MNI US MARKETS ANALYSIS - Dovish Fed Pricing Holds Into NFP

Highlights:

- Fed funds implied rates hold recent dovish shift into what's expected to be a softer payrolls report

- UK PM Starmer expected to face a tough reception at weekly PMQs

- CAD, MXN offered as Trump reportedly considers abandoning USMCA altogether

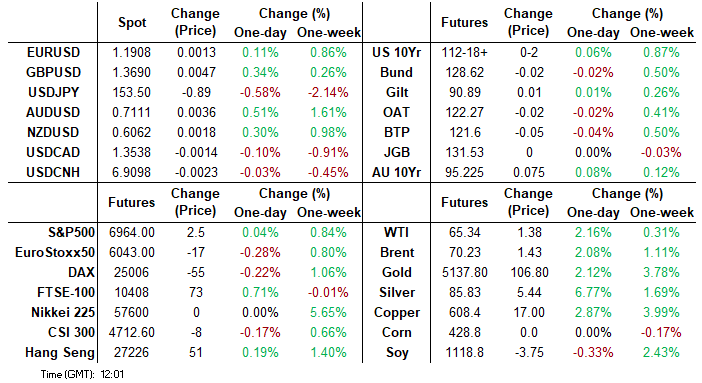

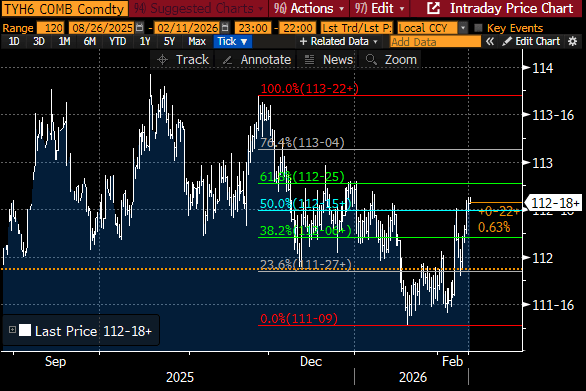

US TSYS: Data-Induced Gains Held Before A Wednesday NFP Report

Treasuries broadly consolidate yesterday’s gains on clearly weaker than expected retail sales data in a further dovish build-up ahead of today’s unusual Wednesday release for nonfarm payrolls. The short-term bullish condition in TYH6 has been strengthened and starts to eye a next resistance at 112-25.

- Cash yields are 0.8-1.7bp lower, with declines led by 5s.

- 10Y yields at 4.129% (-1bp) are close to lows since Jan 15 vs last Thursday’s 4.2796% before a slew of soft labor updates.

- TYH6 trades at 112-18+ (+02) for close to earlier highs of 112-20, on reasonable cumulative volumes of 315k for a pre-NFP overnight session and with a Japanese holiday.

- This week’s rally has strengthened a short-term bullish condition with further resistance seen at 112-25 (61.8% retrace of Nov 25 – Jan 20 bear leg) after which could see 112-27 (today’s equivalent to the 4.10% yield).

- To the downside, support is seen at 112-00 (20-day EMA) before 111-26 (Feb 9 low).

- Data: Weekly MBA mortgage applications (0700ET), Nonfrm payrolls Jan (0830ET), Federal budget balance Jan (1400ET)

- Fedspeak: Schmid (1000ET), Bowman (1015ET), Hammack (1600ET) – see STIR bullet

- Coupon issuance: US Tsy $42B 10Y Note auction - 91282CPZ8 (1300ET). Last month’s 10Y auction stopped through by 0.6bps whilst the bid-to-cover was steady at 2.55x.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in visit with Israel PM (1100ET), Trump in Champion of Coal event (1600ET), Trump meets with special envoy to UK (1730ET)

