MNI US MARKETS ANALYSIS - Mkts Gear for Consequential NFP

Highlights:

- Markets gear for consequential NFP print; whisper number has drifted lower

- Treasuries hold at weekly highs, USD softer as payrolls expected to signal slowing economy

- Second Trump-Putin meeting could be organised "quickly", according to Russia media

US TSYS: Mid-Week Rally Consolidated, Awaiting A Key Payrolls Report

- Treasuries consolidate yesterday’s rally, maintaining narrow ranges ahead of a highly anticipated payrolls report for August.

- The NFP report dominates the session before plenty of occasions to hear President Trump’s reaction to it after last month’s large negative revisions prompted his firing of BLS Commissioner McEntarfer (with EJ Antoni subsequently nominated).

- There’s no Fedspeak scheduled for after the event but there could be appearances on the last day before the FOMC blackout ahead of the 25bp cut currently priced for the Sep 17 decision.

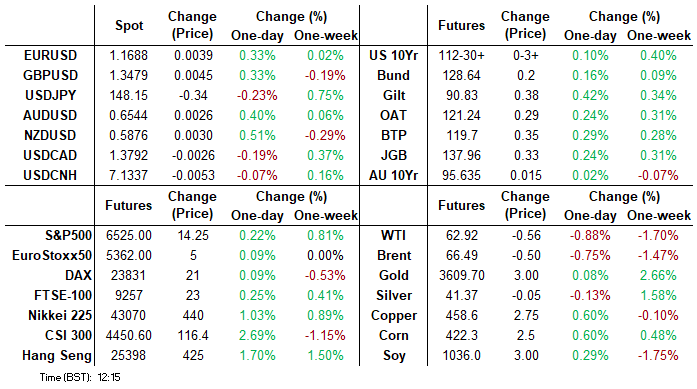

- Cash yields are between 0.4-0.9bp lower on the day.

- Curves hold the shift off recent steeps, including 5s30s at 121.3bp off mid-week multi-year highs of 124.6bps.

- TYZ5 trades at 112-30+ (+ 03+) having earlier touched 113-00 for a fresh short-term cycle high, reinforcing the bullish condition, on unsurprisingly mild volumes of 235k ahead of a major risk event.

- The latest moves pave the way for an extension towards 113-06 (Fibo projection) whilst support is seen at 112-04 (20-day EMA).

- Data: Payrolls Aug (0830ET)

- Politics: Trump participates in Ambassador Credentialing Ceremony (1200ET), Trump signs Executive Orders (1400ET), Trump makes an announcement (1600ET)

- Cook lawsuit: Court filings earlier this week suggest that Cook could reply to the government's latest arguments (made yesterday) today. The judge will at some point determine whether to grant Cook's request for a temporary restraining order that would keep her in her position going into the next FOMC meeting, while the case is ongoing. Both sides are seeking a quick resolution, so we may have an answer by next week if not earlier

