MNI US MARKETS ANALYSIS - Markets Anticipate BOE Cut

Highlights:

- Markets await anticipated 25bps BOE rate cut

- Putin-Trump face-to-face meeting could come as soon as next week

- Weekly jobless claims in focus, Trump to make remarks after the equity close

US TSYS: Mildly Firmer Ahead Of Jobless Claims Latest Test Of Labor Strength

- Treasuries are mildly firmer as they keep within yesterday’s range on light cumulative volumes so far, with jobless claims, 30Y supply and Trump remarks on the docket.

- Domestic data focus is likely on jobless claims after initial claims in particular have been surprisingly robust in recent weeks, especially in contrast to Friday’s soft payrolls report.

- There could also be spillover from the BoE decision at 0700ET.

- Cash yields are between 0-1bp lower on the day.

- TYU5 trades at 112-06 (-01+) on thin cumulative volumes of 220k, having kept without yesterday’s range throughout.

- It holds a modest back further from what is now latest resistance at 112-15+ from the Aug4/5 overnight high (after which lies 112-23, May 1 high)). Support is some way lower at 110-19+ (Jul 24 low).

- Data: Weekly jobless claims (0830ET), ULCs/Productivity (Q2 prelim), Wholesale trade sales/inventories Jun/Jun F (1000ET), NY Fed inflation expectations Jul (1100ET) and Consumer credit Jun (1500ET)

- Fedspeak: Bostic (1000ET) – see STIR bullet

- Coupon issuance: US Tsy to sell $25B 30Y - 912810UM8 (1300ET). Yesterday’s 10Y tailed by 1bp along with a sizeable decline in bid-to-cover from 2.61x to 2.35x for its lowest since Aug 2024.

- Bill issuance: US Tsy to sell $100B 4-W and $85B 8-W bills (1130ET)

- Politics: Trump signs executive orders (1200ET) and later delivers remarks (1600ET). Wires report the Putin-Trump meeting is likely to take place next week, where ceasefire demands on Moscow will undoubtedly be a topic of conversation. Friday’s deadline for Russia has presumably been paused - however secondary sanctions on India and other select countries are expected to proceed. We could hear more on this today.

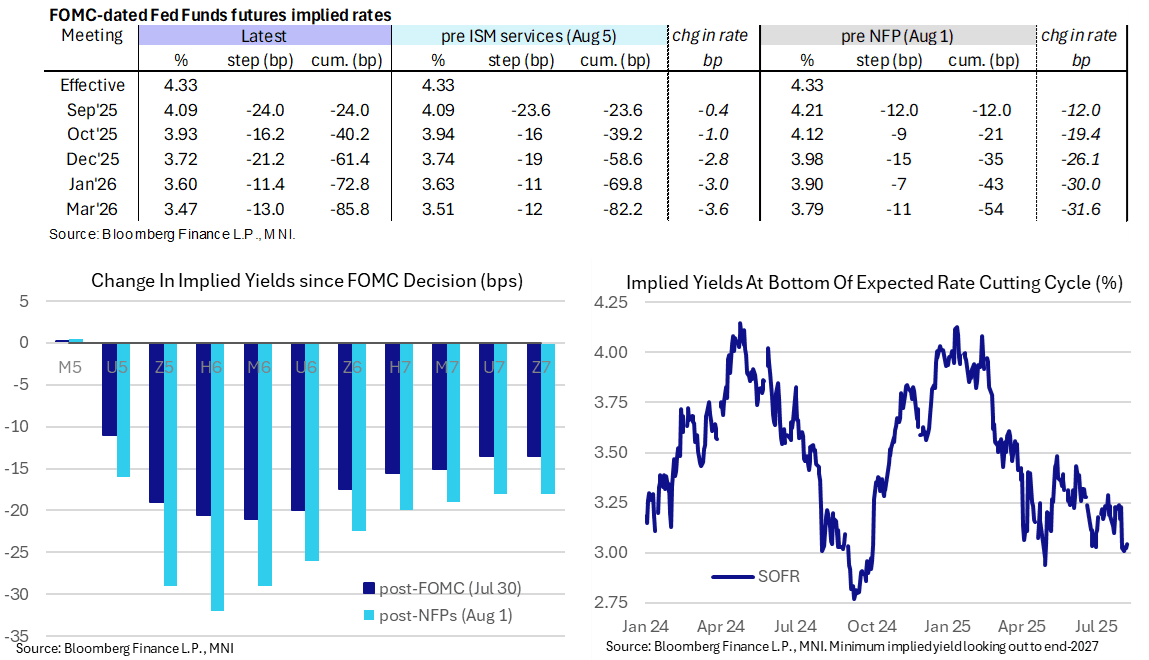

STIR: Fed Rates Within Post-NFP Range, 61.5bp Cuts To End-2025

- Fed Funds implied rates are up to 1bp lower overnight for meetings out to Mar 2026 as they keep to post-NFP ranges ahead of data focus on weekly jobless claims.