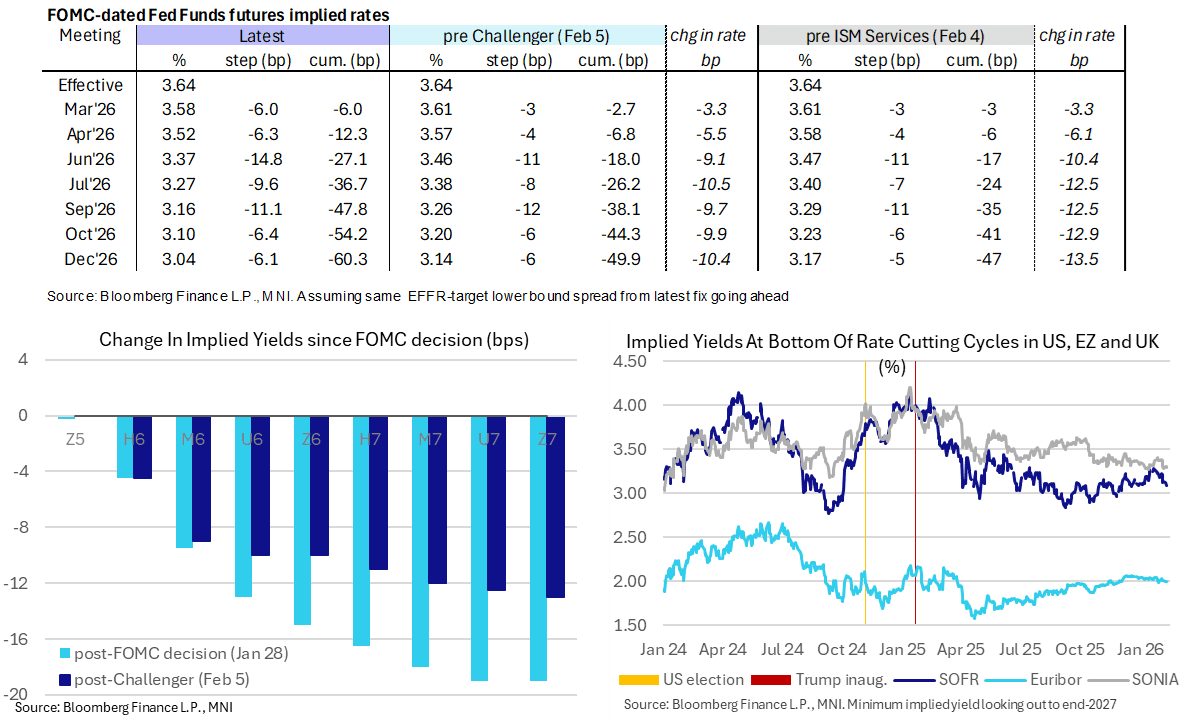

STIR: Dovish Shift Held Ahead Of NFPs and Fed Reaction

- Fed Funds implied rates hold the dovish shift in recent days ahead of today’s NFP release (Preview: https://mni.marketnews.com/3Mv6fNA) helped by soft data (both labor and yesterday’s retail sales) and Trump administration officials attempting to manage expectations of softer jobs numbers.

- The near-term rate path sees the most conviction in a June rate cut since spillover from crypto and precious metals pressure last week and before that Jan 9, whilst the terminal yield is at ytd lows.

- FF cumulative cuts from 3.64% effective: 6bp Mar, 12.5bp Apr, 27bp Jun, 36.5bp Jul, 48bp Sep, 54bp Oct and 60.5bp Dec.

- SOFR futures are little changed on the day, with the terminal implied yield of 3.09% (H7) at the bottom of the ytd range of 3.09-3.285% across closes.

- Today’s Fedspeak can see reaction to today’s job numbers from either end of the hawk-dove spectrum. Schmid (hawk) speaks for the first time in nearly a month, although he next has a voting role in 2028.

- 1000ET – Kansas City Fed’s Schmid on mon pol and economic outlook (text + Q&A). He said Jan 15 that his preference is to keep policy modestly restrictive and that rate cuts risk inflation harm without supporting the labor market.

- 1015ET – VC Supervision Bowman (voter, dove) in moderated conversation at a financial services conference. She said on Jan 30 that while she didn't elect to cut rates in January, she could be ready to cut in March. She made clear that she saw 3 cuts this year in the Dec SEP, making her one of the biggest doves on the Committee as widely assumed.

- 1600ET – Cleveland Fed’s Hammack (’26 voter, hawk) on leadership. Topic aside, she said yesterday that rates could be on hold for some time.

