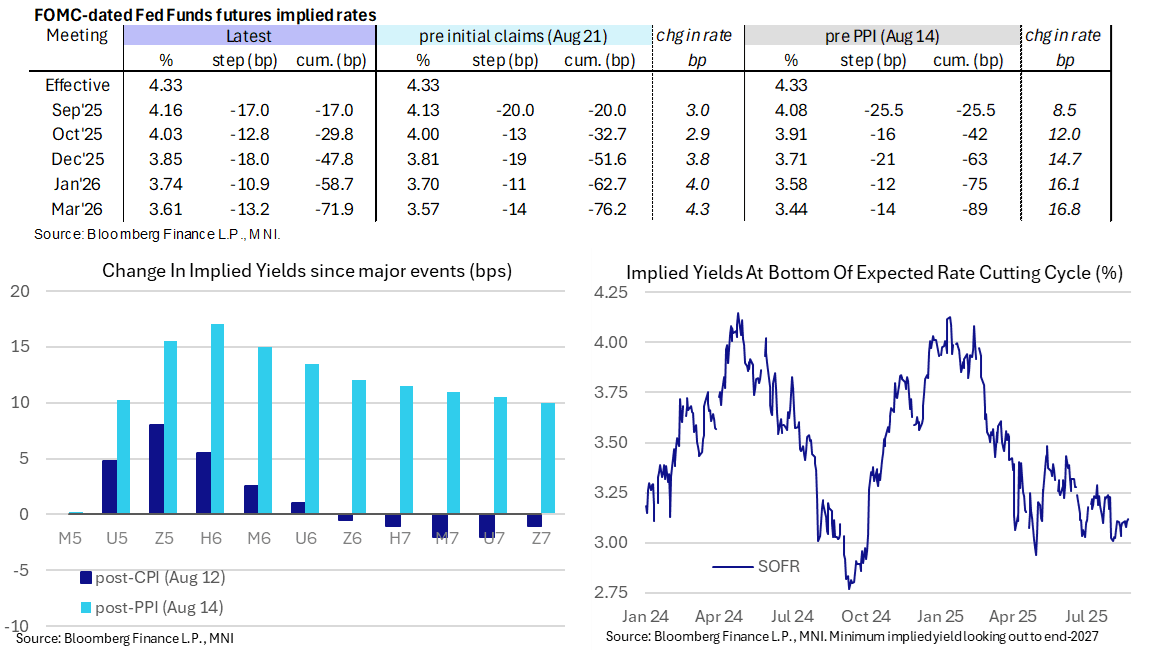

STIR: 17bp Of Fed Cuts Priced For Next Month Ahead Of Powell

Aug-22 10:25

- Near-term Fed Funds implied rates are at their most hawkish since the Aug 1 nonfarm payrolls report, aided by yesterday’s surprisingly strong flash PMIs and more patient Fedspeak.

- That path includes 17bp of cuts next month vs up to 26bp after last week’s CPI release, with Fed Chair Powell’s Jackson Hole speech firmly in focus today 1000ET.

- MNI Preview: https://media.marketnews.com/Fed_JH_Preview_Aug2025_44c9766301.pdf

- Cumulative cuts from 4.33% effective: 17bp Sep, 30bp Oct, 48bp Dec, 58.5bp Jan and 72bp Mar.

- The SOFR implied terminal yield of 3.12% (SFRH7, +1bp) last closed higher pre-payrolls, although just about keeps to its rough range of 125bp +/-5bp of cuts from current levels seen in the month to date.

- Chicago Fed’s Goolsbee (’25 voter, dove) reiterated late yesterday that Sept is a ‘live’ meeting but, for one of the more dovish FOMC members, he thought the rise in services inflation is a “dangerous” data point and that current tariffs don’t look “one and done”. Independence from political interference is critical.

- Boston Fed’s Collins (’25 voter) meanwhile said a rate cut may be appropriate soon if the labor outlook worsens and that the Fed can’t wait for full clarity on inflation to consider cuts. She had advocated for an “actively patient” policy approach prior to the July FOMC meeting.

- Collins speaks again today on Bloomberg TV at 0900ET whilst Hammack (’26 voter, hawk) follows Powell at 1130ET on CNBC after saying yesterday she doesn’t see the case for a September cut as data stand.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Bull Cycle In Gold Remains In Play

Jul-23 10:24

- On the commodity front, a bull cycle in Gold that started Jun 30 remains intact, and this week's gains mark an extension of the recovery. $3395.1, the Jun 23 high, has been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that moving average studies are in a bull-mode position highlighting a dominant uptrend. The bear trigger is $3248.7, the Jun 30 low. An initial firm support to watch is 3282.8, the Jul 9 low.

