MNI US MARKETS ANALYSIS - USD Rally Running Out of Steam

Highlights:

- Ripple effect of Iran conflict continues, but USD rally abates

- Crude oil holds bulk of rally, but off highs on reports of back channel Iran-US talks

- ISM services, ADP data eyed to gauge NFP risks

US TSYS: Modest Losses Pared On Iran Outreach Report, Risk Sentiment Still Fluid

Treasuries have modestly pared losses after the NYT reported that Iran's Ministry of Intelligence reached out indirectly to the C.I.A. with an offer to discuss terms for ending the conflict the day after strikes began - there continues to be a fluid correlation between equities and yields. Geopolitical headlines around Middle East escalation/off-ramps will likely remain in main focus although today also sees monthly ADP employment (before Friday’s NFP report) and ISM services (after its manufacturing counterpart saw a jump in prices paid).

- Cash yields are 1-2.6bp higher.

- 2s10s at 56.6bp (+0.3bp) is little changed after yesterday reversing most of its slide to 51.3bp for its flattest since late November.

- TYM6 trades at 112-28+ (-04) on heavy cumulative volumes of 630k, within yesterday’s range of 112-16+ to 113-07+.

- Having reversed sharply lower on Tuesday, it maintains a softer tone with the recent overbought condition unwinding. Support is seen at 112-16+/112-16 (Mar 3 low/50-day EMA) after which lies 112-11 (Fibo retrace of Jan 20 – Mar 2 bull leg), whilst resistance is seen at 113-13+ (Fibo projection of Feb 19-23-25 price swing).

- Data: MBA mortgage apps (0700ET), ADP employment Feb (0815ET), S&P Global US services/composite PMI Feb final (0945ET), ISM services Feb (1000ET)

- Fedspeak: Beige Book (1400ET)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: WH Press Sec Leavitt press briefing (1300ET), Trump in roundtable on ratepayer protection pledge (1500ET)

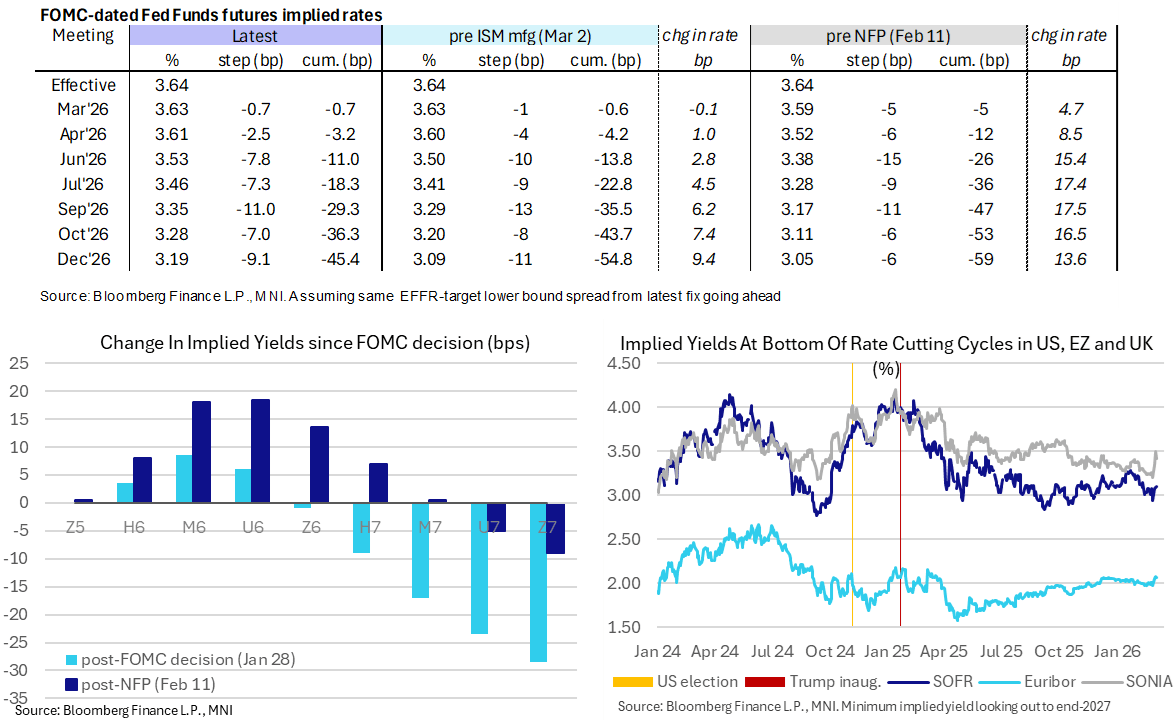

STIR: Fed Rate Cut Expectations Within Wide Ranges, ADP & ISM Services Ahead

- US rates pared overnight losses following the NYT reporting that Iran’s Ministry of Intelligence reached out indirectly to the C.I.A. with an offer to discuss terms for ending the conflict the day after strikes began.

