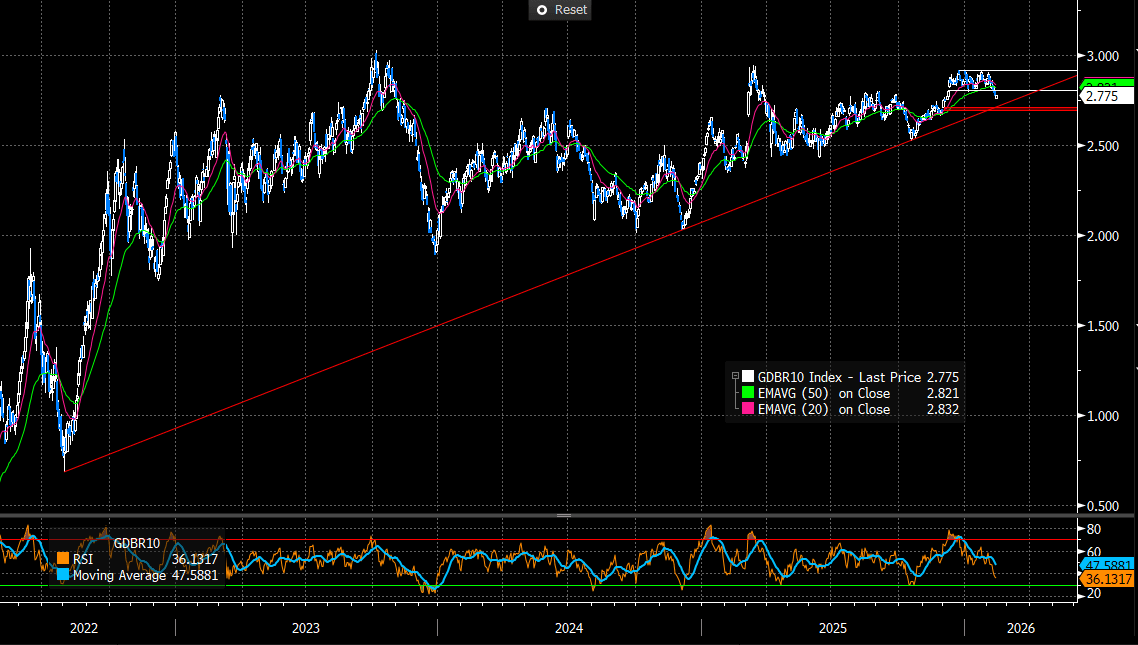

EGBS: 10-year Bund Yields Trying To Consolidate Below 2.80%

German yields are marginally lower this morning, with the 10-year yield notably trying to consolidate below the 2.80% figure. The next downside levels to watch are 2.75% and 2.70% - the latter closely aligning with trendline support (see chart). Despite well-documented domestic fiscal/issuance pressures, Bunds remain a popular safe haven /diversifier, which is countering upward yield moves for now. The median analyst still expects Bund yields to drift up towards 3% through the course of this year.

- Bund futures are –7 ticks at 128.94, after registering a multi-week high of 129.12 this morning. A bull mode in Bund futures remains intact recent technical breaks signal scope for an extension towards 129.55, the Nov 26 ‘25 high and the next key resistance point.

- 10-year EGB spreads to Bunds widened into yesterday’s close amid the broad-based souring of risk sentiment, but have stabilised a little this morning. The 10-year BTP/Bund spread is currently at 60.6bps.

- The second reading of Eurozone Q4 GDP was in line with the flash at 0.3% Q/Q. Meanwhile, employment growth of 0.2% Q/Q confirmed the ECB’s December projections. Spanish January HICP was revised down a tenth on a rounded basis to 2.4% Y/Y.

- Global focus remains on today’s US CPI report at 1330GMT. Meanwhile, Moody’s reviews Austria’s sovereign rating after hours (current rating: Aa1; Outlook Negative).

