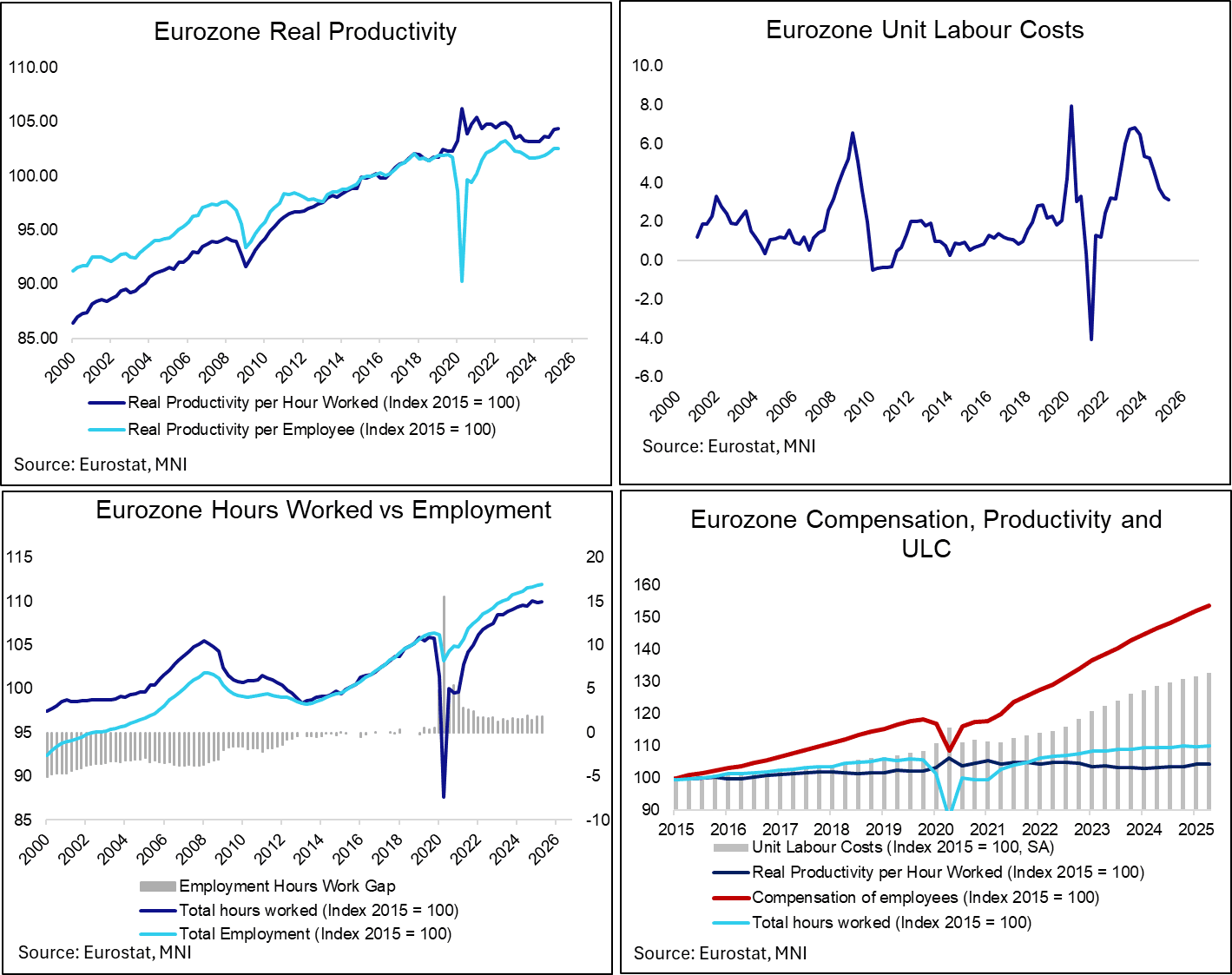

EUROZONE DATA: ULC Growth Still Easing, But At A Slower Clip Than ECB Assumed

Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB’s 2.9% projection made in June, seemingly driven the smaller-than-expected deceleration in total compensation per employee growth (noted earlier: 3.9% Y/Y vs 4.0% prior, 3.4% ECB). While a declaration in unit labour cost growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- With the Eurozone unemployment rate currently at an all-time low of 6.2%, some analysts have been cognisant of the risk that growing labour market slack could become evident in hours worked, rather than employment, figures.

