MNI US MARKETS ANALYSIS - Powell Provides Crux of Fri Session

Highlights:

- Powell's speech to be watched carefully for September meeting clues; markets hold a balance of 17bps cuts priced

- USD Index holds firm, helping GBP/USD print a sixth session of lower highs and lower lows

- Lagarde, Ueda, Bailey, Thedeen, Hammack and Collins among others to appear at policy symposium

US TSYS: Treading Water Ahead Of Powell, Trump Announcement Follows

- Treasuries have pared minor losses to leave them little changed on the day with a firm focus on Fed Chair Powell’s Jackson Hole address at 1000ET.

- MNI Preview: https://media.marketnews.com/Fed_JH_Preview_Aug2025_44c9766301.pdf

- President Trump is also set to make an announcement at 1200ET. There’s no topic at present although it will follow Powell’s Jackson Hole appearance and also comes after his federal police visit to DC yesterday.

- Cash yields are 0.3-0.7bp higher on the day.

- Yesterday’s strong flash PMIs and patient Fedspeak from Hammack saw a flattening off recent steeps, with 5s30s for example currently at 106.9bps off Wednesday's fresh ytd high of ~111bps.

- TYU5 trades at 111-17 (-00+) on subdued cumulative volumes of 235k.

- Support is still seen at 111-12 (50-day EMA) having some close with 111-13+ after last Thursday’s PPI report. A test there could open 110-23+ (Aug 1 low) but a bullish theme remains intact with resistance seen at a bull trigger of 112-15+ (Aug 5 high).

- Data: None scheduled

- Fedspeak: Collins (0900ET), Powell (1000ET), Hammack (1130ET) – see STIR bullet

- Politics: President Trump makes an announcement (1200ET)

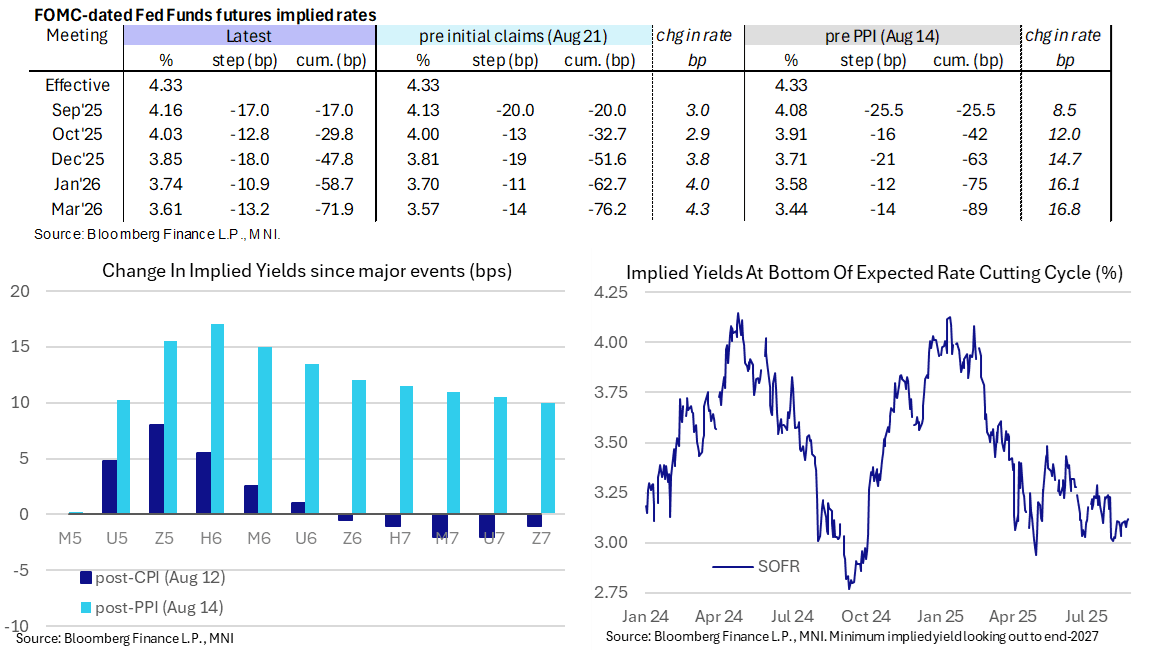

STIR: 17bp Of Fed Cuts Priced For Next Month Ahead Of Powell

- Near-term Fed Funds implied rates are at their most hawkish since the Aug 1 nonfarm payrolls report, aided by yesterday’s surprisingly strong flash PMIs and more patient Fedspeak.