Figure 1: 10-year Bund Yields (Source: Bloomberg Finance L.P)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN AUCTION RESULTS: Bund Results

| 3.25% Jul-42 Bund | 0% Aug-52 Bund | 2.90% Aug-56 Bund | |

| ISIN | DE0001135432 | DE0001102572 | DE000BU2D012 |

| Total sold | E1bln | E1bln | E1bln |

| Allotted | E701mln | E809mln | E822mln |

| Previous | E733mln | E750mln | E1.14bln |

| Avg yield | 3.23% | 3.45% | 3.45% |

| Previous | 3.08% | 2.83% | 3.26% |

| Bid-to-offer | 0.80x | 1.24x | 1.72x |

| Previous | 0.91x | 1.41x | 0.99x |

| Bid-to-cover | 1.14x | 1.53x | 2.09x |

| Previous | 1.24x | 1.89x | 1.30x |

| Avg Price | 100.23 | 40.58 | 89.70 |

| Low Price | 100.17 | 40.56 | 89.69 |

| Pre-auction mid | 100.189 | 40.518 | 89.613 |

| Prev avg price | 102.24 | 46.63 | 93.08 |

| Prev low price | 102.22 | 46.60 | 93.06 |

| Prev mid-price | 102.172 | 46.615 | 92.961 |

| Previous date | 08-Oct-25 | 16-Apr-25 | 12-Nov-25 |

GILTS: Off Lows, Strong Demand At Auction Noted

Gilts have recovered from early London lows alongside peers.

- Futures +4 at 92.39.

- Bulls remain in technical control after the break of several key resistance levels last week.

- Resistance is now layered in at 92.62/72/91, while initial support is located at 91.84.

- Yields flat to ~1bp lower, 10s outperform on the curve.

- The ’25 low in 10s (4.363%) remains untested and protects the base of the upward sloping triangle we have previously identified (4.339% today).

- The presence of this morning’s GBP4.5bln 4.75% Oct-35 gilt auction didn’t provide much in the way of concessionary headwinds. The auction ultimately generated strong demand (highest bid-to-cover at a 10-year auction since August and the second highest ever volume of bids at a 10-year gilt auction), factoring into 10-Year outperformance.

- Comments from BoE MPC member Taylor reaffirmed his well-known dovish stance. He noted that “we can now see inflation at target in mid-2026, rather than having to wait until 2027 as in our previous projection. I see this as sustainable, given cooling wage growth, and I now therefore expect monetary policy to normalise at neutral sooner rather than later, as I said in the December minutes.”.

- GBP STIRs essentially flat on the day, 44bp of easing priced through year-end, next 25bp step not fully discounted until the end of the June MPC.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Feb-26 | 3.720 | -0.4 |

Mar-26 | 3.630 | -9.4 |

Apr-26 | 3.510 | -21.5 |

Jun-26 | 3.443 | -28.2 |

Jul-26 | 3.363 | -36.1 |

Sep-26 | 3.325 | -40.0 |

Nov-26 | 3.291 | -43.4 |

Dec-26 | 3.286 | -43.9 |

FOREX: JPY Off Lows, But Still Nursing Sharp Weekly Losses

- In contrast to JPY weakness that pervaded across the first few sessions of the week, the currency is stronger on the day headed into the NY crossover, helping press USDJPY back below Y159.00 and EURJPY back below Y185.00.

- Moves follow slightly more forceful language from Japan's Katayama, who again stressed how "deeply concerned" the authorities are on sudden currency weakness, and has kept the prime minister's office informed on options available and the trajectory of markets.

- Takaichi's junior coalition partner confirmed the plans to dissolve parliament and run early lower house elections, helping again affirm concerns around fiscal risk stemming from greater LDP control of the Diet. This, as well as the possible knock-on impacts on inflation from new government measures is again a JPY negative.

- Outside of Japan, GBP is trading well and rising against most others. This keeps the broad downtick in EURGBP intact, with the 200-dma of 0.8643 acting as first major support on any fresh selling pressure.

- US PPI data today will take a second look at the inflation picture in the US, albeit for October & November rather than yesterday's December CPI print (December PPI follows in the schedule on January 30th), which could contain any market reaction to an outside-of-expectations print today. That said, the PPI print today will provide further key inputs for PCE metrics - which could prove influential.

- Central bank speaker schedule is busy Wednesday, with appearances from Fed's Paulson, Miran, Kashkari, Bostic & Williams all due alongside BoE's Ramsden - who speaks on bank resolution regimes.