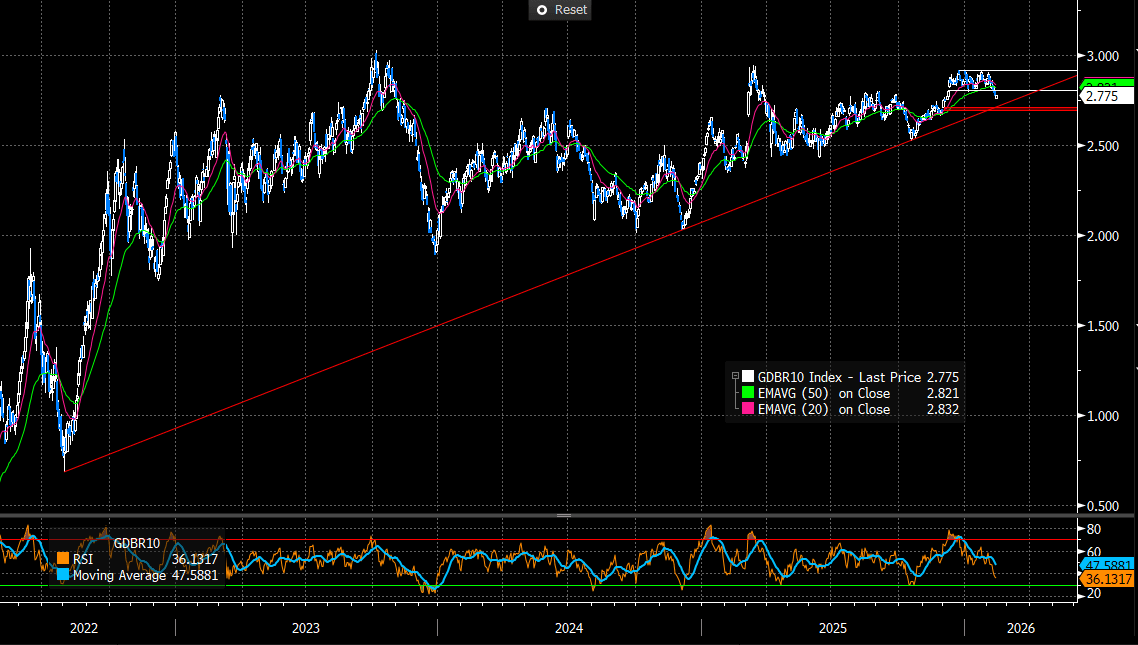

EGBS: 10-Year Bund Yields Trying to Consolidate Below 2.80%

German yields are marginally lower this morning, with the 10-year yield notably trying to consolidate below the 2.80% figure. The next downside levels to watch are 2.75% and 2.70% - the latter closely aligning with trendline support (see chart). Despite well-documented domestic fiscal/issuance pressures, Bunds remain a popular safe haven /diversifier, which is countering upward yield moves for now. The median analyst still expects Bund yields to drift up towards 3% through the course of this year.

- Bund futures are –7 ticks at 128.94, after registering a multi-week high of 129.12 this morning. A bull mode in Bund futures remains intact recent technical breaks signal scope for an extension towards 129.55, the Nov 26 ‘25 high and the next key resistance point.

- 10-year EGB spreads to Bunds widened into yesterday’s close amid the broad-based souring of risk sentiment, but have stabilised a little this morning. The 10-year BTP/Bund spread is currently at 60.6bps.

- The second reading of Eurozone Q4 GDP was in line with the flash at 0.3% Q/Q. Meanwhile, employment growth of 0.2% Q/Q confirmed the ECB’s December projections. Spanish January HICP was revised down a tenth on a rounded basis to 2.4% Y/Y.

- Global focus remains on today’s US CPI report at 1330GMT. Meanwhile, Moody’s reviews Austria’s sovereign rating after hours (current rating: Aa1; Outlook Negative).

Figure 2: 10-year Bund yields

Source: Bloomberg Finance L.P

GILTS: Off Highs, Recovery Intact

Gilts have faded from opening highs, with wider core global FI peers also off best levels, while global equity benchmarks and crude oil futures are off session lows.

