STIR: Fed Terminal Rate Expectations At Fresh Recent Lows Ahead Of Payrolls

Sep-05 2025 10:33

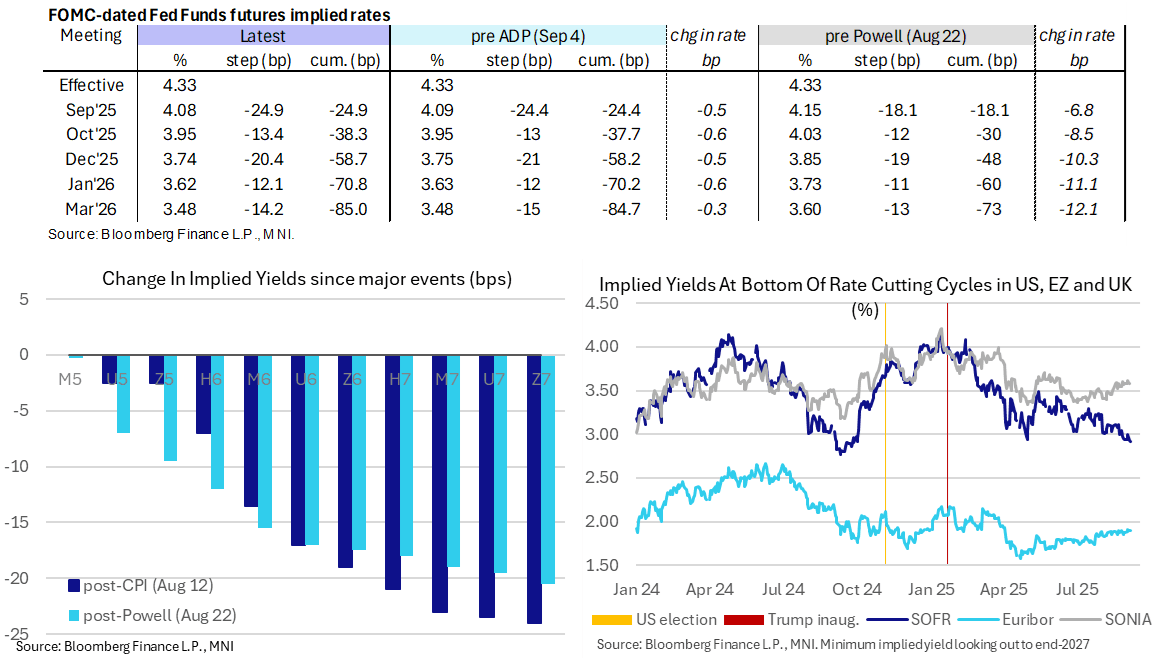

- Fed Funds implied rates are unchanged overnight for Sept and Oct meeting but have lifted 1.5bps for Dec-Mar meetings ahead of payrolls.

- Cumulative cuts from 4.33% effective: 25bp Sep, 38.5bp Oct, 58.5bp Dec, 71bp Jan and 85bp Mar.

- SOFR futures echo this Z5/H6 modest sell-of (1 tick lower) whilst the curve sits modestly flatter with late 2026/early 2027 contracts 0.5-1 higher.

- The SOFR implied terminal yield of 2.92% (SFRH7) is another 1bp lower after yesterday’s close was the lowest since Oct 2024. It points to ~140bp of cuts from current levels.

- Ahead of today’s payrolls report (MNI preview here: https://mni.marketnews.com/3I3oEii), Chicago Fed’s Goolsbee (’25 voter, dove) said yesterday he will take the upcoming August payroll figures with a grain or salt. He'll instead focus more closely on the jobless rate, something we have heard increasingly from FOMC member. He still has not yet made up his mind on whether to support cutting interest rates this month, and is still balancing out growing concern about the labor markets with lingering worries about persistent inflation.

- There is no Fedspeak scheduled today although there could be surprises appearances after payrolls on the last day before the FOMC blackout starts.

- Major releases still to come in the blackout before the Sep 16-17 FOMC meeting include the preliminary benchmark revision on Sep 9, PPI on Sep 10 and CPI on Sep 11.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Wednesday Data Calendar: 10Y Note Sale, Fed Speak

Aug-06 2025 10:33

- US Data/Speaker Calendar (prior, estimate)

- 08/06 0700 MBA Mortgage Applications (-3.8%, --)

- 08/06 1130 US Tsy $65B 17W bill auction

- 08/06 1300 US Tsy $42B 10Y Note auction (91282CNT4)

- 08/06 1400 Fed Gov Cook & Boston Fed Collins panel event (no text, Q&A)

- 08/06 1610 SF Fed Daly moderated discussion eco-summit

- Source: Bloomberg Finance L.P. / MNI

CHF: BofA Think Markets Complacent, Weaker Franc If Tariff Levels Remain

Aug-06 2025 10:19

Following the US's announcement of 39% tariffs on Swiss imports, Bank of America think "the options available to the Swiss appear limited and it is unclear whether these will appease the U.S." as opposed to a complacent-appearing market which believes "that a deal will be struck in line with precedent of other negotiations".

- This leads them to conclude that if announced tariff levels would in fact remain in play, they "doubt that [an SNB] move into negative territory is the solution [...]. The more impactful policy lever would be to absorb the tariff rate via a weaker currency. This has been a path trodden by other economies in the past notably China."

- "SNB itself has history of attempting to weaken the currency via the EUR/CHF 1.20 floor. The net result in our view is that 39% tariff which cannot be negotiated downwards would lead to a structurally weaker currency, in large part driven by SNB action."

EUR: Volume Spike Tips EUR/USD Through Post-NFP High

Aug-06 2025 10:16

EUR edges to the best levels of the day into the NY crossover, with a sizeable upturn in EUR futures volumes at 1107BST/0607ET the likely driver. No notable newsflow or headlines crossing to trigger the move, and cross-market prices also relatively subdued.

- Just shy of $200mln notional traded on the initial EUR rally - helping push EUR/USD spot now through the 1.1600 handle for a new weekly high. Break of resistance into the post-NFP high at 1.1597 also helping here - and spot now within range of a sizeable option expiry (€1.1bln) rolling off at 1.1600 today.

- This tips EUR/JPY to new daily highs - but progress above 171.85 is needed before the late July highs can come into play.