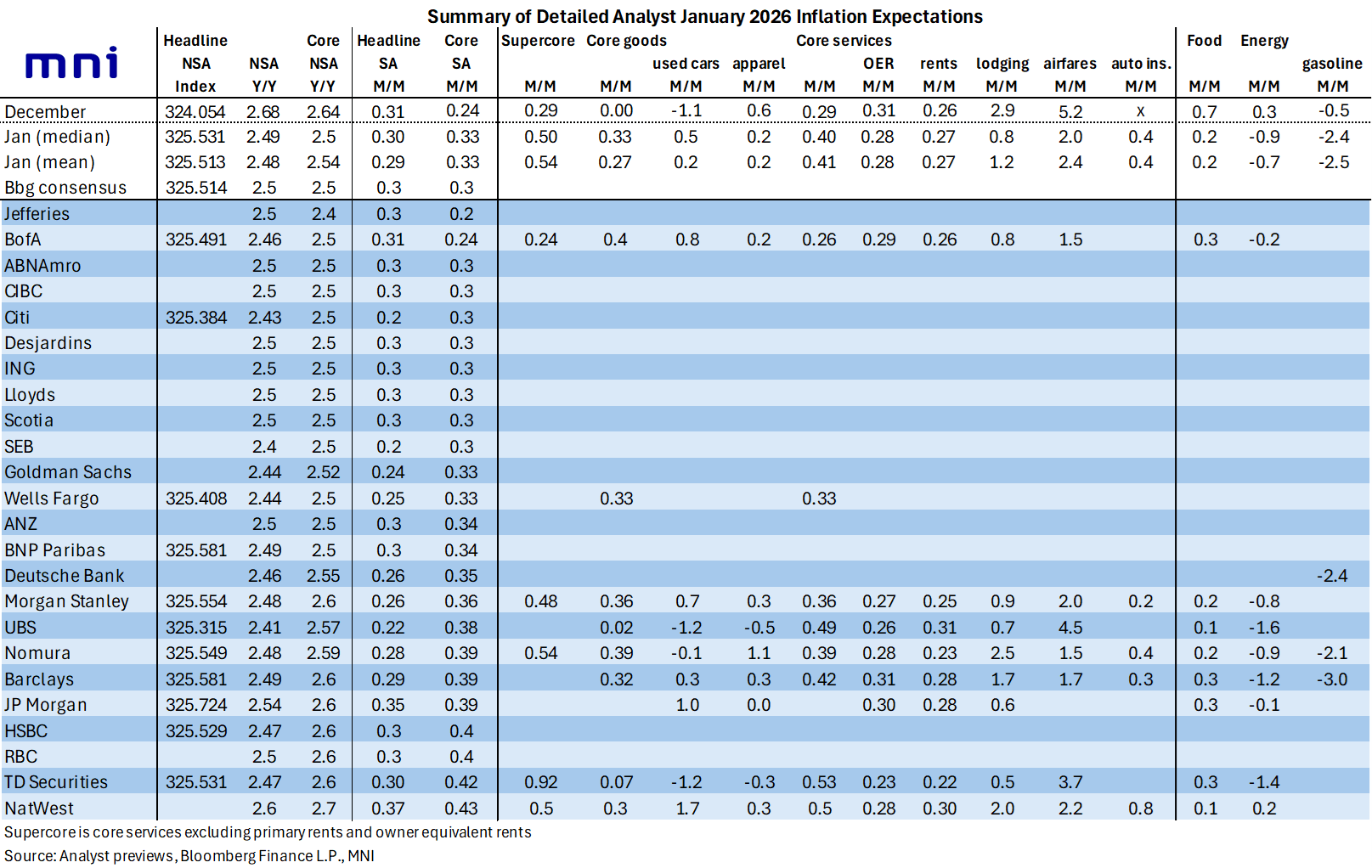

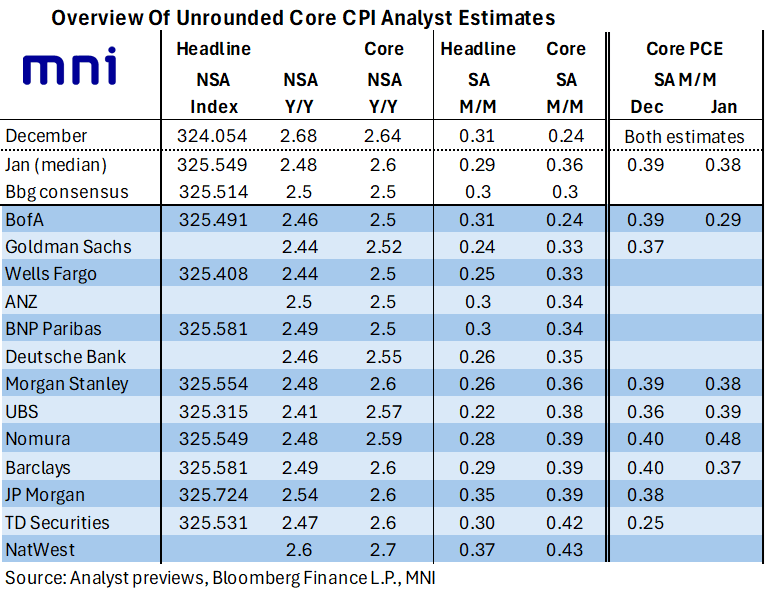

US PREVIEW: Used Cars and Smaller Services Behind Expected Core CPI Firming

Analysts look for the acceleration in core CPI to come from both goods and services:

- on the core goods side, used cars are on balance expected to play a large role in the sequential firming, shifting from -1.1% M/M in December to perhaps a small positive. That’s far from a uniform view though with an analyst range of -1.2% to 1.7%.

- going against this but with a smaller weight, apparel is on balance expected to moderate with a median 0.2% estimate after a strong 0.6% M/M in December.

- on the core services side, the sequential firming comes despite relative softening in some of the noisier non-housing categories that can swing broader inflation from month-to-month. In particular, airfares (no feed through to PCE) and lodging away from home (feeds through to PCE) are expected to moderate after strong increases in December.

- rental inflation is expected to be fractionally softer than in December, with an average estimate of 0.28% for OER (range 0.23-0.31) after 0.31% but tenants’ rents at 0.27% (range 0.22-0.31) after 0.26%.