- Eurozone hours worked rose 0.4% in Q2, down from 0.5% last quarter for the lowest rate since Q1 2021. That comes alongside a 0.6% Y/Y rise in total employment (down from 0.7% in Q1). While hours worked have grown at a slightly softer clip than total employment in recent quarters, there’s not yet clear evidence that slack is meaningfully increasing through the hours worked channel yet.

- Real productivity per hour worked was flat Q/Q but still up 1.1% Y/Y for the second consecutive quarter. Real productivity per employee was also steady at 0.8% Y/Y. While productivity is undergoing a gradual cyclical recovery, it remains below its pre-covid trend. Further improvements will be needed to increase the Eurozone’s potential growth rate going forward.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Goldman Note Risk Of Further Curve Steepening

Goldman Sachs write “the shift in Fed cut pricing has compressed the gap between the market and our economists' expected Fed path. Despite the abruptness of last Friday's rally, we think risk/reward favours remaining long the front end in the U.S.. The timing and pace of any policy adjustment are key to dictating the curve shape, with the sustained outperformance of 5s at risk in the event of more rapid cuts”.

- They go on to note that “while the long end of the curve is somewhat cheap versus fundamentals, we nonetheless expect that evidence of further economic weakness would justify stronger front-end outperformance and sharper curve steepening”.

- Goldman’s “year-end forecasts of 3.45% 2-Year and 4.20% 10-Year yields imply steepening of the spot curve and relatively stable longer term rates”.

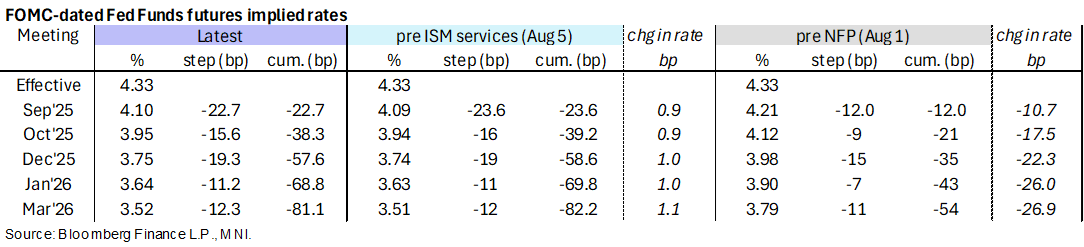

STIR: Slightly Less Dovish, More Post-FOMC (and NFP) Fedspeak Later

- Fed Funds implied rates are up to 1.5bp higher for meetings out to Mar 2026, hovering close to their highest since the Friday’s NFP and ISM mfg reports had been digested but still holding a strong dovish shift on net.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 38.5bp Oct, 57.5bp Dec, 69bp Jan and 81bp Mar.

- The SOFR implied terminal yield of 3.055% (SFRH7, +2.5bp) continues its slow rise off Monday’s lowest close since late April, but still broadly prices five cuts from current levels.

- Today sees a particularly thin data docket although there is a continuation of post-FOMC and NFP Fedspeak later on. Bostic and Hammack took a measured tone on Friday, Daly a little more dovish on Monday.

- 1400ET – Gov. Cook (permanent voter) and Collins (’25 voter) in a panel event (no text). We last heard from Cook back in early June when she warned the Fed must be open to all possibilities regarding rates including explicit mention of rate hikes. Collins pushed an “actively patient” approach to monetary policy as remaining appropriate when last speaking in mid-July.

- 1610ET – Daly (non-voter) speaks at Anchorage Economic Summit (text + Q&A). She told Reuters late Monday that she still sees two rate cuts this year as “an appropriate amount of recalibration”. “We of course could do fewer than two if inflation picks up and spills over or if the labor market springs back”. However, “I think the more likely thing is that we might have to do more than two...we also should be prepared in my judgment to do more if the labor market looks to be entering that period of weakness and we still haven’t seen spillovers to inflation”

- Trump yesterday on deliberations over Gov. Kugler’s board position: “I’ll be making that decision before the end of the week. We’ll either decide on one for permanence or the four-month period — the term. You know, there’s a term of about a number of months.”

LOOK AHEAD: Wednesday Data Calendar: 10Y Note Sale, Fed Speak

- US Data/Speaker Calendar (prior, estimate)

- 08/06 0700 MBA Mortgage Applications (-3.8%, --)

- 08/06 1130 US Tsy $65B 17W bill auction

- 08/06 1300 US Tsy $42B 10Y Note auction (91282CNT4)

- 08/06 1400 Fed Gov Cook & Boston Fed Collins panel event (no text, Q&A)

- 08/06 1610 SF Fed Daly moderated discussion eco-summit

- Source: Bloomberg Finance L.P. / MNI