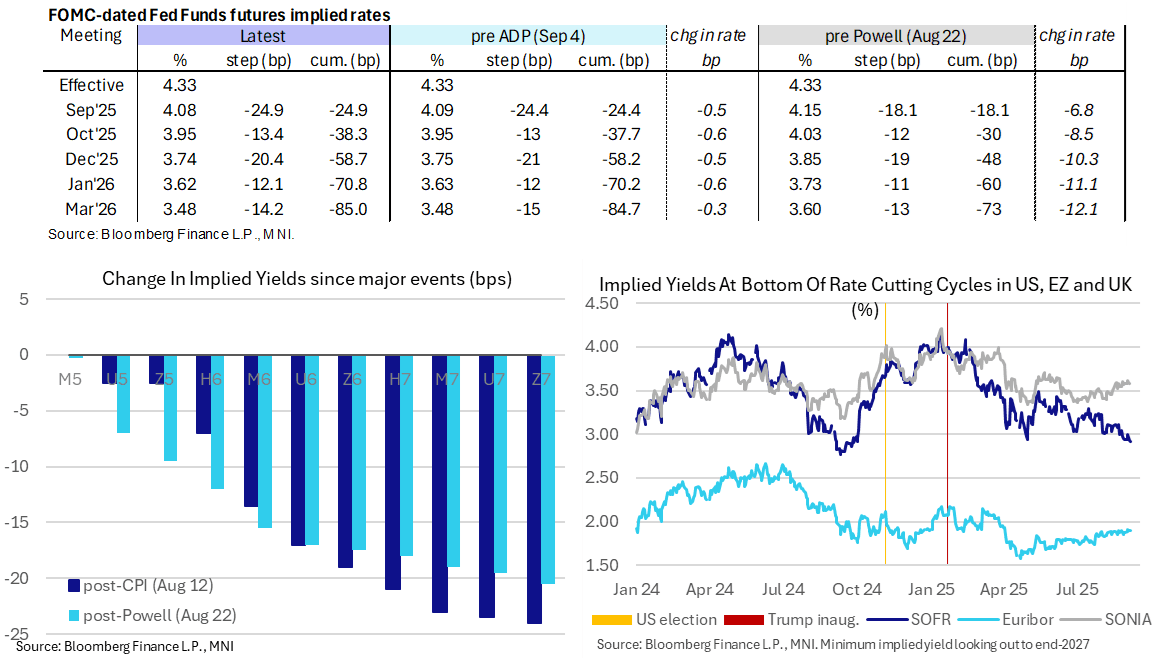

STIR: Fed Terminal Rate Expectations At Fresh Recent Lows Ahead Of Payrolls

- Fed Funds implied rates are unchanged overnight for Sept and Oct meeting but have lifted 1.5bps for Dec-Mar meetings ahead of payrolls.

- Cumulative cuts from 4.33% effective: 25bp Sep, 38.5bp Oct, 58.5bp Dec, 71bp Jan and 85bp Mar.

- SOFR futures echo this Z5/H6 modest sell-of (1 tick lower) whilst the curve sits modestly flatter with late 2026/early 2027 contracts 0.5-1 higher.

- The SOFR implied terminal yield of 2.92% (SFRH7) is another 1bp lower after yesterday’s close was the lowest since Oct 2024. It points to ~140bp of cuts from current levels.

- Ahead of today’s payrolls report (MNI preview here: https://mni.marketnews.com/3I3oEii), Chicago Fed’s Goolsbee (’25 voter, dove) said yesterday he will take the upcoming August payroll figures with a grain or salt. He'll instead focus more closely on the jobless rate, something we have heard increasingly from FOMC member. He still has not yet made up his mind on whether to support cutting interest rates this month, and is still balancing out growing concern about the labor markets with lingering worries about persistent inflation.

- There is no Fedspeak scheduled today although there could be surprises appearances after payrolls on the last day before the FOMC blackout starts.

- Major releases still to come in the blackout before the Sep 16-17 FOMC meeting include the preliminary benchmark revision on Sep 9, PPI on Sep 10 and CPI on Sep 11.

STIR: Net Long Setting In Most Futures On Thursday

OI data suggests that net long setting dominated in most SOFR futures for a second consecutive day on Thursday, with mixed impetus from data releases and wider focus on today’s NFP release. Instances of net short cover were fairly isolated.

| 04-Sep-25 | 03-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,164,180 | 1,163,886 | +294 | Whites | +16,273 |