- the gap, with these large service components at similar monthly pace/softer than in December likely reflects a residual seasonality boost expected more broadly.

Away from core CPI, headline inflation is expected to be weighed on by softer food and energy inflation.

- Food inflation is expected to moderate heavily after a far stronger than expected 0.7% M/M in December, its strongest monthly increase since Aug 2022 but also a move that looked suspiciously like a reversal of November holiday discounting (with the later than survey period back in November).

- Energy prices are also expected to have seen a reasonable seasonally adjusted decline after a modest increase in December. Note the wider than usual range to analyst estimates this month (from -1.6% to 0.2%) which we suspect is down to treatment of differing natural gas and electricity price assumptions.

[A quick reminder that the below table shows median/mean figures across all estimates. The core CPI median of 0.33% M/M would be 0.36% M/M if only taking unrounded estimates per the separate table shown above]

US PREVIEW: Unrounded Core CPI Estimates Point To Upside Risk In January

Today’s NFP report is clearly in immediate focus but we quickly look ahead to Friday’s CPI report, where unrounded core CPI estimates point to upside risk to consensus compared to more in-line/softer readings for headline.

- We see a median of thirteen unrounded estimates for core CPI at 0.36% M/M (Bloomberg cons 0.3) having surprised clearly lower back in December with 0.24% M/M vs the median estimate of 0.35% at the time.

- This monthly strength also translates to upside risk for the Y/Y figures in NSA data, with a median 2.6% vs 2.5% consensus after 2.64% in December. Include a wider range of rounded estimates and this would sit on the cusp of a 2.5-2.6% Y/Y print (to be shown in a second table in part two).

- Headline estimates look more in line with consensus however, with a median 0.29% M/M (Bloomberg cons 0.3). They are also closer to the rounded consensus of 2.5% Y/Y with some seeing risk of rounding lower.

- A smaller sample of unrounded estimates for core PCE currently tracks at 0.39% M/M in December and 0.38% M/M in January. The delayed December PCE report is currently due to be released on Feb 20 before the January report on Mar 13.

- The full MNI US CPI Preview will be published later today once the payrolls report is fully wrapped up.

SOFR: Short Cover In White Pack Dominated Following Soft Retail Sales

OI data points to meaningful net short cover in the white pack of the SOFR futures strip as the softer-than-expected retail sales data triggered dovish repricing on Tuesday. Long setting was more prominent further out the strip.

| 10-Feb-26 | 09-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,348,752 | 1,351,972 | -3,220 | Whites | -130,177 |

SFRH6 | 1,302,214 | 1,349,589 | -47,375 | Reds | +854 |

SFRM6 | 1,403,277 | 1,436,485 | -33,208 | Greens | +11,781 |

SFRU6 | 1,374,369 | 1,420,743 | -46,374 | Blues | +4,518 |

SFRZ6 | 1,389,437 | 1,402,174 | -12,737 |

|

|

SFRH7 | 970,542 | 962,171 | +8,371 |

|

|

SFRM7 | 890,529 | 889,105 | +1,424 |

|

|

SFRU7 | 842,345 | 838,549 | +3,796 |

|

|

SFRZ7 | 918,479 | 913,067 | +5,412 |

|

|

SFRH8 | 527,865 | 520,395 | +7,470 |

|

|

SFRM8 | 441,973 | 441,540 | +433 |

|

|

SFRU8 | 393,448 | 394,982 | -1,534 |

|

|

SFRZ8 | 383,760 | 374,845 | +8,915 |

|

|

SFRH9 | 222,680 | 216,867 | +5,813 |

|

|

SFRM9 | 206,352 | 213,039 | -6,687 |

|

|

SFRU9 | 173,695 | 177,218 | -3,523 |

|

|

US TSY FUTURES: Short Cover Outweighs Long Setting On Tuesday

OI data points to a mix of net short cover (TU, FV, TY & UXY) and long setting (US & WN) as Tsy futures rallied on Tuesday, with the former providing the dominant move in curve-wide DV01 terms.

- Net long setting in US futures provided the largest DV01 swing in individual contract terms.

| 10-Feb-26 | 09-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,659,442 | 4,703,183 | -43,741 | -1,608,789 |

