MNI RBNZ WATCH: Cautious Hold On Moderate Economic Recovery

The Reserve Bank of New Zealand is expected to leave the Official Cash Rate at 2.25% when it meets next Wednesday, while maintaining a cautious tone as the economy recovers only moderately and core inflation pressures remain largely contained.

The Monetary Policy Committee cut the OCR 25 basis points in December, after a 50-basis-point reduction in October, bringing cumulative easing since August 2024 to 300 basis points. (See MNI RBNZ WATCH: Easing Bias Maintained, But 2026 Hold Likely) The October move was aimed at supporting activity at a time of persistent spare capacity and after a 0.9% quarterly GDP contraction in Q2.

Markets see little chance of a near-term move. However, RBNZ overnight index swaps imply a 2.66% OCR by December, with hiking risks weighted to the second half.

DATA POINTS

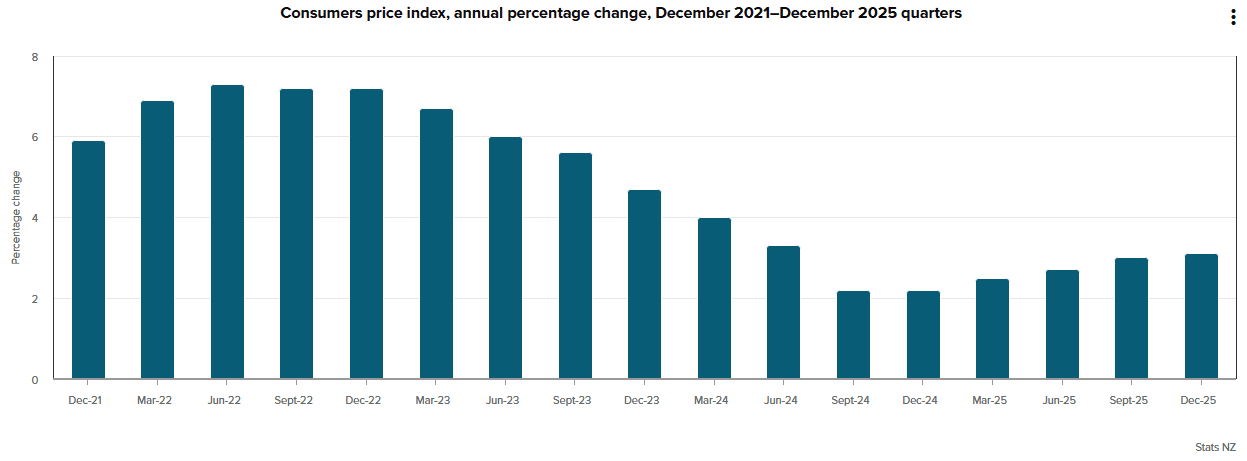

December-quarter consumer prices rose 3.1% year-on-year, 10bp above expectations, and 0.6% quarter-on-quarter, while core inflation remained roughly 50bp above 2%, according to Stats NZ. The data showed large increases in administered costs, including council rates, electricity, and health insurance. Prices for imported retail goods have also risen, while earlier easing in service-sector inflation has stalled, leaving the core inflation measure above 2%.

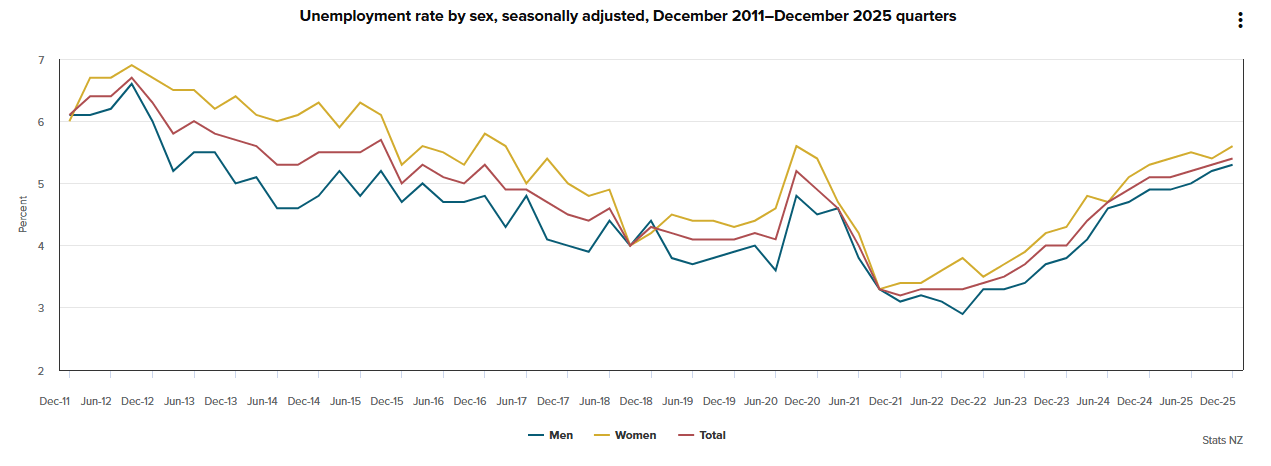

Unemployment edged up to 5.4% in the fourth quarter from 5.3% in Q3, while underutilisation remained steady at 13% and the employment rate rose slightly to 66.7%.

Most see signs of only a moderate recovery, that will drive RBNZ caution and keep the OCR at its current level until at least the second half when the economy should gain greater momentum. (See MNI: RBNZ To Hold, Hikes Not Likely Until H2 -Former Officials)

The RBNZ’s hawkish tone late last year, despite the easing bias in its forecasts and December's cut, pushed fixed-mortgage rates higher, effectively tightening financial conditions, according to former RBNZ assistant governor John McDermott, who noted that this, combined with the stronger New Zealand dollar, would weigh on the recovery. “The economy is still struggling, and there’s a lot of surplus capacity around, so it’s less than clear that the recovery could handle higher mortgage rates,” McDermott told MNI.

The Bank will release an updated set of forecasts within the Monetary Policy Statement, which will likely remove the easing bias in November's publication, give greater clarity on the neutral rate and show a slightly firmer OCR path.

NEW GOVERNOR

Wednesday’s meeting will also mark the first policy decision and post-decision press conference under the Bank's new Governor, Anna Breman. While Breman brings extensive policy experience from her former role at the Riksbank, she remains largely an unknown in terms of how she will manage policy and assess the New Zealand economy. The press conference is expected to provide the first clear insight into her stance on both.