UK: PMQs At Top Of Hour w/Starmer Still Under Pressure

Feb-11 11:55

Prime Minister's questions get underway at the top of the hour (livestream here). PMQs are rarely a noteworthy event for markets, but the significant political pressure that PM Sir Keir Starmer is currently under could give today's session in the House of Commons increased focus.

- On Monday, there was significant speculation that Starmer could resign or face a formal leadership challenge. Leader of the Scottish Labour Party, Anas Sarwar, publicly called for the PM's resignation in a press conference. However, this intervention was swiftly marginalised as the Cabinet and senior Labour figures expressed their support for Starmer's continued leadership.

- Starmer declared he would continue in officehaving been handed a sizeable mandate in the 2024 general election. The furore surrounding Peter Mandelson's ambassadorial appointment prompted the resignation of Starmer's chief of staff and communications director, and drew attention to a former senior aide who apologised for past associations with a convicted paedophile former councillor, leaving the PM in a weakened position with fewer of his close allies in 10 Downing Street.

- Despite surviving the events of the past 48 hours, questions remain over party stability and internal divisions within Labour, with an increased likelihood that Starmer will be challenged in the near future.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Firmly Bear Steeper Following Powell Subpoenas, 4.20% 10Y Yields Probed

Jan-12 11:54

Treasuries trade firmly steeper from Friday’s close in reaction to the DoJ serving Powell with subpoenas over the weekend, driving heavy volumes and multiple tests of 4.20% 10Y yields. Today sees front-loaded US supply (owing to settlement ahead of MLK Day next week) before NY Fed’s Williams after the close.

- Cash yields are 0-4.4bp higher from Friday’s close, led by 20s.

- 10Y yields currently sit at 4.199% (+3.4bp) after brief tests above 4.20%, after similar levels following Friday’s NFP report saw buyers step in.

- TYH6 trades at 112-02 (-05), near session lows as it probes level equivalent to the 4.20% yield (112-02+ today), with huge cumulative volumes of 790k.

- It currently remains within Friday’s range with its low of 111-31 just above a key support at 111-29 (Dec 10 low). A breach would confirm a continuation of the bear cycle and could initially open 111-19 (1.236 proj of Oct 17 – Nov 5 – 25 price swing), whilst a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. A key short-term resistance is unchanged at 112-31 (Dec 18 high).

- Data: No data of note today with focus firmly on tomorrow’s CPI report for December.

- Fedspeak: Bostic moderates discussion (1230ET), Barkin in fireside chat (1245ET), Williams keynote remarks (1800ET) – see STIR bullet

- Coupon issuance: US Tsy $39B 10Y Note re-open - 91282CPJ4 (1300ET)

- Bill issuance: US Tsy $58B 3Y Note (91282CPT2) & $77B 26W bill auctions (1130ET), $86B 13W bill auction (1300ET)

- Politics: Trump meets with Secretary of State (1030ET), Trump meets with Archbishop Coakley (1330ET), Trump participates in Signing Time (1530ET), Trump meets with CEO of Tunnel to Towers Foundation (1600ET)

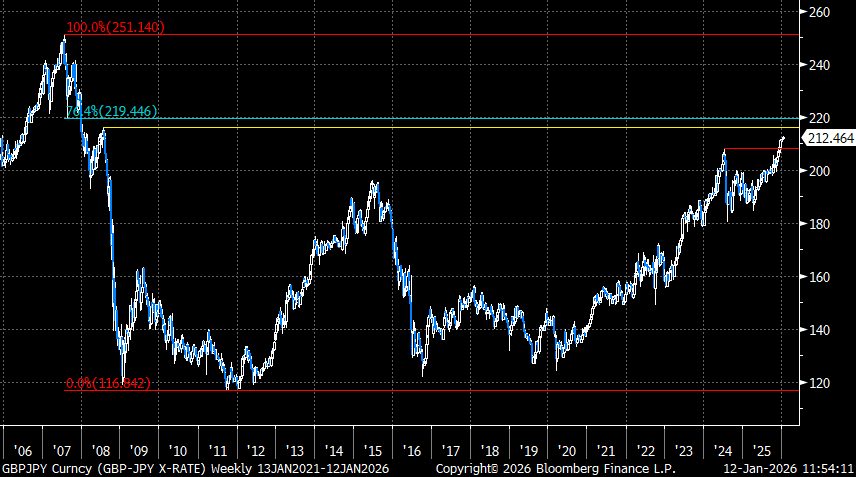

FOREX: GBPJPY Extends to New Cycle High, Sights on Mid-2008 Peak

Jan-12 11:54

- Sterling is a moderate outperformer to start the week, and despite the weaker equity backdrop, GBPJPY has risen to a fresh cycle high above 212.50 this morning. This extends the latest upswing for the cross, which gathered momentum on a break of 208.00 in December and now places the cross at the highest level since mid-2008.

- Moving average studies continue to highlight the sharp uptrend for the cross, with the 20-day EMA providing almost perfect support on three occasions since mid-November.

- Price action has taken spot considerably closer to a key medium-term target at 215.88, the July 2008 high. Above here, 219.45 is another meaningful target, the 76.4% retracement of the 2007-2011 range.

- Analysts continue to cite post-budget positioning adjustments as driving the recent optimism for GBP, however, as Rabo note, this may only have a little further to run near-term as they await the release of monthly UK November GDP data on Jan 15 to provide fresh direction.

- Separately Goldman Sachs say that while much of the Sterling price action throughout 2025 was driven by the ebb and flow of UK fiscal risk premium, they think the stage is set for a much more ‘conventional’ form of underperformance in 2026 driven by data, policy, and valuation.

EURIBOR OPTIONS: Call Spread buyer

Jan-12 11:54

0RM6 98.00/98.25cs, bought for 3.5 in 10k