FV | 6,834,310 | 6,882,157 | -47,847 | -2,053,316 |

TY | 5,420,663 | 5,468,616 | -47,953 | -3,164,507 |

UXY | 2,545,476 | 2,576,871 | -31,395 | -2,811,848 |

US | 1,738,174 | 1,705,015 | +33,159 | +4,631,970 |

WN | 2,187,762 | 2,179,540 | +8,222 | +1,504,697 |

|

| Total | -129,555 | -3,501,792 |

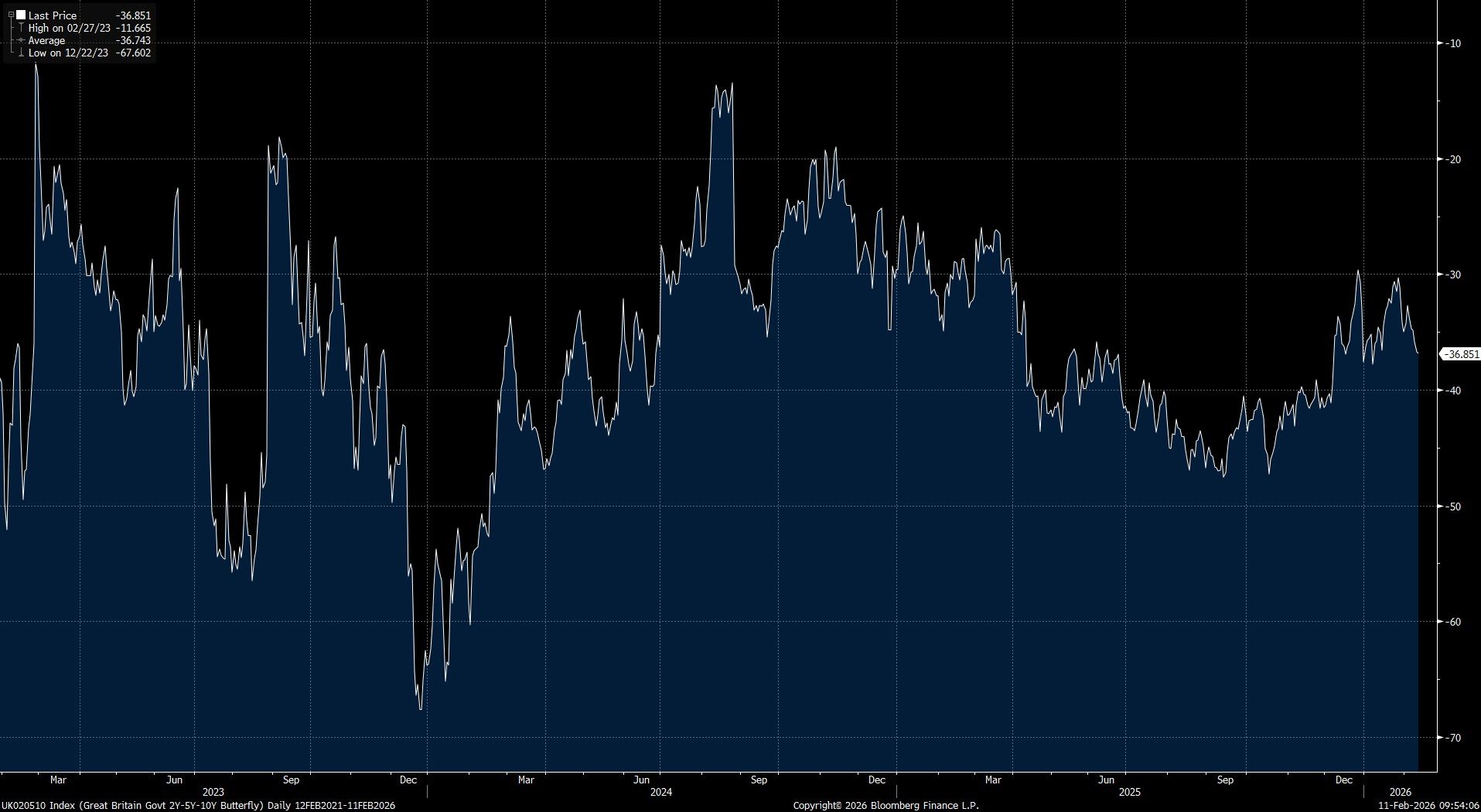

GILTS: Fiscal Risk & Dovish BoE Supports Receiving Belly of 2-/5-/10-Year Fly

Those looking for fresh fiscal/political risk premia to be embedded into gilts may look to engage in long 5s vs. 2s and 10s on a gilt butterfly after the structure failed to break its December closing high as 5s cheapened during January.

- We have previously noted that any eventual leadership challenge/Starmer resignation would probably see the market initially focus on the likelihood that UK fiscal policy would become more expansionary under a new PM, resulting in the pricing of shallower BoE easing.

- However, increased fiscal uncertainty would likely steepen the 5s10s side of the structure, providing at least some insulation to any hawkish monetary policy repricing, if not a full offset.

- Beyond the initial knee-jerk, medium-term focus could quickly come to the fore. If there is greater fiscal expansion it will need to be funded through increasing taxes (a left leaning government is more likely to be focus such hikes on business/higher earners/entrepreneurs and hit private sector confidence more, resulting in deeper BoE rate cuts) or without the backing of the OBR, risking a hit to credibility. The Truss moment provides a recent example of the latter, which would knock confidence and possibly result in deeper rate cuts being delivered further down the line. 5s could also outperform against this backdrop.