SFRU5 | 1,397,068 | 1,416,701 | -19,633 | Reds | +44,959 |

SFRZ5 | 1,595,252 | 1,559,948 | +35,304 | Greens | +12,367 |

SFRH6 | 1,134,011 | 1,133,703 | +308 | Blues | +21,269 |

SFRM6 | 958,654 | 936,986 | +21,668 |

|

|

SFRU6 | 900,581 | 895,798 | +4,783 |

|

|

SFRZ6 | 998,250 | 975,778 | +22,472 |

|

|

SFRH7 | 723,017 | 726,981 | -3,964 |

|

|

SFRM7 | 811,235 | 810,440 | +795 |

|

|

SFRU7 | 651,361 | 640,704 | +10,657 |

|

|

SFRZ7 | 641,426 | 641,796 | -370 |

|

|

SFRH8 | 419,141 | 417,856 | +1,285 |

|

|

SFRM8 | 338,339 | 333,277 | +5,062 |

|

|

SFRU8 | 231,165 | 223,823 | +7,342 |

|

|

SFRZ8 | 253,648 | 245,408 | +8,240 |

|

|

SFRH9 | 164,928 | 164,303 | +625 |

|

|

SECURITY: Second Trump-Putin Meeting Could Be 'Quickly Organised' - Kremlin

Kremlin Spokesperson Dmitri Peskov told Russian outlet Argumenty i Fakty that a second meeting between Russian President Vladimir Putin and US President Donald Trump could take place in the near future, with “working contacts" taking place "all the time.”

- Peskov: "I have no doubt that if the presidents consider it necessary, their meeting can be organized very quickly. Just as the meeting in Alaska was quickly organized."

- The comments came after Trump spoke with European leaders yesterday to discuss the outcome of a meeting of the so-called ‘coalition of the willing’ group of Ukraine-backers in Paris yesterday. The New York Times notes that more than 30 heads of state and government attended the meeting, but few details emerged about exactly how the European nations would help Ukraine or how the US would be involved.

- A White House official said Trump pushed European leaders to stop buying Russian oil that he said allows Moscow’s military to sustain the conflict, per Politico. The official added, “[Trump] also emphasized that European leaders must place economic pressure on China for funding Russia’s war efforts.”

- French President Emmanuel Macron told reporters that, without a peace deal, Russia would face international sanctions, including from the US. But, as the Times points out, “Trump has threatened sanctions before without following through.”

- Politico notes that Trump’s call for economic pressure on China, “may have evoked eyerolls among some European leaders", as Trump has deferred secondary sanctions on Beijing, similar to those levied on India.