- That path includes 17bp of cuts next month vs up to 26bp after last week’s CPI release, with Fed Chair Powell’s Jackson Hole speech firmly in focus today 1000ET.

- MNI Preview: https://media.marketnews.com/Fed_JH_Preview_Aug2025_44c9766301.pdf

- Cumulative cuts from 4.33% effective: 17bp Sep, 30bp Oct, 48bp Dec, 58.5bp Jan and 72bp Mar.

- The SOFR implied terminal yield of 3.12% (SFRH7, +1bp) last closed higher pre-payrolls, although just about keeps to its rough range of 125bp +/-5bp of cuts from current levels seen in the month to date.

- Chicago Fed’s Goolsbee (’25 voter, dove) reiterated late yesterday that Sept is a ‘live’ meeting but, for one of the more dovish FOMC members, he thought the rise in services inflation is a “dangerous” data point and that current tariffs don’t look “one and done”. Independence from political interference is critical.

- Boston Fed’s Collins (’25 voter) meanwhile said a rate cut may be appropriate soon if the labor outlook worsens and that the Fed can’t wait for full clarity on inflation to consider cuts. She had advocated for an “actively patient” policy approach prior to the July FOMC meeting.

- Collins speaks again today on Bloomberg TV at 0900ET whilst Hammack (’26 voter, hawk) follows Powell at 1130ET on CNBC after saying yesterday she doesn’t see the case for a September cut as data stand.

SOFR: Mix Of Short Setting And Long Cover Seen In Futures On Thursday

OI data points to a mix of net short setting and long cover during Thursday’s move lower in SOFR futures, as markets reacted to the latest round of data and ongoing hawkish Fedspeak from Hammack.

- Short setting was more prominent in the whites and blues, while long cover was more meaningful in the reds and greens.

| 21-Aug-25 | 20-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,193,761 | 1,201,669 | -7,908 | Whites | +122,091 |

SFRU5 | 1,323,790 | 1,285,920 | +37,870 | Reds | -49,088 |

SFRZ5 | 1,445,894 | 1,390,807 | +55,087 | Greens | -28,504 |

SFRH6 | 1,087,165 | 1,050,123 | +37,042 | Blues | +25,062 |

SFRM6 | 930,069 | 929,516 | +553 |

|

|

SFRU6 | 888,164 | 898,573 | -10,409 |

|

|

SFRZ6 | 988,636 | 997,409 | -8,773 |

|

|

SFRH7 | 707,809 | 738,268 | -30,459 |

|

|

SFRM7 | 850,795 | 904,302 | -53,507 |

|

|

SFRU7 | 604,017 | 608,581 | -4,564 |

|

|

SFRZ7 | 614,579 | 601,939 | +12,640 |

|

|

SFRH8 | 376,262 | 359,335 | +16,927 |

|

|

SFRM8 | 288,303 | 279,377 | +8,926 |

|

|

SFRU8 | 220,850 | 209,693 | +11,157 |

|

|

SFRZ8 | 224,434 | 217,751 | +6,683 |

|

|

SFRH9 | 149,209 | 150,913 | -1,704 |

|

|

JAPAN: PM Ishiba's Position Looks More Assured As Polling Improves

Following the 20 July House of Councillors election it was widely assumed that PM Shigeru Ishiba's ouster from office was a matter of 'when' rather than 'if' after the ruling Liberal Democratic Party (LDP)-Komeito coalition lost its majority in the upper house (having already lost its majority in the lower house in the 2024 election). However, a groundswell of public support for the PM has seen betting market odds of his removal from office (in 2025 at least) plummet.

- Data from Polymarket shows political bettors assigning a 21% implied probability that Ishiba leaves office in 2025. This is down from 61% on 17 August, and a peak of 77.8% on 26 July.