- Outside of a leadership change, further dovish developments at the BoE (after last week’s ‘dovish hold’) would provide tailwinds for the position. Here we caution that markets have been unable to fully discount 50bp of further easing for the current cycle during the 2 most recent instances of notable dovish repricing. This suggests that fresh dovish developments are required to promote a meaningful shift here e.g. signals of further easing alongside a March cut (~17bp of easing priced for the March BoE at present).

Fig. 1: Gilt 2-/5-/10-Year Butterfly (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

EUROPE ISSUANCE UPDATE:

France syndication: Priced

- E8bln (MNI expected E8bln) of the new 30-year 4.40% May-57 OAT. Spread set at 3.75% May-56 OAT +4bp (guidance was 3.75% May-56 OAT +6bp area), Books closed in excess of E135bln. Reoffer 99.329 to yield 4.439%.

- That E135bln will be a record book size for France (although is still pre-rec at present). It is marginally larger than the E134bln seen in January 2025 for the long 15-year 3.60% May-42 OAT launch.

Slovakia syndication: Launched

- E2.0bln (MNI expected E2.0-3.0bln although size guidance from ARDAL was for E2.0-2.5bln) of the new 20-year Feb-46 SlovGB. Spread set at MS + 110bps (guidance was MS+120 Area MS+ 115bps area), books closed in excess of E8.6bln.

Gilt syndication announcement

- DMO has noted that it will launch a new green gilt maturing on 7 March 2037 in the week commencing 9 March. We expect a GBP6.5bln transaction size for now.

Gilt tender results

- GBP0.3bln of the 4.25% Dec-49 Gilt. Avg yield 5.256% (bid-to-cover 4.32x, tail 0.2bp).

Greece auction results

- E300mln of the 3.375% Jun-36 GGB. Avg yield 3.34% (bid-to-cover 2.62x).

Germany auction results

- E1bln (E749mln allotted) of the 2.50% Aug-54 Bund. Avg yield 3.47% (bid-to-offer 1.16x; bid-to-cover 1.54x).

- E1.5bln (E1.16bln allotted) of the 2.90% Aug-56 Bund. Avg yield 3.47% (bid-to-offer 1.26x; bid-to-cover 1.63x).

Portugal auction results

- E708mln of the 1.95% Jun-29 OT. Avg yield 2.178% (bid-to-cover 2.28x).

- E673mln of the 3.25% Jun-36 OT. Avg yield 3.142% (bid-to-cover 2.02x).

UK: PMQs At Top Of Hour w/Starmer Still Under Pressure

Prime Minister's questions get underway at the top of the hour (livestream here). PMQs are rarely a noteworthy event for markets, but the significant political pressure that PM Sir Keir Starmer is currently under could give today's session in the House of Commons increased focus.

- On Monday, there was significant speculation that Starmer could resign or face a formal leadership challenge. Leader of the Scottish Labour Party, Anas Sarwar, publicly called for the PM's resignation in a press conference. However, this intervention was swiftly marginalised as the Cabinet and senior Labour figures expressed their support for Starmer's continued leadership.

- Starmer declared he would continue in officehaving been handed a sizeable mandate in the 2024 general election. The furore surrounding Peter Mandelson's ambassadorial appointment prompted the resignation of Starmer's chief of staff and communications director, and drew attention to a former senior aide who apologised for past associations with a convicted paedophile former councillor, leaving the PM in a weakened position with fewer of his close allies in 10 Downing Street.

- Despite surviving the events of the past 48 hours, questions remain over party stability and internal divisions within Labour, with an increased likelihood that Starmer will be challenged in the near future.

EU-UK: Politico-Reeves Will Call To Rebuild EU Ties

Politico reports that the UK's Chancellor of the Exchequer, Rachel Reeves, is set to call for ties with the European Union to be rebuilt. Politico reports an extract from the speech stating, "There are three big economic blocks: US, China and Europe. We will always seek every opportunity to grow our economy and these trading relationships, but ultimately only one of these is on our doorstep, and so the biggest prize is closer integration with Europe.”

- Reeves is due to speak at a Bruegel event at the LSE this evening at 18:00GMT (13:00ET, 19:00CET).

- Discussing Brexit has become of a 'third rail' for the governing centre-left Labour party, something that it avoids touching at all costs. In the 2016 referendum, Labour backed the Remain campaign. Prior to the UK formally leaving the EU in 2020, Labour supported a second referendum, but since then, under PM Sir Keir Starmer, it has not formally advocated for a new vote.

- The issue has recently raised its head, with Health Secretary Wes Streeting appearing to back the UK joining a customs union with the EU in a Dec 2025 interview, despite this not being the gov'ts official position. This was seen as laying down a challenge to Starmer, a view that will only intensify amid today's reports that Streeting could look to oust the PM sooner rather than later.

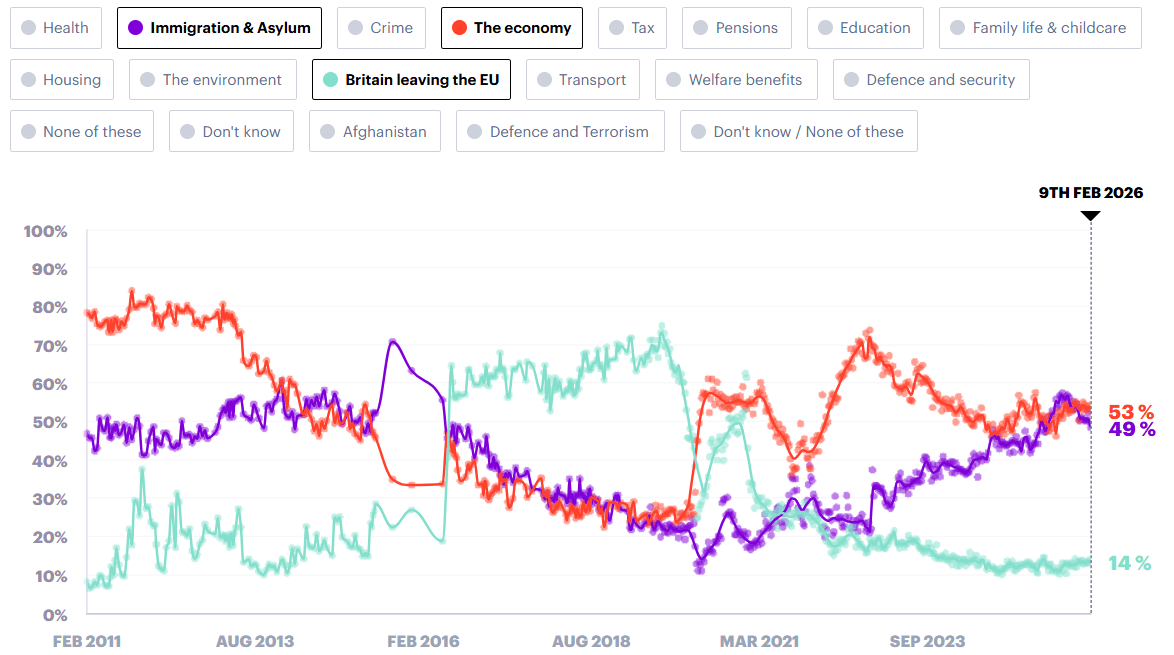

- The Brexit issue has slipped down the list of main political issues facing the country, according to polls. YouGov's issues tracker has just 14% of respondents in February selecting it as one of their three key issues, compared to 53% for the top issue (the economy) and 49% for immigration in second.

Chart 1. Opinion Polling, Most Important Issues Facing the Country, %

Source: YouGov

GLOBAL MACRO: Trump Considering Withdrawing Entirely from USMCA - Bloomberg

Bloomberg reports that "President Donald Trump is privately musing about exiting the North American trade pact, people familiar with the matter said, injecting further uncertainty about the deal’s future into pivotal renegotiations involving the US, Canada and Mexico."

The piece writes that:

- The president has asked aides why he shouldn’t withdraw from the agreement, which he signed during his first term, though he has stopped short of flatly signaling that he will do so

- A White House official [...] described Trump as the ultimate decision-maker and someone always seeking a better deal for the American people. Discussion about potential action amounted to baseless speculation before an announcement from the president, the official said.

- Generally speaking, these negotiations are going to proceed bilaterally and separately, the Mexicans are being quite pragmatic right now. We’ve had a lot of discussions with them. With the Canadians, it’s more challenging,” Greer said on Fox Business.

USDCAD is recovering from lows at typing, while USDMXN has taken a bigger move higher: rate is erasing the day's losses to trade lower by 0.1% on the day - having traded lows of 17.1307 just before the report.

CHF: EURCHF Consolidates In Low 0.91s, Sellside Remains Bullish

- Swiss Franc resilience continues to be on show in 2026, with EURCHF consolidating in the low 0.91s on Wednesday. The softer greenback has prompted USDCHF to edge closer to cycle lows which are located 0.7605, with participants also awaiting inflation data from both Switzerland and the US on Friday.

- UBS flag that "asset managers are buying CHF at the fastest pace in a decade", one factor leading to their call for 0.75 USDCHF at quarter-end estimate, and "consistent with deeper EURCHF downside towards 0.90 by year-end and beyond".

- Danske meanwhile say "We think the bar is relatively high for the SNB to intervene [...] also note the shift taking place in safe-haven dynamics the past year which has favoured a stronger CHF [...] stick to our long call of being bullish CHF FX."

- This comes after Morgan Stanley targeted EURCHF 0.8700 earlier this week.

FOREX: DXY Extends Reversal Lower, USDJPY Approaching 152.10 Support

- Although much of the focus has been on the yen over the past two sessions, the Ice USD index has been gradually edging lower, approaching 96.50 as we await the key US employment figures later today. It’s been well noted that the DXY’s recovery to the December lows around the 98.00 mark appears to have provided an attractive entry point for those looking to reengage shorts.

- Yesterday’s retail sales data has certainly added to the renewed greenback pessimism, alongside the dovish repricing across the US curve. This dynamic provides an important backdrop for today’s payrolls report, as weak figures may bolster bets on imminent easing from the Fed. The data will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

- With Japan out for a national holiday today, the JGB stabilisation theme has allowed the yen to extend its post-election upswing, with the US data assisting the squeeze. USDJPY broke swiftly through the 100-day MA on Tuesday, and spot has traded down to 152.80 overnight, narrowing the gap substantially to 152.10 support.

- The sharp downswing for GBPJPY has seen spot extend below the 50-day EMA to fresh 2026 lows. The average has been a notable pivot given the fact we have not posted a daily close below it since October, and it acted as perfect support on Jan 26. Next support is seen at 206.78, the Dec 16 low.

- Elsewhere, AUDUSD broke above the 0.71 handle overnight after RBA's Hauser said the country's inflation rate is too high and the RBA will take all necessary measures to bring it under control. 0.7128 highs bring us closer to the 2023 peak, at 0.7158.

- MBA Mortgage Applications are scheduled ahead of payrolls. Fed's Schmid, Bowman and Hammack will appear while ECB hawk Schnabel is also scheduled.

OPTIONS: Expiries for Feb11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1820-30(E1.4bln), $1.1850(E742mln), $1.1900(E535mln), $1.2000(E1.8bln)

- USD/JPY: Y156.45-60($2.2bln)

- GBP/USD: $1.3575(Gbp537mln)

- EUR/GBP: Gbp0.8660(E821mln)

- USD/CAD: C$1.3700($874mln)

EQUITIES: Tuesday's Cycle High for EuroStoxx Futures Reinforces Bullish Theme

The medium-term trend condition in EuroStoxx 50 futures remains bullish and yesterday's fresh cycle high reinforces the bull theme. The move higher paves the way for a climb towards 6100.00 and 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5890.56, the 50-day EMA. Clearance of this average would highlight a short-term top and signal scope for a deeper pullback. The firm reversal higher on Feb 6 in S&P E-Minis refocuses attention on the primary uptrend and key resistance at 7043.00, the Jan 28 high. Clearance of this level would confirm a resumption of the primary uptrend and mark the end of a flat correction in the contract. Key short-term support has been defined at 6751.50, the Feb 6 low, where a break is required to highlight a top and a stronger short-term reversal.

- In China the SHANGHAI closed higher by 3.611 pts or +0.09% at 4131.985 and the HANG SENG ended 83.23 pts higher or +0.31% at 27266.38.

- Across Europe, Germany's DAX trades lower by 80.22 pts or -0.32% at 24908.04, FTSE 100 higher by 38.7 pts or +0.37% at 10392.8, CAC 40 down 42.19 pts or -0.51% at 8285.69 and Euro Stoxx 50 down 23.81 pts or -0.39% at 6023.25.

- Dow Jones mini up 37 pts or +0.07% at 50308, S&P 500 mini down 2.5 pts or -0.04% at 6959, NASDAQ mini down 43.5 pts or -0.17% at 25172.5.

COMMODITIES: WTI Futures Narrow Gap to Bull Trigger at $66.48

A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.33. The 50-day EMA lies at $60.63. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger to watch has been defined at $66.48, the Jan 30 high. The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude up $0.9 or +1.41% at $64.85

- Natural Gas up $0 or +0.13% at $3.12

- Gold spot up $44.51 or +0.89% at $5071.67

- Copper up $7.5 or +1.27% at $598.85

- Silver up $4.08 or +5.05% at $84.9387

- Platinum up $91.98 or +4.41% at $2179.76

| Date | GMT/Local | Impact | Country | Event |

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack | ||

| 12/02/2026 | 0700/0700 | *** | UK Monthly GDP | |

| 12/02/2026 | 0700/0700 | ** | Trade Balance | |

| 12/02/2026 | 0700/0700 | ** | Index of Production | |

| 12/02/2026 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/02/2026 | 0700/0700 | ** | Index of Services | |

| 12/02/2026 | 0700/0700 | *** | GDP First Estimate | |

| 12/02/2026 | 0900/1000 | ECB's Cipollone At Commissione Europa Conference | ||

| 12/02/2026 | - | BOE MPG Meeting | ||

| 12/02/2026 | - | *** | New Loans | |

| 12/02/2026 | - | *** | Money Supply | |

| 12/02/2026 | - | *** | Social Financing | |

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers panel talk on productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR existing home sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane At The World Ahead 2026 Gala Dinner |