- In the oil space, a bearish theme in WTI remains intact and the recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.68. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. Initial resistance to monitor is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.

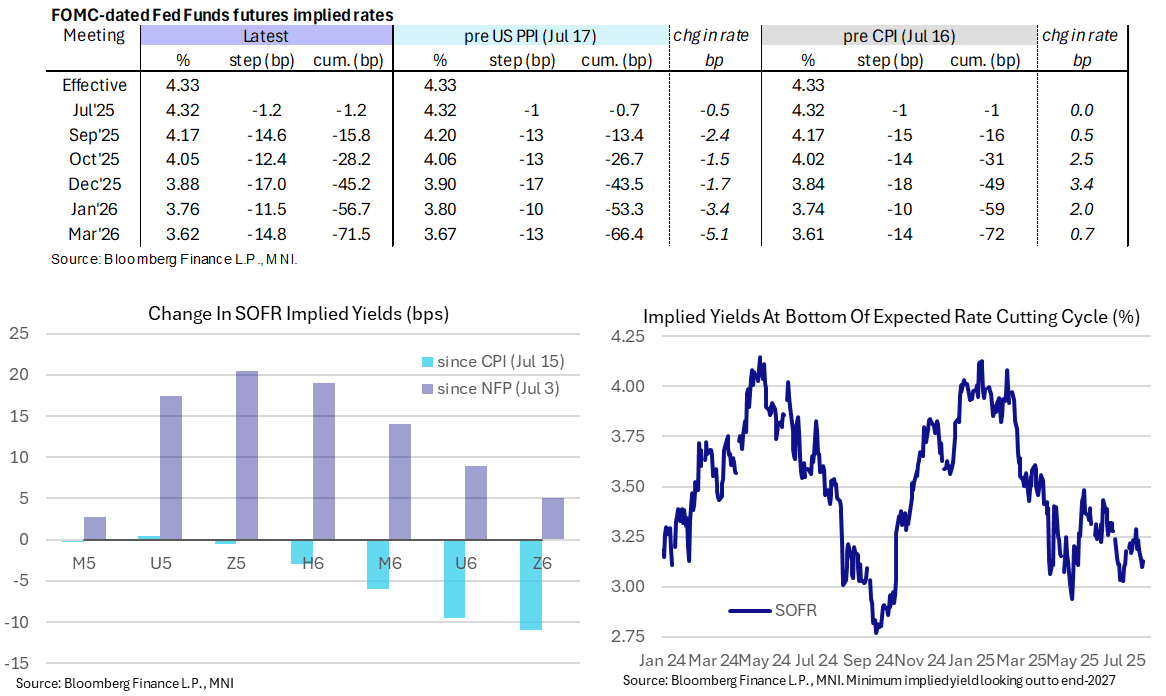

STIR: US Rate Path Slightly More Hawkish On Broader Equity Strength

Jul-23 10:23

- Fed Funds implied rates have drifted higher with broader risk-on emanating from Japan following a US-Japan trade deal with 15% tariffs rather than the 25% threatened.

- The Dec 2025 rate is 1bp higher on the day but remains within narrow range seen since Friday.

- Cumulative cuts from 4.33% effective: 1bp Jul, 16bp Sep, 28bp Oct, 45bp Dec, 56.5bp Jan, 71.5bp Mar.

- SOFR implied terminal yields are 3bp higher on the day at 3.13% (SFRZ6), still close to implying five more cuts for the cycle from current levels.

- Today sees existing home sales, watched amidst broad-based housing market weakness. Trade deal progress remains in focus and we see comments from the White House Press Briefing at 1300ET before President Trump remarks whilst sign Executive Orders at an AI Summit at 1700ET.

LOOK AHEAD: Wednesday Data Calendar: MBA Mtg Apps, Exist Home Sales, 20Y Reopen

Jul-23 10:23

- US Data/Speaker Calendar (prior, estimate)

- 07/23 0700 MBA Mortgage Applications (-10.0%, --)

- 07/23 1000 Existing Home Sales (4.03M, 4.0M), MoM (0.8%, -0.7%)

- 07/23 1130 US Tsy $65B 17W bills

- 07/23 1300 US Tsy $13B 20Y Bond re-open

- Source: Bloomberg Finance L.P. / MNI