- Fed Funds implied rates are up to 1.5bp higher on the day for the July meeting, with a next Fed cut still only seen in September.

- The 45bp of cuts to year-end sits within yesterday’s notably wide range of 38-52bp on volatile risk sentiment.

- Cumulative cuts from 3.64% effective: 0.5bp Mar, 3bp Apr, 11bp Jun, 18.5bp Jul, 29.5bp Sep, 36.5bp Oct and 45.5bp Dec.

- SOFR futures are up to 1.5 ticks lower in 2027 contracts, with the terminal implied yield of 3.10% (U7, +2bp) comfortably within the ytd range of 2.94-3.285%.

- Away from data headlined by ADP employment and ISM services, the Fed’s Beige Book will offer a latest look at regional momentum in still important liaison programmes.

- Cleveland Fed’s Hammack (’26 voter, hawk) told the NYT that the escalating conflict in the Middle East represents a new inflationary risk that she is watching closely. Higher energy prices could translate to a more persistent inflation problem for the Fed, but at the same time dent consumer demand, although it is far too early to know what the overall economic impact will be.

SOFR: Mix Of Positioning Moves In Futures On Tuesday, Oil Swings In Control

OI data points to a mix of dominant positioning themes across packs as the SOFR futures strip twist flattened on Tuesday.

- Short setting dominated in the whites with long cover noted in the reds, before short cover came to the fore in the greens & blues.

- Long cover in SFRZ6 provided the largest net positioning move in single contract terms.

- Swings in commodity prices after the recent escalation in the Middle East continued to shape sentiment.

| 03-Mar-26 | 02-Mar-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,311,150 | 1,303,923 | +7,227 | Whites | +20,894 |

SFRH6 | 1,338,314 | 1,328,087 | +10,227 | Reds | -18,103 |

SFRM6 | 1,313,382 | 1,324,585 | -11,203 | Greens | -11,764 |

SFRU6 | 1,235,721 | 1,221,078 | +14,643 | Blues | -28,959 |

SFRZ6 | 1,328,772 | 1,376,511 | -47,739 |

|

|

SFRH7 | 918,148 | 914,876 | +3,272 |

|

|

SFRM7 | 881,340 | 856,736 | +24,604 |

|

|

SFRU7 | 723,165 | 721,405 | +1,760 |

|

|

SFRZ7 | 1,072,383 | 1,066,863 | +5,520 |

|

|

SFRH8 | 549,439 | 550,360 | -921 |

|

|

SFRM8 | 425,822 | 427,529 | -1,707 |

|

|

SFRU8 | 366,737 | 381,393 | -14,656 |

|

|

SFRZ8 | 379,157 | 392,860 | -13,703 |

|

|

SFRH9 | 227,725 | 229,215 | -1,490 |

|

|

SFRM9 | 189,246 | 198,159 | -8,913 |

|

|

SFRU9 | 179,898 | 184,751 | -4,853 |

|

|

ISRAEL: Local Media Reports IDF Says Two Weeks More Bombing Of Iran

Israel's Channel 13 reports that "Senior IDF officers say today (Wednesday) that we have two more weeks of bombings across Iran ahead of us, with the plan being to attack thousands of targets with heavy bombers from the United States military - including all targets of the regime, the Revolutionary Guards, Basij, satellites, drones and tanks." Al Jazeera, reports Israel's Channel 12 stating the bombardment will last "at least" two weeks, rather than a set fortnight.

- Separately, Israel's Ynet reports that "In terms of the targets ahead, the IDF explains that there is a systematic plan to move to a set of military targets of the regime. These are thousands of targets. To do this, Americans are needed, and therefore, a systematic crushing of all regime targets and military targets, throughout Iran, is currently expected in the next two weeks."

