MNI RBNZ WATCH: MPC To Hold, Eye Iran Impacts

The Reserve Bank of New Zealand is likely to leave the Official Cash Rate at 2.25% at next Wednesday’s meeting, looking through the initial impact of the Iran conflict while remaining alert to second-round inflation pressures later in the year.

Governor Anna Breman has signalled a standard central bank response to an oil shock, indicating policy is well placed to manage global volatility and its impact on inflation. Recent remarks by Breman and Chief Economist Paul Conway have also pushed back against tightening financial conditions, suggesting rate hikes are not imminent, a message likely to be reinforced during next week's press conference following the decision.

Market pricing has adjusted accordingly, with little expectation of a move next week, though traders still see at least one hike by September and the OCR rising to around 2.85% by year-end.

However, New Zealand – like Australia – remains exposed to a prolonged energy shock, making next week’s communication key to understanding how the MPC assesses inflation risks and the potential for stagnation. (See MNI: Energy Shock, Stagflation Risks Cloud RBNZ Policy Path)

The MPC has held the rate steady since its last 25 basis point cut in October 2025. (See MNI RBNZ WATCH: Breman Notes Dec Hike Risk, Weak House Prices)

INFLATION EXPECTATIONS

Breman has emphasised vigilance against a near-term inflation spike becoming entrenched, as headline inflation was already above 3% and expected to rise further leading into the supply shock, while core measures also remain elevated.

Even so, the Bank is likely to reassert its confidence that increasing spare capacity and weak domestic demand will help drive inflation back to the 1-3% target band. Policymakers will focus on whether price-setting behaviour remains consistent with the target, placing greater weight on longer-term expectations, which are expected to remain anchored near 2%.

DATA AND OUTLOOK

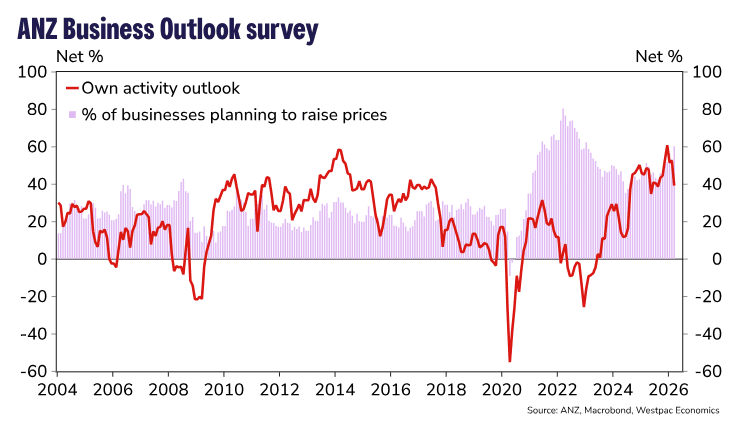

However, price risks are tilted to the upside. A sustained inflation shock could shift pricing behaviour and wage dynamics. Recent data point to a fragile recovery, driving fears of future stagflation among former RBNZ economists, concerned that a failure to contain expectations could ultimately require a more aggressive policy response. Business confidence fell 26.7% in March and will more than likely continue to fall in April. (See chart)

GDP growth also remains soft, with Q4 expanding just 0.2% quarter-on-quarter, underscoring weak private demand. The outlook for 2026 has deteriorated, with higher fuel costs acting as a drag on consumption and downside risks to growth intensifying.

If demand remains subdued and external conditions deteriorate, policymakers may be forced to balance rising inflation pressures against a fragile economic backdrop.