- The 61.5bp of cuts to year-end sits within the 56-64bp seen this week.

- Cumulative cuts from 4.33% effective: 24bp Sep, 40bp Oct, 61.5bp Dec, 73bp Jan and 85.5bp Mar.

- The SOFR implied terminal yield of 3.045% (SFRH7) is 2bp higher on the day, holding close to recent levels with a little more than five cuts priced from current levels.

- Atlanta Fed’s Bostic (non-voter) speaks on monetary policy today at 1000ET (no text). He was one of the first to speak after Friday’s NFP report, noting the significant revisions but warning that the Fed still needs to determine what the trend of hiring will be. He hasn’t changed his view on rates and still expects one cut this year.

- Yesterday, Gov. Cook (permanent voter) called the July jobs report “concerning,” as “these revisions are somewhat typical of turning points”.

- Cook added that business leaders report spending significant amounts of time managing uncertainty – “This is deadweight loss”. Boston Fed’s Collins (’25 voter) agreed, saying an “uncertainty tax” was “top of mind across a wide range of different industries.”

- Trump yesterday on latest Fed Governor/Chair deliberations: “We’re probably going to go with the temp and then a permanent. I think the temp is going to be named, I’d say, over the next two, three days, and then we’re going to go permanent.”

US TSY FUTURES: Mix Of Positioning Swings During Wednesday's Twist Steepening

OI data points to a mix of net long setting (TU), short setting (TY, US & WN) and long cover (UXY) as the curve twist steepened on Wednesday.

- The net short setting in the long end (flagged above) provided the most meaningful DV01 equivalent positioning adjustment.

| 06-Aug-25 | 05-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,576,105 | 4,560,638 | +15,467 | +567,824 |

FV | 7,048,214 | 7,017,897 | +30,317 | +1,297,264 |

TY | 5,110,737 | 5,094,292 | +16,445 | +1,088,166 |

UXY | 2,451,969 | 2,457,408 | -5,439 | -477,653 |

US | 1,767,692 | 1,746,506 | +21,186 | +2,972,608 |

WN | 1,983,910 | 1,978,027 | +5,883 | +1,078,942 |

|

| Total | +83,859 | +6,527,151 |

SOFR: Net Long Setting In SFRU5 Most Prominent On Wednesday

OI data points to a mix of net long setting and short cover through the SOFR reds on Wednesday, before a mix of net short setting and long cover came to the fore further out as the futures strip twist steepened.

- The most meaningful net positioning swing came via net long setting in SFRU5.

| 06-Aug-25 | 05-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,225,953 | 1,228,733 | -2,780 | Whites | +14,768 |

SFRU5 | 1,299,725 | 1,265,095 | +34,630 | Reds | -1,763 |

SFRZ5 | 1,360,191 | 1,364,698 | -4,507 | Greens | -8,900 |

SFRH6 | 1,049,923 | 1,062,498 | -12,575 | Blues | -2,890 |

SFRM6 | 874,402 | 878,790 | -4,388 |

|

|

SFRU6 | 856,066 | 853,616 | +2,450 |

|

|

SFRZ6 | 951,467 | 952,629 | -1,162 |

|

|

SFRH7 | 725,629 | 724,292 | +1,337 |

|

|

SFRM7 | 779,372 | 780,513 | -1,141 |

|

|

SFRU7 | 575,593 | 579,499 | -3,906 |

|

|

SFRZ7 | 510,911 | 512,899 | -1,988 |

|

|

SFRH8 | 332,344 | 334,209 | -1,865 |

|

|

SFRM8 | 267,656 | 273,215 | -5,559 |

|

|

SFRU8 | 205,702 | 206,936 | -1,234 |

|

|

SFRZ8 | 216,888 | 215,554 | +1,334 |

|

|

SFRH9 | 152,652 | 150,083 | +2,569 |

|

|

EUROPE ISSUANCE UPDATE

Spain auction results

- E1.675bln of the 2.40% May-28 Bono. Avg yield 2.166% (bid-to-cover 2.24x).

- E1.602bln of the 3.20% Oct-35 Obli. Avg yield 3.199% (bid-to-cover 2.12x).

- E1.221bln of the 3.45% Jul-43 Obli. Avg yield 3.758% (bid-to-cover 2.15x).

- E490mln of the 1.00% Nov-30 Obli-Ei. Avg yield 0.81% (bid-to-cover 2.83x).

France auction results

- E4.58bln of the 1.25% May-34 OAT. Avg yield 3.17% (bid-to-cover 2.47x).

- E2.396bln of the 1.25% May-36 OAT. Avg yield 3.41% (bid-to-cover 2.93x).

- E2.175bln of the 0.50% May-40 OAT. Avg yield 3.7% (bid-to-cover 3.30x).

- E1.348bln of the 4.00% Apr-55 OAT. Avg yield 4.09% (bid-to-cover 2.96x).

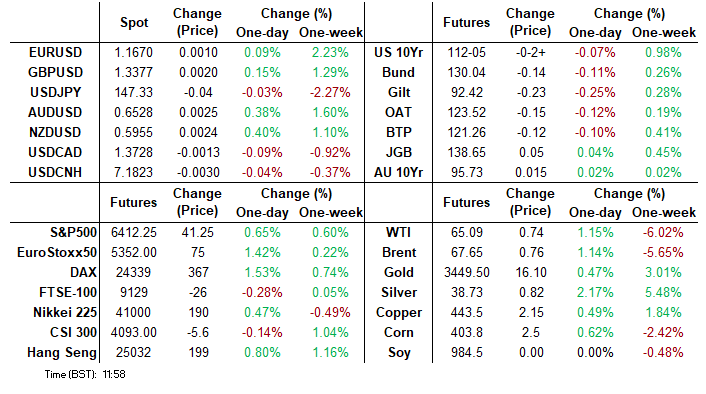

FOREX: USD Softer Again; Trump/Putin Talks Inject Dose of Risk

- After a bearish close Wednesday, the USD is softer again on the back of a further retracement of the US curve. Risk appetite also saw a boost as headlines confirmed a meeting set between Russian President Putin and US President Trump in the coming days. While the location is yet to be confirmed - the ceasefire demands on Moscow will undoubtedly be a topic of conversation. As a result, the Friday deadline for Russia has presumably been paused - however secondary sanctions on India and other select countries are expected to proceed.

- EUR/USD edged higher still early Thursday, further clearing the post-NFP high in the process. This keeps the recovery off the late July pullback low intact, and works against the bearish backdrop. The break of firm resistance into 1.1607, the 20-day EMA, is signaling greater odds of a further reversal higher.

- The BoE rate decision takes focus going forward, with GBP/USD again resilient. In particular, the vote split among the MPC will be of interest. Markets expect the committee to opt for a 25bps rate cut today, split down the lines of 2-5-2 (50bps cut, 25bps cut, unch) as the modal consensus. We flag that the baseline projections may become less useful as a communication tool going forward - and as such, less market relevant. EUR/GBP remains in a nascent uptrend, evident in the recovery from last Thursday's low. Key resistance and the bull trigger remains at 0.8769, the Jul 27 high.

- Focus elsewhere Thursday is on US weekly jobless claims and unit labor costs. Fed's Bostic is also due to be addressing monetary policy shortly after the BoE rate decision, while POTUS Trump is set to make remarks after the cash equity close.

OPTIONS: Expiries for Aug07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.1bln), $1.1600(E957mln)

- USD/JPY: Y146.50($605mln), Y146.93-05($569mln), Y147.65($1.4bln), Y148.00-15($2.0bln), Y148.50($1.2bln)

- EUR/JPY: Y170.00(E770mln)

- AUD/USD: $0.6500(A$1.2bln), $0.6600(A$2.0bln)

- USD/CAD: C$1.3800($700mln)

- USD/CNY: Cny7.2500($836mln)

EQUITIES: E-mini S&P Recovering Well, But Still Short of Resistance

The trend condition in Eurostoxx 50 futures faltered Friday, with short-term weakness resulting in a break of the bear trigger. Having shown below 5194.00, the Jun 23 low, the April 30 hi/lo range at 5078-5138 becomes the area of downside interest. E-mini S&P sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. Since that spell of weakness, price has recovered back above support at the 20-day EMA, at 6325.25.