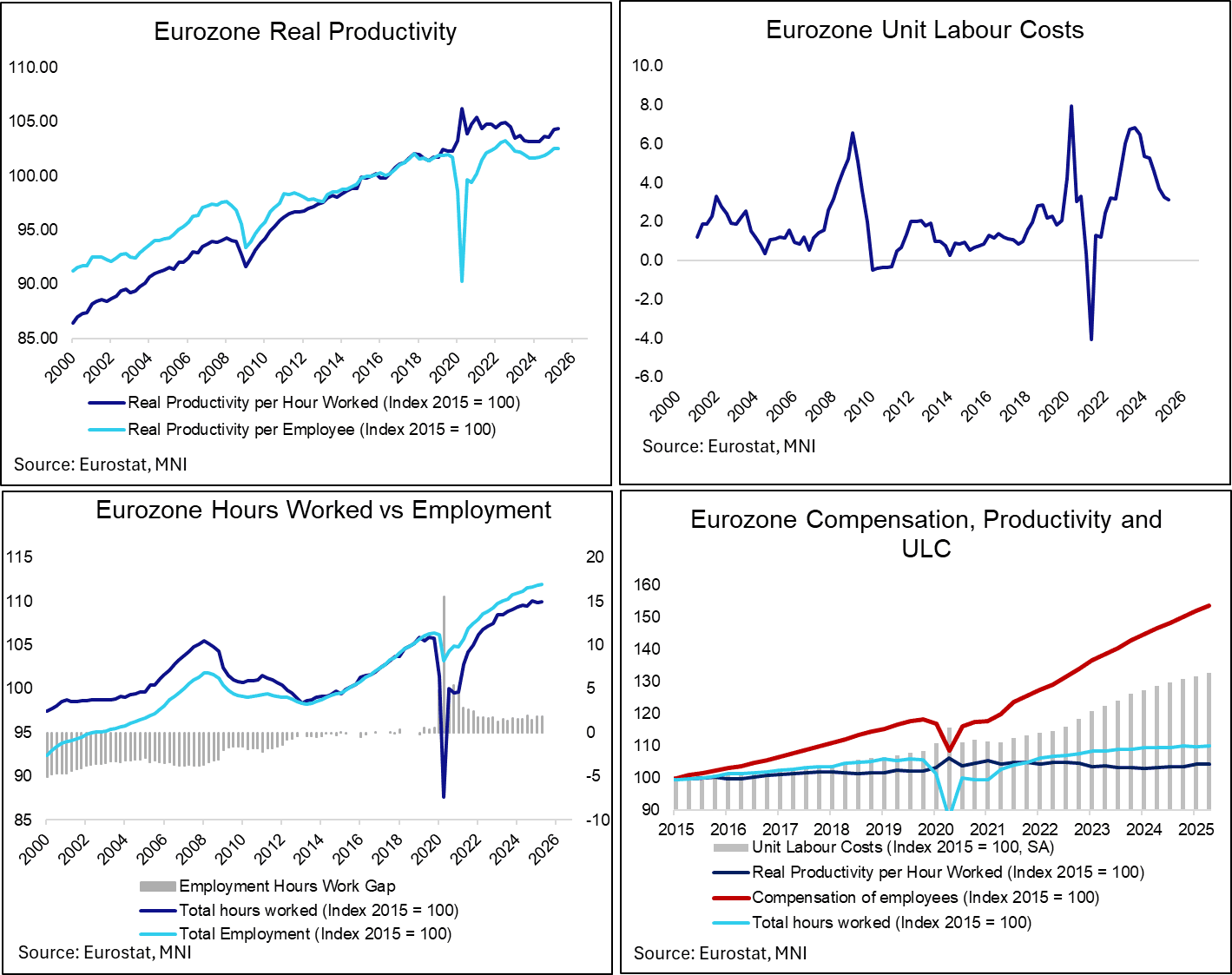

EUROZONE DATA: ULC Growth Still Easing, But At A Slower Clip Than ECB Assumed

Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB’s 2.9% projection made in June, seemingly driven the smaller-than-expected deceleration in total compensation per employee growth (noted earlier: 3.9% Y/Y vs 4.0% prior, 3.4% ECB). While a declaration in unit labour cost growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- With the Eurozone unemployment rate currently at an all-time low of 6.2%, some analysts have been cognisant of the risk that growing labour market slack could become evident in hours worked, rather than employment, figures.

- Eurozone hours worked rose 0.4% in Q2, down from 0.5% last quarter for the lowest rate since Q1 2021. That comes alongside a 0.6% Y/Y rise in total employment (down from 0.7% in Q1). While hours worked have grown at a slightly softer clip than total employment in recent quarters, there’s not yet clear evidence that slack is meaningfully increasing through the hours worked channel yet.

- Real productivity per hour worked was flat Q/Q but still up 1.1% Y/Y for the second consecutive quarter. Real productivity per employee was also steady at 0.8% Y/Y. While productivity is undergoing a gradual cyclical recovery, it remains below its pre-covid trend. Further improvements will be needed to increase the Eurozone’s potential growth rate going forward.

FOREX: USD Weaker into NFP, At Risk of Correction on Stronger Print

- The USD trades weaker through to the NY crossover, with markets continuing to position for signals of a soft labour market and slowing economy in today's NFP print. Renewed USD sales through the European morning has the USD Index at new daily lows, despite generally light volumes across the board. The downtick in the dollar has the USD Index trading either side of the 50-dma, and weakness through 97.993 support would open 97.818 intraday: the 23.6% retracement for the downleg posted off the Aug27 high.

