MNI RBNZ WATCH: Breman Notes Dec Hike Risk, Weak House Prices

Reserve Bank of New Zealand Governor Anna Breman sees the possibility of an end-of-year hike in the Official Cash Rate from its current 2.25% but acknowledged that economic recovery remains in its early stages, with policymakers closely watching how weak house price growth will feed through to household consumption.

“I think that currently our best forecast is the OCR track, and that indicates that there is a possibility of a rate hike before the end of the year,” Breman told reporters following the Monetary Policy Committee’s largely-expected decision to hold rates steady, adding that the Bank had not fully priced in such an outcome. (See MNI RBNZ WATCH: Cautious Hold On Moderate Economic Recovery)

Incoming data pointed to a recovery in its early stages, but one which is uneven and likely not felt by most households, she noted. "They're still feeling the high inflation that we had over the past few years. Many businesses are still struggling.”

Breman, delivering her first OCR decision since taking on the governorship, stressed the Bank was not planning to tighten policy until stronger inflation pressures and activity data emerge. “We want to keep the OCR on hold to support the recovery while ensuring that inflation falls back to target," she continued.

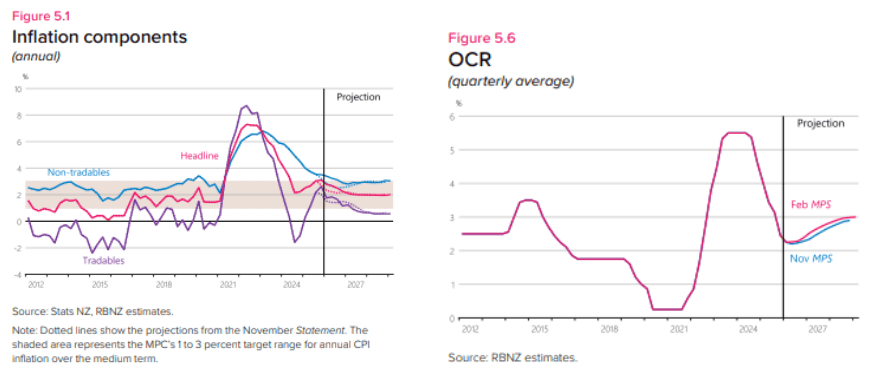

The market read Breman’s comments and the latest Hidden PDF – which showed a slightly firmer OCR projection but a lower CPI outlook – as mildly dovish, with overnight index swaps softening around eight basis points to roughly 31bp of tightening priced by year-end. (See charts)

The Bank has held the OCR at 2.25% since its last 25bp cut in October, with 300bp of cumulative easing since the rate peaked in May 2023. (See MNI RBNZ WATCH: Easing Bias Maintained, But 2026 Hold Likely)

LABOUR, HOUSING & CONSUMPTION

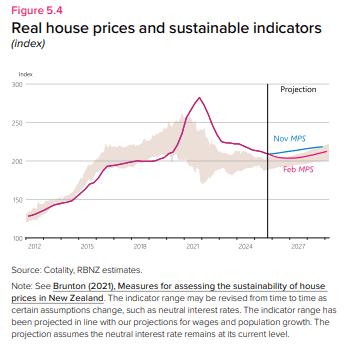

Driving the Bank’s caution is a subdued housing market and its implications for spending. Chief Economist Paul Conway said slower house price growth represents a structural shift for the economy, which has historically relied on housing wealth to drive demand. House prices remain slightly above levels the Bank considers sustainable, underpinning expectations that housing inflation will stay subdued over the coming year.

“That’s a big change for the New Zealand economy, and that's why we're highlighting the downside risk to consumption,” Conway said, noting household spending is likely to become more dependent on labour market conditions rather than housing gains.

Conway added that lower interest rates are already helping broaden the recovery across sectors. “We're seeing growth broadening out of the ag sector, regional New Zealand, into metropolitan centres and manufacturing. Construction is starting to pick up because of lower interest rates.” He noted, however, that the shift away from housing-led demand creates downside risks. “Consumption is a huge part of the economy, and we do need households to stop being as cautious if the recovery is to continue to broaden.”

MORE TRANSPARENCY, MEETINGS

Breman said the Bank plans to increase transparency around policy deliberations and expand its meeting schedule to eight in 2027, following the introduction of monthly CPI data.

The recent statement reflected differing views on OCR timing but she said consensus decision-making remains the goal. Breman added policymakers will also step up outreach, with speeches and regional visits aimed at both explaining decisions and gathering feedback from businesses and households on economic conditions.