- These are the first public comments attributed to the IDF with at least some form of timeframe for how long the bombardment of Iran could continue. Of course, this timeline is almost certain to shift around given the highly fluid nature of the geopolitical situation in the region. A key question is whether a two-week aerial offensive is a precursor to further action, or the extent of the attacks from Israel and the US.

IRAN: Senior Cleric-'We Are Close To Selecting New Supreme Leader'

State TV reports comments from Ayatollah Ahmad Khatami, Temporary Friday Imam of Tehran and a senior member of the Assembly of Experts, saying that 'Leadership candidates have been identified and we are close to selecting the new supreme leader. The new leader will be chosen at the earliest opportunity, but the current situation is wartime, so we are taking all precautions.'

- As noted earlier (IRAN: Mojtaba Khamenei Survived Strikes, Seen as Possible Next Leader: RTRS), the late Supreme Leader Ayatollah Ali Khamenei's son, Mojtaba, is reported to have survived US/Israeli strikes and is well positioned to be confirmed as the next Iranian leader. The selection of Khamenei's son would not be a knee-jerk reaction. Shortlists from analysts and observers have included his name for many years.

- In a statement earlier today, Israeli Defence Minister Israel Katz said in a statement that the next supreme leader will be an “unequivocal target for elimination" adding, “It does not matter what his name is or where he hides.”

- Katz: "We will continue to act with full force, together with our American partners, to dismantle the regime’s capabilities and create the conditions for the Iranian people to overthrow and replace it.”

- Israeli intelligence in the early stages of the conflict has proved extremely effective in identifying how and when to take out senior targets. It remains to be seen whether such accuracy can be maintained amid the fog of war, and with a much more cautious Iranian high command.

STIR: SONIA/Euribor Dec '26 Spread Trades To Widest Since BoE Dovish Hold

The SONIA/Euribor December ‘26 spread has widened by 11bp since Friday, registering the highest close seen since the day before the BoE’s dovish hold in early February. 135bp held during yesterday’s move.

- Those that look for more than one BoE rate cut this year may engage in SONIA longs via spread tighteners here.

- A deeper scale of easing was priced into GBP STIRs than their ECB counterpart (~50bp vs. ~10bp late on Friday), which along with the ECB’s “in a good place” mantra, provided scope for greater movement in GBP STIRs in any hawkish adjustment.

- However, relative exposure of electricity prices to the rally in natural gas is also worth noting (given the commodity-centric nature of the hawkish move in the wake of the escalation in the Middle East), with the UK's electricity prices being far more closely tied to the natural gas price relative to Europe.

- We still think that a BoE cut in April is relatively likely, while the presence of additional slack in the UK labour market could help promote further easing latter in ’26 (market prices ~25bp of cumulative cuts for the year at this stage).

- On the Euribor leg, while the bar to an ECB move in either direction is high, it is worth noting that our latest sources piece warned that the ECB would have lower tolerance for any extended energy price shock resulting from the Iran war than in the past. This presents hawkish risks if the energy price move extends and becomes more prolonged.

- The spread last trades at 131.5bp. Cycle closing lows are located at 118.5bp.

SOUTH KOREA: Finance Minister Says to Respond to Market Fallout "Calmly"

"S.KOREA FINMIN: STOCK, FOREX MARKET TUMBLE DUE TO EXTERNAL FACTORS, NOT DOMESTIC ECONOMIC FUNDAMENTALS, GOVT TO RESPOND CALMLY" - Reuters

- Follows the largest one-day drawdown in the KOSPI on record overnight. We noted yesterday markets will begin to gauge intervention options from the BoK and South Korean government after the scale of foreign capital outflow this week - particularly after they floated market stabilisation tools overnight: https://www.mnimarkets.com/articles/markets-gauge-intervention-options-as-krw-slides-to-new-lows-1772551272664

EUROPE ISSUANCE UPDATE:

German auction results

- E1bln (E960mln allotted) of the 2.30% Feb-33 Green Bund. Avg yield 2.53% (bid-to-offer 1.69x; bid-to-cover 1.76x).

FOREX: USD Index Consolidating Weekly Advance, AUD Volatility Remains High

- Global markets continue to digest implications from the Middle East conflict as hostilities go on. With an emerging frontrunner for the next Supreme Leader, chances are a collapse of the Mullah regime is not imminent, deepening the prospects for a prolonged crisis. Given the US's relative isolation to energy market developments and safe haven flows emanating from the broader hit to risk sentiment, the Ice Dollar Index is consolidating a 1.4% advance this week.

