STIR: Fed Rate Cut Expectations Within Wide Ranges, ADP & ISM Services Ahead

Mar-04 11:30

- US rates pared overnight losses following the NYT reporting that Iran’s Ministry of Intelligence reached out indirectly to the C.I.A. with an offer to discuss terms for ending the conflict the day after strikes began.

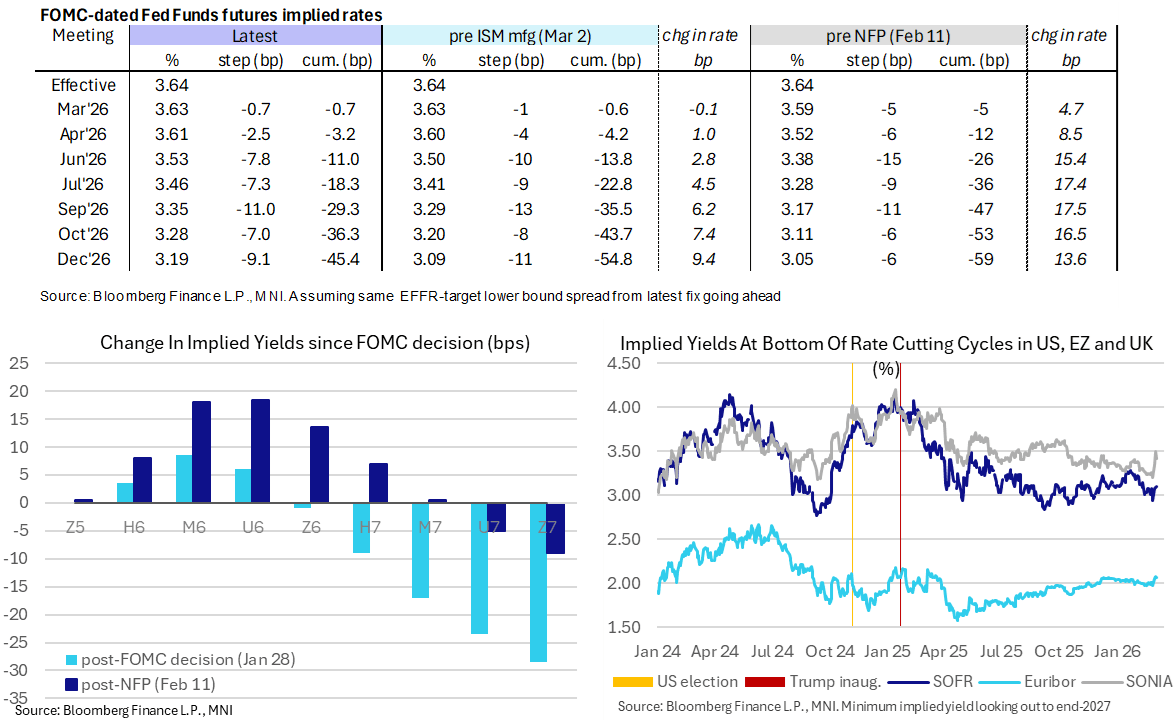

- Fed Funds implied rates are up to 1.5bp higher on the day for the July meeting, with a next Fed cut still only seen in September.

- The 45bp of cuts to year-end sits within yesterday’s notably wide range of 38-52bp on volatile risk sentiment.

- Cumulative cuts from 3.64% effective: 0.5bp Mar, 3bp Apr, 11bp Jun, 18.5bp Jul, 29.5bp Sep, 36.5bp Oct and 45.5bp Dec.

- SOFR futures are up to 1.5 ticks lower in 2027 contracts, with the terminal implied yield of 3.10% (U7, +2bp) comfortably within the ytd range of 2.94-3.285%.

- Away from data headlined by ADP employment and ISM services, the Fed’s Beige Book will offer a latest look at regional momentum in still important liaison programmes.

- Cleveland Fed’s Hammack (’26 voter, hawk) told the NYT that the escalating conflict in the Middle East represents a new inflationary risk that she is watching closely. Higher energy prices could translate to a more persistent inflation problem for the Fed, but at the same time dent consumer demand, although it is far too early to know what the overall economic impact will be.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHF: Solid Turnaround for EURCHF as Momentum Sub 0.9200 in Focus

Feb-02 11:28

- Swiss Franc price action is catching the eye Monday, a notable underperformer across G10 as we approach the NY crossover. After reaching a new decade low of 0.9140 in APAC trade, EURCHF has had a solid turnaround, rising to a session high of 0.9212 in recent minutes.

- Broader cross-asset sentiment has most recently stabilised, potentially assisting the cross/CHF recovery, however, given the de-risking that has been on display elsewhere since Friday, short-term positioning dynamics may be assisting the squeeze.

- EURCHF lows today may also be approaching the threshold that could be considered alarming for the SNB. We highlighted last week that JPM stated we need to see EURCHF getting closer to 0.91 quickly for them to get worried, while ING said "the fact that EURCHF is offered near 0.92 and that USDCHF has broken under 0.7800 will be ringing alarm bells in Zurich”.

- As a reminder, President Schlegel spoke last week on the current economic situation and monetary policy, and notably there was no mention of the recent CHF strength.

- Today’s CHF reversal comes despite the earlier retail sales data beat, underpinning the narrative that the Swiss consumer is in solid shape and, barring new shocks, the SNB is likely to hold its policy rate at 0% for the foreseeable future.

EGBS: UBH6 Sold

Feb-02 11:13

UBH6 5K blocked at 109.86, recent downtick suggests a seller, despite being conducted above the prevailing offer at time quoted by BBG. DV01 ~EUR1.06mln.

AUD: AUDUSD Winning Streak Halted, RBA Tightening in Focus

Feb-02 11:09

- The weaker commodity complex, with oil also down ~5%, did weigh on the likes of AUD and NZD to start the week, although both have stabilised across the European morning. Positioning dynamics will also be a consideration for AUD as we approach the RBA decision tomorrow.

- The combination of a resilient labour market and stronger than expected Dec/Q4 inflation has the sell-side consensus expecting a 25bp RBA rate hike tomorrow. If delivered, focus will be on how much follow up action the central bank sees as needed to ensure inflation returns to target.

- For AUDUSD, the recent streak of consecutive winning sessions came to an end on Friday, and spot has subsequently stabilised around 0.6950. The latest pullback highlights the start of a corrective phase. If correct, it suggests potential for an extension towards support around the 20-day EMA, at 0.6835. This would also confirm an unwinding of the recent overbought trend condition.

- Key short-term resistance and the bull trigger have been defined at 0.7094, the Jan 29 high.

Trending Top

May-01 21:26