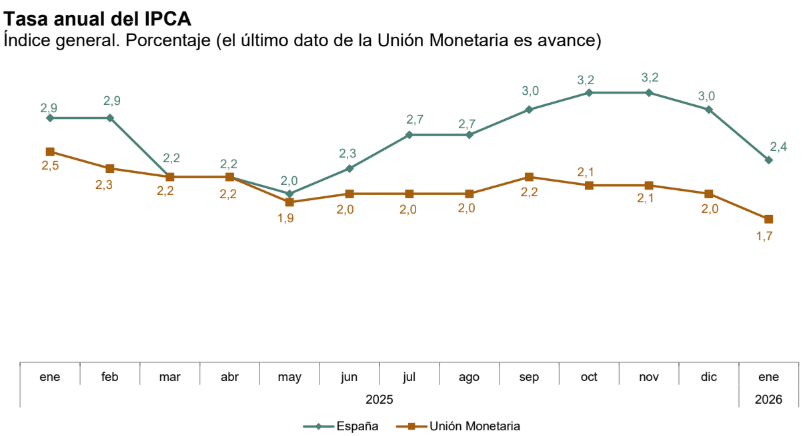

EUROPEAN INFLATION: Spain HICP Revised 0.1ppt Lower vs Flash, Core CPI Unrevised

Spain final Jan HICP printed at 2.42% Y/Y, 0.1ppt lower than the flash reading when rounded (vs 3.0% Dec). The M/M rate was also revised down 0.1ppt on a rounded basis to -0.8% M/M (vs 0.3% Dec) but unrounded was -0.75%.

- Core HICP (ex unprocessed foods and energy - not the Eurostat definition) was 2.77%Y/Y (flash was also 2.8%Y/Y).

- Headline CPI (non-HICP) was also revised a tenth lower than flash at 2.3% Y/Y (vs 2.9% Dec), while core CPI was unrevised at 2.6% Y/Y.

- COICOP divisions that most significantly influenced the decrease in CPI inflation (per INE): housing, water and household fuels (2.7% Y/Y vs 3.0% prior) - due to electricity price base effects (lower price increase than in Jan 2025), and transport (-0.1% Y/Y, down almost 2ppt) - due to lower fuels and lubricants prices for personal vehicles compared to the increase in Jan 2025.

- Housing, water and household fuels contributed +0.112ppt to the monthly CPI rate, at 0.9% M/M, due to the increase in electricity prices noted above.

- Notable negative monthly drivers: clothing and footwear (-13.1% M/M) - contributing -0.468 to CPI, and due to winter sales; recreation sports and culture (-2.8% M/M) - contributing -0.210, due to lower package holidays; and transportation (-1.1% M/M) - contributing -0.165 due to lower prices for "other services related to personal vehicles" and fuels and lubricants for personal vehicles.

Chart source: INE. Blue line is Spain HICP Y/Y, orange line is Eurozone HICP Y/Y (flash estimate for Jan 2026).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Still Looking For Gains

- RES 4: 1.4023 76.4% retracement of the Nov 5 - Dec 26 bear leg

- RES 3: 1.3977 High Dec 4

- RES 2: 1.3950 61.8% retracement of the Nov 5 - Dec 26 bear leg

- RES 1: 1.3920 High Jan 9

- PRICE: 1.3889 @ 08:11 GMT Jan 14

- SUP 1: 1.3851/3814 50- and 20-day EMA values

- SUP 2: 1.3752 Low Jan 6

- SUP 3: 1.3701 Low Jan 2

- SUP 4: 1.3643 Low Dec 26 and the bear trigger

A bull cycle in USDCAD remains in place and the pair is trading closer to its recent highs. The pair is through the 50-day EMA, at 1.3851, and a clear break of this average highlights a stronger reversal. Sights are on 1.3950 next, a Fibonacci retracement. On the downside, initial support to watch is 1.3814, the 20-day EMA. A breach of it would instead highlight a possible reversal.

BOE: Taylor Re-iterates Preference For Further Cuts

BOE Taylor full speech titled "Driving over the peak, or a false summit?" is here

The speech is largely historical/theoretical in nature, arguing that " there is, at the level of the deep economic fundamentals driving trade, a lot of reason for optimism about the scope for international trade to remain robust and even grow, in the years ahead".

It ends with some monetary policy implications. The key part: “We can now see inflation at target in mid-2026, rather than having to wait until 2027 as in our previous projection. I see this as sustainable, given cooling wage growth, and I now therefore expect monetary policy to normalise at neutral sooner rather than later, as I said in the December minutes. Interest rates should continue on a downward path, that is if my outlook continues to match up with the data, as it has done over the past year”.

Additional excerpts from the conclusion:

- “My basic message here is that these are very welcome forces. Smoother international trade is, at the end of the Bank of England Page 24 day, a positive supply shock – for those countries who choose to participate, at least. It brings more and more affordable goods and services into the home economy. As such it is clearly disinflationary, and helps central banks maintain low and stable inflation while boosting economic growth and welfare.”

- “In the short run, however, trade diversion will be the bigger story. I will again repeat, from my speech in Cambridge, my sense of how this is playing out in the UK. I think we are seeing signs of substantial trade diversion into the UK and also into the EU, our main trading partner, with the latter more clearly evident from some of the policy response to import surges in some sectors.”

- “The Bank of England has considered various scenarios and estimates that trade diversion could lower inflation in the UK by some 0.2 percentage points in 2026 and 2027, abating to 0.1 percentage points in 2028, most via lower import prices (see Box C of the May 2025 Monetary Policy Report). This is a baseline figure, and arguably quite conservative. My judgement of the volumes and elasticities is a bit higher than this baseline and has been one factor therefore in my judgement throughout 2025 that UK inflation would end up on a lower trace than in our central projection.”

- “In the medium term, the economy should return to long-run trend productivity growth. And as I said today, the adjustments to the 2025 trade shock should eventually feed through, trade should prove resilient. Both of which would be welcome disinflationary forces that keep inflation well anchored.”

AUDUSD TECHS: Monitoring Support

- RES 4: 0.6872 38.2% retracement of the 2021 - 2025 L/T downtrend

- RES 3: 0.6858 1.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.6795 0.764 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 1: 0.6767 High Jan 7 and the bull trigger

- PRICE: 0.6694 @ 08:03 GMT Jan 14

- SUP 1: 0.6664 Low Jan 9

- SUP 2: 0.6632 50-day EMA

- SUP 3: 0.6593 Low Dec 18

- SUP 4: 0.6553 Low Dec 3

Recent weakness in AUDUSD still appears corrective and has allowed an overbought condition to unwind. Initial firm support around the 20-day EMA, at 0.6681, has been pierced. A clear break of it would expose support at the 50-day EMA, at 0.6632. The area between the two EMAs still represents a key support zone. For bulls, a resumption of the uptrend would open 0.6795 next, a Fibonacci projection.