- AUD's new daily highs has the price narrowing in on resistance defined by the 15-min candle chart: 0.6550 marks the downtrendline drawn off the Sep 1st Europe AM high - touched twice since over the past 4 sessions. AUD and NZD are the firmest performers in G10 after the APAC session made light work in erasing a weaker Thursday close for NZD/USD.

- Naturally, the focus shifts to payrolls data in light of the recent string of soft job market data in the US: JOLTS, IJC and the employment components of ISM services & manufacturing all came in weaker-than-expected), which is helping weigh on the whisper number for today's print, down to 75k (inline with consensus) after holding between 80-85k just a few days ago.

- Alongside the US jobs print, Canada's August employment data also crosses, at which the unemployment rate is seen rising to 7.0%, matching the post-COVID high in the process. Into the data, the bull cycle in USDCAD that started mid-June remains in play. Near term, the recovery from the Aug 29 low highlights a potential early reversal signal and if correct, the end of the corrective pullback between Aug 22 - 29.

FOREX: USD Gears for Most Consequential NFP of Trump's Term

The USD Index is holding at yesterday's lows in expectedly light trade so far, as markets gear for today's payrolls print. USD markets have eased of the week's earlier highs on continued softness in labour market data (JOLTS, IJC and the employment components of ISM services & manufacturing all came in weaker-than-expected), which is helping weigh on the whisper number for today's print, down to 75k (inline with consensus) after holding between 80-85k at the beginning of the week.

- Options markets help us quantify the market risk into today's print, and the vol premium added is sizeable: an average 3.9 point vol premium across G10 FX is close to double that seen for the July, June and May NFP - making the August print potentially the most consequential since January.

- Markets maintain the net short USD position that carried over the summer - but investors are seemingly unwilling to engage in more convictive downside despite the growing risks to Fed independence and firmer pricing for Fed easing into year-end. This may be down to growing fiscal and political risks in the UK and Europe - in which case, a fade of these risks could provide fresh impetus to push the USD lower from here should today's NFP print endorse current Fed pricing.

OPTIONS: Sizeable Strikes Could Help Define Post-Payrolls Range

More sizeable options strikes rolling off at today's post-payrolls NY cut include sizeable expiries at 1.16 and 1.1740-50 in EURUSD, 146.95-00 in USDJPY and layered between 0.64 - 0.65 in AUDUSD that could help define the range after data volatility.

Given recent intraday vol in JPY, no surprise to see USD/JPY isolated by options markets this week - overnight vols of ~18.5 points blows out the break-even on a USDJPY straddle expiring today to just over 100 pips, double that of the same option struck earlier in the week.

- EUR/USD: $1.1600(E2.1bln), $1.1700(E964mln), $1.1740-50(E1.6bln), $1.1775-80(E1.2bln)

- USD/JPY: Y146.95-00($1.3bln), Y147.40-50($957mln), Y148.85-00($679mln)

- AUD/USD: $0.6400(A$1.1bln), $0.6500-10(A$1.5bln), $0.6600(A$1.0bln)

- USD/CAD: C$1.3720-30($917mln), C$1.3850-60($1.1bln)

EQUITIES: Latest Pullback for E-Mini S&P Appears to Be Only a Shallow Correction

- The primary trend set-up in Eurostoxx 50 futures is bullish, however a corrective bear cycle remains in play. Recent weakness resulted in a breach of 5370.73, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5384.25, the 20-day EMA. A clear break of it would be bullish.

- A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract has traded to a fresh cycle high, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6447.06, the 20-day EMA.

COMMODITIES: Recent Move Lower for WTI Futures Signals End of Corrective Phase

- A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. Tuesday’s move down highlights a possible early reversal signal and the end of the corrective phase. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold is unchanged, it remains in a clear bull cycle and trades closer to its recent highs. This week’s gains resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3600.00. Initial firm support lies at $3424.5, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |