ECB: Macro Developments and GC Signals All But Confirm September Hold

Aug-22 11:02

This week’s signals from flash PMI data, President Lagarde’s speech and the latest Bloomberg sources piece all but ensure the ECB deposit rate will be held at 2.00% in September. Focus now turns to the August flash inflation round (starting next Friday), which alongside the final Q2 GDP report on September 5th will be the last major inputs before the ECB’s September decision.

- With the September rate decision seemingly certain, focus will be on the updated macroeconomic projections and policy statement/press conference signals.

- On Wednesday, President Lagarde played down the negative impact of the 15% baseline reciprocal tariff rate in the EU-US trade deal. She said that the tariff rate was “somewhat higher than – but still close to – the assumptions used in our baseline projections last June”, while noting that it was “well below the severe scenario for US tariffs of over 20% for euro area goods envisaged in the June projections”. This may reflect the positive impact that lower (but still elevated) trade policy uncertainty will have on the Eurozone outlook.

- Lagarde stated that “ECB staff will factor the implications of the EU-US trade deal for the euro area economy into the upcoming September projections, which will guide our decisions over the coming months”.

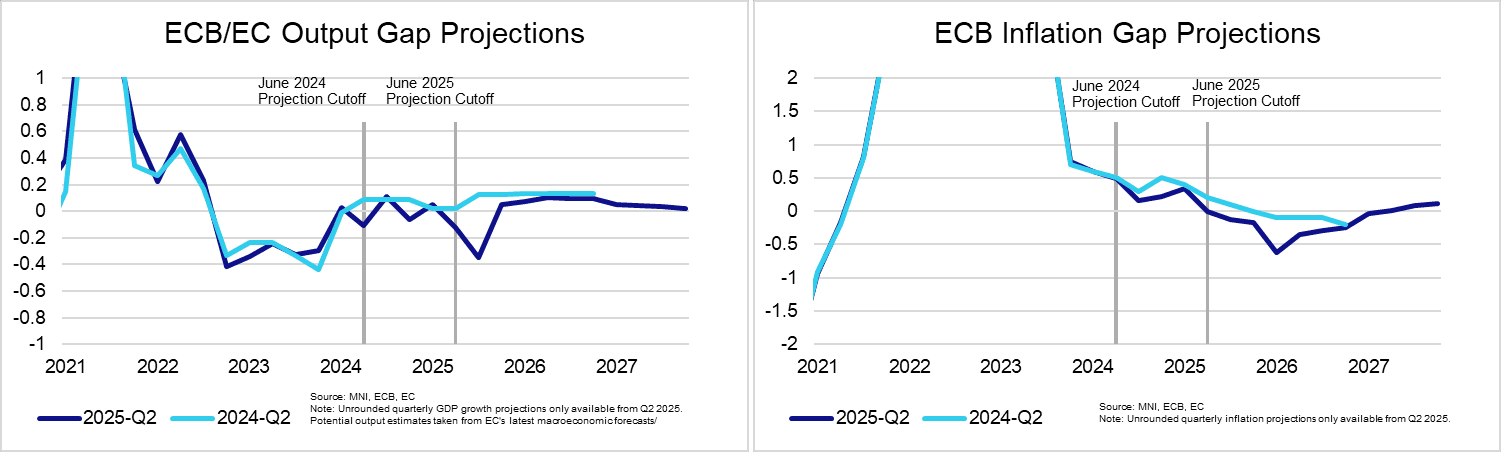

- The June projections saw inflation falling below target through most of 2026, before returning close to 2% by 2027. The ECB does not publicly release in-house estimates of potential output, so we have supplemented with data from the EC’s latest forecast round to calculate output gaps. That points to a degree of slack being present the economy in Q3 ’25 (as tariff front-loading unwinds), before a rebound in Q4.

- Markets still lean in favour of one more 25bp cut this cycle, but currently price less than 10bps of easing through year-end. A clear deterioration in inflation/activity data is seemingly required for another cut to be supported by the majority of the Governing Council.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU: EU Plans 30% Tariffs On E100bn Of Goods To US If No US Deal - Bloomberg

Jul-23 11:02

- Bloomberg reports that "The European Union plans to quickly hit the US with 30% tariffs on some €100 billion ($117 billion) worth of goods in the event of no deal and if US President Donald Trump carries through with his threat to impose that rate on most of the bloc’s exports after Aug. 1.

- As a part of a first wave of countermeasures, the EU would combine an already approved list of tariffs on €21 billion of US goods and a previously proposed list on an additional €72 billion of American products into one package, an European Commission spokesman said on Wednesday."

- The broad piece chimes with our policy team exclusive from last week (see "MNI: Support Grows For Retaliation Against US - EU Officials" - Jul 17).

- However, the following would be a notable firming in Germany stance. "Berlin would be willing to even support the activation of the EU’s anti-coercion instrument, or ACI, in a no-deal scenario, a government official said on condition of anonymity. This tool would come into play only if a deal fails to materialize."

- From our policy piece last week: "There is also the prospect of enacting the EU’s Anti-Coercion Instrument, which would apply charges to a wide range of U.S. services, though concerns over whether this would do excessive harm to Europe’s economy mean there is widespread reluctance to see it deployed."

MNI: US MBA: MARKET COMPOSITE +0.8% SA THRU JUL 18 WK

Jul-23 11:00

- MNI: US MBA: MARKET COMPOSITE +0.8% SA THRU JUL 18 WK

US TSYS: Losses Pared, 20Y Auction Watched After Steepening

Jul-23 10:44

- Treasuries are off lows although maintain a modest sell-off that has been aided by broader equity strength in Japan following a US-Japan trade deal with 15% tariffs rather than the 25% threatened. Japan PM Ishiba denied media reports that he is set to announce his resignation soon.

- A poorly received JGB auction also helps the steepening bias seen.

- Trade talks: Building on comments from Bessent yesterday, the China Ministry of Commerce says China-US will hold trade talks in Sweden Jul 27-30. Separately, EU’s Sefcovic is to talk to US Commerce Secretary Lutnick this afternoon.

- Today sees existing home sales and 20Y supplybefore Leavitt and then Trump remarks.

- Cash yields are 1-2bp higher with increases led by 10-30Y tenors.

- 2s10s at 52.6bp (+1.1bp), 5s30s at 104.1bp (+0.6bp). 5s30s peaked at 108.5bp last week after Trump-Powell firing headlines.

- TYU5 has lifted a few ticks over the past hour to 111-06+ (-06+) on modest cumulative volumes of 285k.

- It has eased to sit more firmly into yesterday’s range away from the high of 111-14+ which cleared resistance at 111-13+ (Jul 10 high). A clear break of this hurdle would highlight a stronger reversal and open 111-28 (Jul 3 high).

- Data: MBA mortgage applications (0700ET), Existing home sales Jun (1000ET)

- Coupon issuance: US Tsy $13B 20Y Bond re-open (1130ET). Last month’s 20Y was mixed, drawing a small 0.2bp tail, a higher bid-to-cover and lower indirect take-up.

- Bill issuance: US Tsy $65B 17W bills (1300ET)

- Politics: White House Press Secretary Leavitt (1300ET), Trump remarks at Executive Orders at AI Summit (1700ET)

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank

Schatz

Bobl