- A mid-August opinion poll for Jiji Press showed 65.9% of LDP supporters backing Ishiba to remain in office, compared to 24.6% saying he should resign. Among all respondents, 39.9% said Ishiba should remain PM, compared to 36.9% in favour of his standing down. Approval of the cabinet rose to 27.3% in early August, up 6.5% on the previous month.

- On 21 August, the Japan Times reported that the LDP was considering postponing its internal review into the House of Councillors election. The report is now likely to be published in early September, rather than late August. The delay has been put down to Ishiba's busy diplomatic schedule in August, but as the article notes, "The extension of the review period may affect efforts by some in the party to oust Ishiba as the LDP is expected to consider whether to hold an early presidential election after the review concludes."

- The potential process of replacing Ishiba as LDP president and PM remains unclear. The LDP presidential election commission meets for a second time on 27 Aug. Japan Times: "Members are expected to discuss specific ways to confirm whether LDP lawmakers and prefectural chapters want to hold a leadership vote, but are expected to hold off on the confirmation process until after the Upper House election review is completed."

Chart 1. Betting Market Implied Probability Shigeru Ishiba Leaves Office in 2025, %

Source: Polymarket

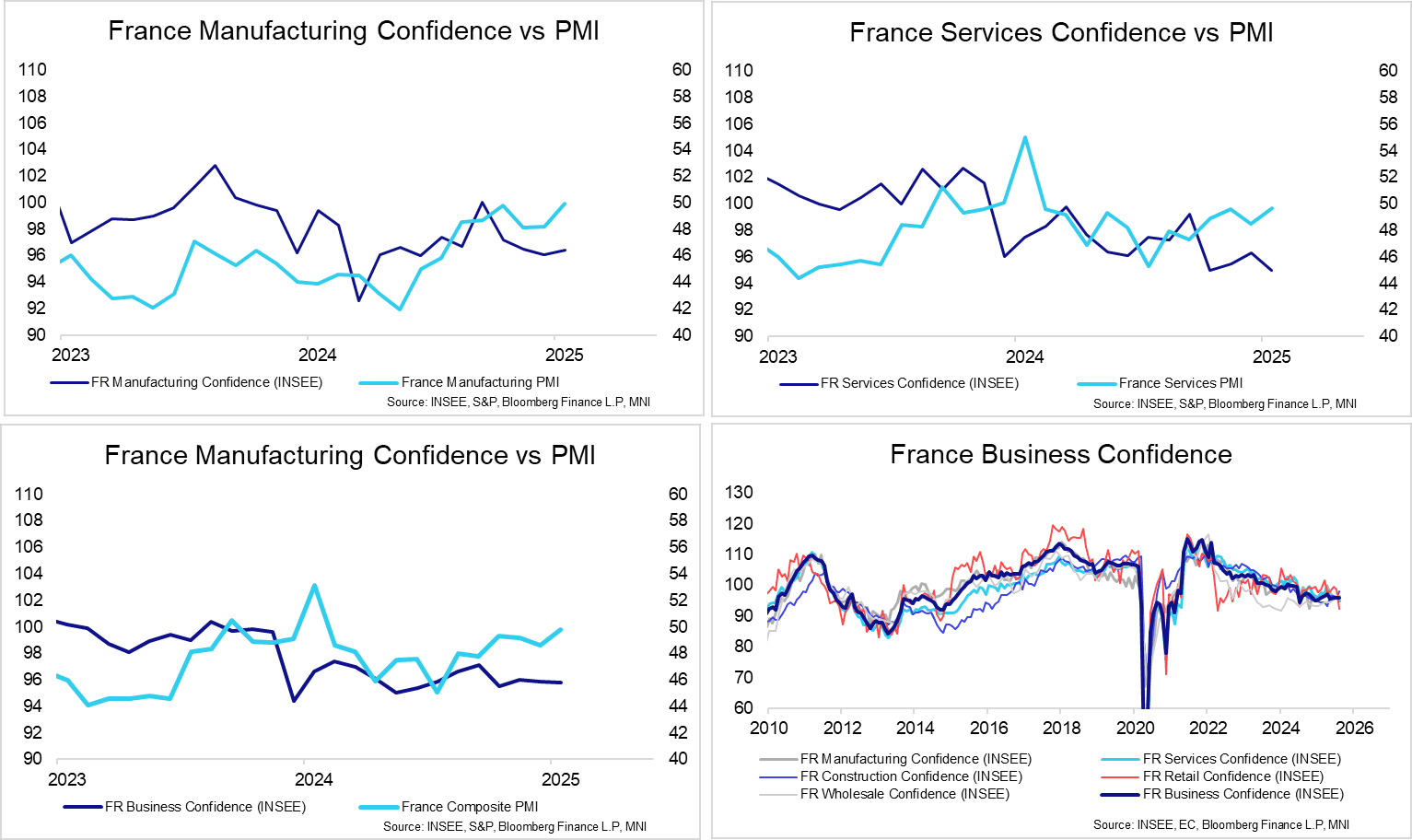

FRANCE DATA: INSEE Survey Much Less Optimistic Than PMIs

French business confidence was slightly weaker-than-expected on a rounded basis in August, printing at 95.8 (vs 95.9 prior, 97 cons). The index has been broadly stagnant since the middle of 2024, which presents some tension with the better momentum seen in PMI metrics in recent months.

- Manufacturing confidence inched up to 96.4 (vs 96.1 prior, 96 cons). We note a continued pullback in the personal production expectations component, which has fallen sharply since April.

- Services confidence fell to 95.0 (vs 96.3 prior), in contrast to the 1.2 point rise seen in the services PMI this month.

- The most notable fall was in retail confidence to 92.4 (vs 98.5 prior). This was the lowest level since April 2022. Separately, July retail sales data was also released today, with Banque de France reporting a -0.6% SA M/M fall in sales (vs -0.7% prior), and a -0.9% 3m/3m rate. There was a huge -9.9% M/M fall in new car sales in July.

- The INSEE expected employment series continued to soften, falling to 94.8 (vs 95.9 prior).

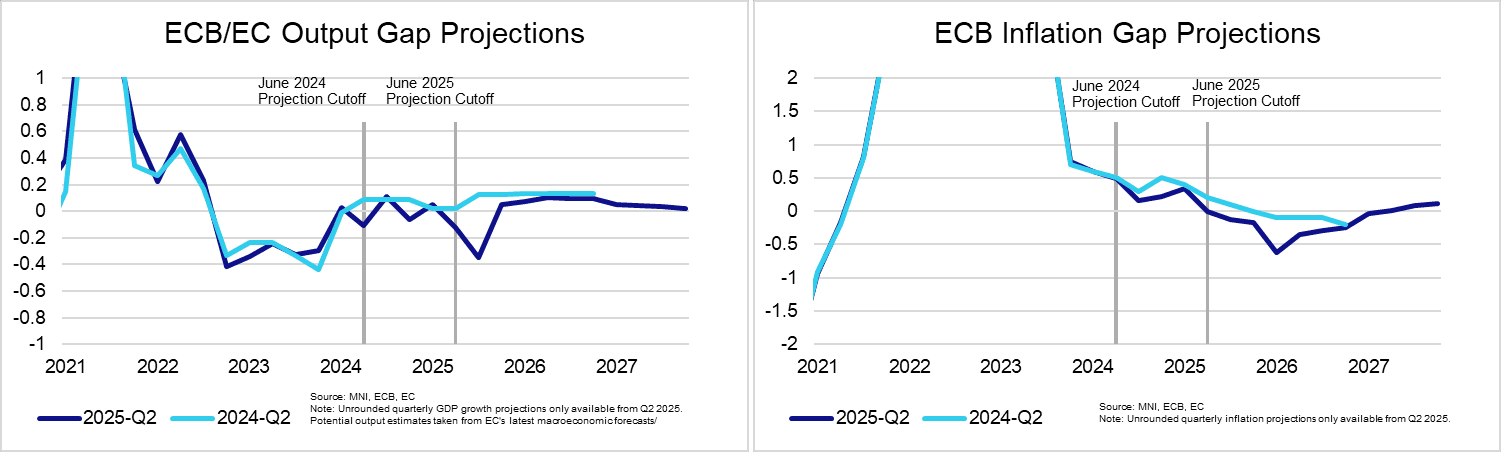

ECB: Macro Developments and GC Signals All But Confirm September Hold

This week’s signals from flash PMI data, President Lagarde’s speech and the latest Bloomberg sources piece all but ensure the ECB deposit rate will be held at 2.00% in September. Focus now turns to the August flash inflation round (starting next Friday), which alongside the final Q2 GDP report on September 5th will be the last major inputs before the ECB’s September decision.