- However, it is worth noting the index remains well off yesterday’s 99.68 peak, with most recent NYT headlines on Iran operatives offering to discuss ceasefire terms improving risk sentiment somewhat and weighing moderately on the greenback.

- AUD volatility has remained a key feature of currency markets this week, with AUDUSD posting an 88pip range on Wednesday. Overall, spot remains towards the middle of the impressive 0.7125-0.6950 range posted yesterday. To the downside, the 50-day EMA at 0.6925 represents the key support level, keeping the bullish trend condition intact for now.

- This morning's headlines from SNB's Vice Martin confirm a step up in the forcefulness of the central bank’s language on FX after Monday's emailed statement on a higher readiness to intervene. Alongside positioning dynamics and the firmer dollar, USDCHF had an impressive short squeeze across Monday and Tuesday, rising as much as 2.7% from the lows. Moves have moderated since and for EURCHF, we have slipped back below 0.9100 and remain just 65pips above the recent cycle lows at 0.9025.

- For the major pairs, EURUSD has stabilised back above 1.16, while USDJPY has been edging lower after 158.00 capped the price action yesterday. BOJ rhetoric on intervention appears to have stalled the USDJPY recovery, despite fiscal headwinds remaining a key area of concern in Japan.

- MBA mortgage applications, ADP employment, the final Services PMI and ISM Services are on the data calendar for today. A set of ECB speakers as well as BoC's Macklem are scheduled, and the Fed will release its most recent beige book.

OPTIONS: Expiries for Mar04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E640mln), $1.1600(E1.2bln), $1.1675(E624mln), $1.1750(E963mln)

- USD/JPY: Y156.00($748mln)

- EUR/GBP: Gbp0.8650(E937mln)

- AUD/USD: $0.7000(A$815mln)

- USD/CNY: Cny6.8850($750mln), Cny6.9150($896mln)

EQUITIES: E-Mini S&P Yet to Convincingly Clear Support at 6751.50

- A strong short-term reversal in EuroStoxx 50 futures has resulted in a breach of both the 20- and 50-day EMAs. This highlights potential for a deeper near-term pullback and Tuesday’s sell-off confirms this threat. Sights are on 5689.00 next, the Dec 18 ‘25 low. On the upside, initial firm resistance is 5967.61, the 50-day EMA ahead of 6038.77, the 20-day EMA. For now, gains would likely be corrective.

- A bearish short-term tone in S&P E-Minis remains intact. For now, the contract is trading inside a range. Attention is on the base of the range at 6751.50, the Feb 6 low. This level has been pierced, a clear break would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

COMMODITIES: WTI Futures Trading Close to This Week's Highs

- A volatile bull cycle in WTI futures remains intact. Despite being in overbought territory, the contract traded higher Tuesday to confirm a resumption of the current uptrend. The move higher paves the way for a climb towards $78.05 next, a Fibonacci projection, ahead of the $80.00 handle. The first key support to monitor is $65.91, the 20-day EMA. A pullback would allow the overbought condition to unwind.

- Gold has pulled back from Monday’s intraday high. For now, a short-term bullish theme remains intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $5077.0, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 04/03/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/03/2026 | - | Chinese People's Political Consultative Conference | ||

| 04/03/2026 | 1330/1430 | ECB de Guindos Remarks at American Academy, Berlin | ||

| 04/03/2026 | 1445/0945 | *** | S&P Global Composite & Services Index (final) | |

| 04/03/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/03/2026 | 1520/1020 | BOC Governor Macklem speech | ||

| 04/03/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/03/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/03/2026 | 0030/1130 | ** | Trade Balance | |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0745/0845 | * | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Unemployment | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Italy Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Germany Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/03/2026 | 0850/0950 | ECB de Guindos in Conversation at IIF European Investment Summit | ||

| 05/03/2026 | 0900/1000 | * | Retail Sales | |

| 05/03/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/03/2026 | 0930/0930 | *** | BOE Decision Making Panel | |

| 05/03/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/03/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 05/03/2026 | - | National People's Congress | ||

| 05/03/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/03/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/03/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 05/03/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 05/03/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/03/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/03/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/03/2026 | 1700/1800 | ECB Lagarde Lecture on Global Risk | ||

| 05/03/2026 | 1815/1315 | Fed's Michelle Bowman |