- Japan's NIKKEI closed higher by 264.29 pts or +0.65% at 41059.15 and the TOPIX ended 21.35 pts higher or +0.72% at 2987.92.

Elsewhere, in China the SHANGHAI closed higher by 5.672 pts or +0.16% at 3639.667 and the HANG SENG ended 171 pts higher or +0.69% at 25081.63. - Across Europe, Germany's DAX trades higher by 241.09 pts or +1.01% at 24164.82, FTSE 100 lower by 24.86 pts or -0.27% at 9136.95, CAC 40 up 61.21 pts or +0.8% at 7696.92 and Euro Stoxx 50 up 49.87 pts or +0.95% at 5313.57.

- Dow Jones mini up 118 pts or +0.27% at 44433, S&P 500 mini up 35.25 pts or +0.55% at 6407, NASDAQ mini up 139.5 pts or +0.6% at 23566.

COMMODITIES: WTI Posts Bearish Daily Close

Gold benefited from the soft NFP print on Friday, returning prices toward the top-end of the recent range. This supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. WTI futures fell further Wednesday, keeping S/T momentum pointed lower. Support at the 50-day EMA has cracked, with the price closing below - a bearish signal. The clear break exposes $58.17, the May 30 low.

- WTI Crude up $0.21 or +0.33% at $64.57

- Natural Gas down $0 or -0.03% at $3.076

- Gold spot up $9.12 or +0.27% at $3378.57

- Copper up $2.05 or +0.46% at $443.4

- Silver up $0.4 or +1.05% at $38.2238

- Platinum down $8.65 or -0.65% at $1327.78

US-RUSSIA: Trump-Putin Summit Possible "In The Coming Days"-Kremlin Aide

Tass reporting comments from Kremlin aide Yuri Ushakov claiming that an agreement has been reached on holding a summit between Russian President Vladimir Putin and US President Donald Trump "in the coming days", with both sides working out the details. Adds that next week was designated as the target date, but that "it is difficult to say how many days preparations will take." Ushakov claims a venue has been agreed upon. Acknowledges that US Middle East envoy Steve Witkoff touched on the idea of a trilateral meeting involving Ukrainian President Volodymyr Zelensky, but Moscow has not responded.

- Trump posted on Truth Social, "My Special Envoy, Steve Witkoff, just had a highly productive meeting with Russian President Vladimir Putin. Great progress was made! Afterwards, I updated some of our European Allies. Everyone agrees this War must come to a close, and we will work towards that in the days and weeks to come...." Speaking later in the Oval Office, Trump was more circumspect, saying, “I don’t call it a breakthrough, I mean, we’ve been working on this a long time.”

- The First Deputy Chair of the Foreign Affairs Committee of the Federation Council (the upper house of the Russian Parliament) praised Witkoff, saying he had "earned significant support in Russia due to his transparency and realistic approach."

- Zelenskyy held a call with Trump after Witkoff's meeting, with European leaders including UK PM Sir Keir Starmer and German Chancellor Friedrich Merz on the line. Zelenskyy said that he would hold calls with the leaders of Germany, France, and Italy to discuss the prospect of a ceasefire, a leaders' summit, and security guarantees.

| Date | GMT/Local | Impact | Country | Event |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1130/1230 | BOE Press Conference | ||

| 07/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 07/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 07/08/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 07/08/2025 | 1300/1400 | BOE Decision Maker Panel Data BOE Decision Maker Panel Data | ||

| 07/08/2025 | 1400/1000 | * | Ivey PMI | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 07/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 07/08/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 07/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 07/08/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 07/08/2025 | 1900/1500 | * | Consumer Credit | |

| 07/08/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 08/08/2025 | 2330/0830 | ** | Household spending | |

| 08/08/2025 | 2350/0850 | Balance of Payments | ||

| 08/08/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/08/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 08/08/2025 | 1115/1215 | BOE Pill At National MPC Agency Briefing | ||

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1420/1020 | St. Louis Fed's Alberto Musalem | ||

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |