US TSYS: Modest Losses Pared On Iran Outreach Report, Risk Sentiment Still Fluid

Mar-04 11:51

Treasuries have modestly pared losses after the NYT reported that Iran's Ministry of Intelligence reached out indirectly to the C.I.A. with an offer to discuss terms for ending the conflict the day after strikes began - there continues to be a fluid correlation between equities and yields. Geopolitical headlines around Middle East escalation/off-ramps will likely remain in main focus although today also sees monthly ADP employment (before Friday’s NFP report) and ISM services (after its manufacturing counterpart saw a jump in prices paid).

- Cash yields are 1-2.6bp higher.

- 2s10s at 56.6bp (+0.3bp) is little changed after yesterday reversing most of its slide to 51.3bp for its flattest since late November.

- TYM6 trades at 112-28+ (-04) on heavy cumulative volumes of 630k, within yesterday’s range of 112-16+ to 113-07+.

- Having reversed sharply lower on Tuesday, it maintains a softer tone with the recent overbought condition unwinding. Support is seen at 112-16+/112-16 (Mar 3 low/50-day EMA) after which lies 112-11 (Fibo retrace of Jan 20 – Mar 2 bull leg), whilst resistance is seen at 113-13+ (Fibo projection of Feb 19-23-25 price swing).

- Data: MBA mortgage apps (0700ET), ADP employment Feb (0815ET), S&P Global US services/composite PMI Feb final (0945ET), ISM services Feb (1000ET)

- Fedspeak: Beige Book (1400ET)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: WH Press Sec Leavitt press briefing (1300ET), Trump in roundtable on ratepayer protection pledge (1500ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - USD Unwinds Its Oversold Trend Condition

Feb-02 11:49

- In FX, EURUSD is trading at its retracement lows and remains below last week’s high print. The move down signals potential for an extension towards 1.1793, the 20- day EMA. Support at the 50-day EMA lies at 1.1729. A breach of the 50-day average would suggest scope for a deeper retracement. Initial firm resistance is at 1.1975, the Jan 30 high.

- The move down in GBPUSD is considered corrective and a continuation lower would allow a recent overbought condition to unwind. The initial firm support to watch is at the 20-day EMA, at 1.3578. Support at the 50-day EMA lies at 1.3471. The medium-term trend theme remains bullish. The bull trigger has been defined at 1.3868, the Jan 27 high.

- USDJPY is holding on to the bulk of its latest gains. The recovery highlights a corrective cycle that remains in play for now. Firm resistance to watch is at 155.76, the 50-day EMA. A clear break of this average would signal a possible bullish reversal. Key short-term support has been defined at 152.10, the Jan 27 low. A break of it would resume the recent downtrend.

SWEDEN: Riksbank Minutes In Focus On Wednesday, SEK A Downside Inflation Risk

Feb-02 11:41

- Last week’s Riksbank decision reaffirmed that the policy rate is expected to remain at 1.75% for “some time to come”, but nonetheless contained some dovish tweaks on inflation risks and geopolitical uncertainty. As a result, we think the near-term risk of a cut has risen a little relative to before the meeting.

- This places focus on Wednesday’s January meeting minutes. We are particularly interested to see if Deputy Governor Jansson further opens the door to a rate cut vote later this year.

- The recent strengthening in the SEK presents an important downside inflation risk to monitor. In an interview with the MNI Policy Team, Governor Thedeen noted that “at this this level we don't have a strong view that it's undervalued or it's overvalued.”. He also suggested that "When inflation was high … the inflationary effect of the krona down move was more pronounced than we thought. And maybe now there's some indication that, maybe, the effects on the deflationary side are also slightly more pronounced. Will that last? Well, very uncertain,"

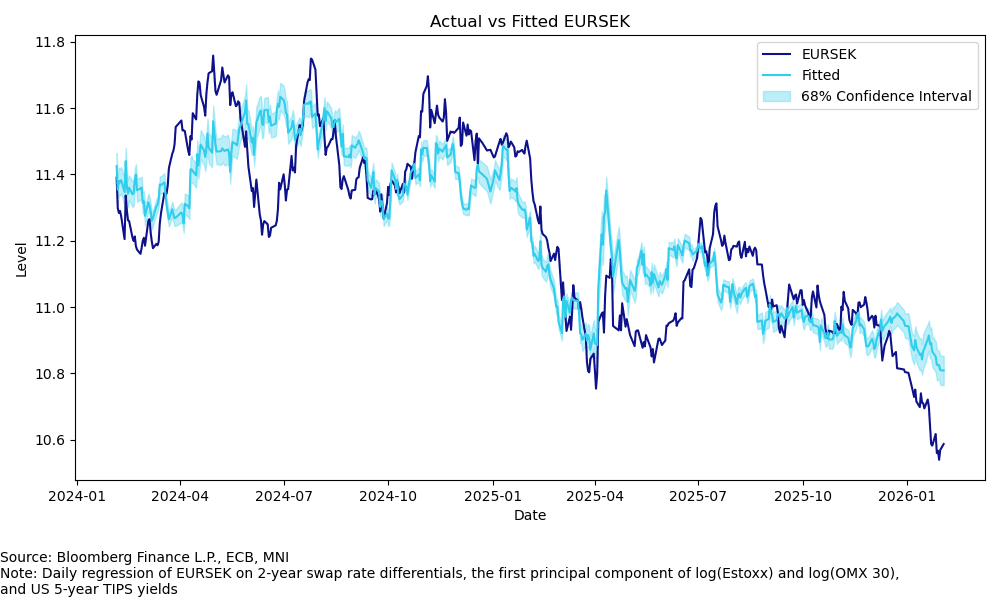

- EURSEK is currently at ~10.57, off Friday's multi-year low of 10.5054 but still comfortably above the ~10.80 fair value implied by a linear model based on nominal rate spreads, equity proxies and US real yields.

- Swedish January flash inflation is due on Thursday morning, with consensus expecting CPIF ex-energy to fall below the 2% target to 1.9% Y/Y (vs 2.3% prior), below the Riksbank’s 2.04% projection.

- Elsewhere, this morning’s January manufacturing PMI provided another piece of evidence supporting the cyclical recovery. The PMI rose to a four year high of 56.0, above December’s 55.4 reading. This follows a consolidation in expansionary territory for the Economic Tendency Indicator’s manufacturing sentiment series last week. Increases in domestic new orders and employment were noted in the PMI.

LOOK AHEAD: Monday Data Calendar: S&P Mfg PMI, ISMs, Tsy Quarterly Refunding

Feb-02 11:40

- US Data/Speaker Calendar (prior, estimate). All times ET

- 02/02 0945 S&P Global US Mfg PMI (51.9, 52.0)

- 02/02 1000 ISM New Orders (47.4 rev, --), Employment (44.8 rev, 46.0)

- 02/02 1000 ISM Manufacturing (47.9, 48.5), Prices Paid (58.5, 59.3)

- 02/02 1130 US Tsy $89B 13W & $77B 26W bill auctions

- 02/02 1230 Atl Fed Bostic moderated Q&A

- 02/02 1500 US Tsy Quarterly Refunding for current (Jan-Mar) & next (Apr-Jun) quarter

- Source: Bloomberg Finance L.P. / MNI

Trending Top

May-01 21:26