- With the September rate decision seemingly certain, focus will be on the updated macroeconomic projections and policy statement/press conference signals.

- On Wednesday, President Lagarde played down the negative impact of the 15% baseline reciprocal tariff rate in the EU-US trade deal. She said that the tariff rate was “somewhat higher than – but still close to – the assumptions used in our baseline projections last June”, while noting that it was “well below the severe scenario for US tariffs of over 20% for euro area goods envisaged in the June projections”. This may reflect the positive impact that lower (but still elevated) trade policy uncertainty will have on the Eurozone outlook.

- Lagarde stated that “ECB staff will factor the implications of the EU-US trade deal for the euro area economy into the upcoming September projections, which will guide our decisions over the coming months”.

- The June projections saw inflation falling below target through most of 2026, before returning close to 2% by 2027. The ECB does not publicly release in-house estimates of potential output, so we have supplemented with data from the EC’s latest forecast round to calculate output gaps. That points to a degree of slack being present the economy in Q3 ’25 (as tariff front-loading unwinds), before a rebound in Q4.

- Markets still lean in favour of one more 25bp cut this cycle, but currently price less than 10bps of easing through year-end. A clear deterioration in inflation/activity data is seemingly required for another cut to be supported by the majority of the Governing Council.

FOREX: USD Index Holds Firm into Powell Appearance

- The USD Index hold firms early Friday, building on the closing gains from Thursday trade. Focus for the duration of Friday rests on the speech from Fed's Powell at the Jackson Hole Policy Symposium. With markets pricing 15-20bps of cuts for the September meeting, Powell's conviction on easing policy, or not easing policy, at today's speech could prove highly market-moving.

- GBP/USD printed a new pullback low alongside the European open, marking six consecutive sessions of lower highs and lower lows as the correction continues. Weakness in pair this week comes in the context of a bullish background condition. Recent gains resulted in a breach of 1.3589, the Jul 24 high, signaling scope for a climb towards 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1.

- The very front-end of the USD vol curve has printed very minimal risk premium headed into Friday's Powell speech - potentially signalling that markets are looking through this year's Jackson Hole symposium as the trigger to revalue vols to the year's norms.

- Indeed, one-week EUR vols printed multi-month lows of 6.2 points earlier this week - the lowest of Trump's term in office so far - mirroring realised vols, that saw very little pick-up on recent US PPI and UK CPI surprises this week. Worth noting Powell's appearance coincides with the Friday 10am NY cut.

- Outside of Powell's appearance at 1500BST/1000ET, Canadian retail sales are due, with markets expecting a rebound after the particularly poor May reading. Fed's Collins and Hammack are also set to speak. Hammack's comments moved markets yesterday, after the Cleveland Fed rep talked against a September cut.

OPTIONS: Expiries for Aug22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E700mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.90-00($1.9bln)

- USD/CAD: C$1.3685($646mln)

EQUITIES: Recent Pullback for E-Mini S&P Appears Corrective for Now

- The trend set-up in Eurostoxx 50 futures remains bullish and the contract traded to a fresh short-term cycle high earlier this week. The recent print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies are in a bull-mode position, highlighting an uptrend. Support to watch lies at 5365.06, the 50-day EMA.

- The dominant uptrend in S&P E-Minis remains intact and the latest retracement appears to be a correction - for now. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, support to watch lies at 6291.07, the 50-day EMA.

COMMODITIES: Bear Cycle in WTI Futures Intact Despite Short-Term Gains

- A bear cycle in WTI futures remains intact and short-term gains appear corrective - for now. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $63.85, the 50-day EMA.

- A bull cycle in Gold remains intact. Moving average studies are in a bull-mode position highlighting a dominant uptrend. The sideways trend that has been in place since the Apr peak appears to be a medium-term pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1400/1000 | *** | US Fed Chair Speech | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/08/2025 | 1625/1725 | BOE Bailey at Jackson Hole | ||

| 23/08/2025 | 1625/1825 | ECB Lagarde at Jackson Hole |