- Futures pierced yesterday’s high, topping out at 91.51, before fading back to trade -9 at 91.33.

- This week’s gains in the contract have resulted in a break of the 50-day EMA, highlighting a stronger reversal, while signalling scope for an extension towards a Fibonacci retracement point (91.73). Our technical analyst warns that it is still possible that the recovery is a correction. Initial firm support to watch lies at the Feb 11 low (90.62).

- Yields are essentially flat to ~1bp higher across the curve, light steepening seen.

- 2s have registered another fresh cycle low at 3.588%, next downside level of note located at the August 14 low (3.531%)

- 10s registered the lowest close of the month yesterday, last ~4.46%. The January 22 low (4.413%%) presents the next downside level of note.

- BoE-dated OIS little changed, showing 17bp of easing for next month, 23bp through April, 32bp through June and 46bp through November.

- BoE chief economist Pill will participate in a fireside chat at a Santander macroeconomic event later today (12:00 London).

- A reminder that Pill sits at the hawkish end of the BoE spectrum and did not vote for a cut at last week’s meeting (5-4 split in favour of leaving rates on hold). We don’t seem him as one of the major swing voters.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.554 | -17.3 |

Apr-26 | 3.495 | -23.2 |

Jun-26 | 3.410 | -31.8 |

Jul-26 | 3.343 | -38.4 |

Sep-26 | 3.309 | -41.8 |

Nov-26 | 3.271 | -45.7 |

Dec-26 | 3.270 | -45.7 |

EQUITIES: Recent Sharp Sell-Off for E-Mini S&P Reinstates Bearish Threat

The medium-term trend condition in EuroStoxx 50 futures remains bullish and this week’s fresh cycle highs reinforce the bull theme. The initial move higher yesterday delivered a print above the 6100.00 handle. A clear breach of this hurdle would open 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5901.38. Clearance of this average would highlight a short-term top. For now, a move down is considered corrective. A sharp sell-off yesterday in S&P E-Minis reinstates a potential bearish threat with key resistance at 7043.00 intact, the Jan 28 high and bull trigger. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6922.20, the 50-day EMA.

- Japan's NIKKEI closed lower by 697.87 pts or -1.21% at 56941.97 and the TOPIX ended 63.31 pts lower or -1.63% at 3818.85.

- Elsewhere, in China the SHANGHAI closed lower by 51.945 pts or -1.26% at 4082.073 and the HANG SENG ended 465.42 pts lower or -1.72% at 26567.12.

- Across Europe, Germany's DAX trades lower by 21.88 pts or -0.09% at 24827.16, FTSE 100 higher by 23.97 pts or +0.23% at 10425.45, CAC 40 down 17.01 pts or -0.2% at 8322.76 and Euro Stoxx 50 down 10.4 pts or -0.17% at 5999.89.

- Dow Jones mini down 92 pts or -0.19% at 49433, S&P 500 mini down 2 pts or -0.03% at 6848.75, NASDAQ mini up 14.25 pts or +0.06% at 24781.25.

Time: 10:15 GMT (05:15 ET)

COMMODITIES: WTI Futures Test 20-Day EMA Support

A bull cycle in WTI futures remains intact. However, the move lower from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.58 (pierced). The 50-day EMA lies at $60.87. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend. Recent gains in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high still highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude up $0.2 or +0.32% at $63.05

- Natural Gas down $0.07 or -2.02% at $3.152

- Gold spot up $52.38 or +1.06% at $4973.68

- Copper down $3.35 or -0.58% at $575.2

- Silver up $3.1 or +4.12% at $78.3844

- Platinum up $35.55 or +1.77% at $2040.64

Time: 10:15 GMT (05:15 ET)

| Date | GMT/Local | Impact | Country | Event |

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event | ||

| 13/02/2026 | - | BOE MPG Minutes Released | ||

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | ** | US CPI Annual Revised | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/02/2026 | 1630/1730 | ECB Lagarde Roundtable on Trade Dependencies and Global Supply Chains | ||

| 15/02/2026 | 0930/1030 | ECB Lagarde Panel on European Competitiveness |