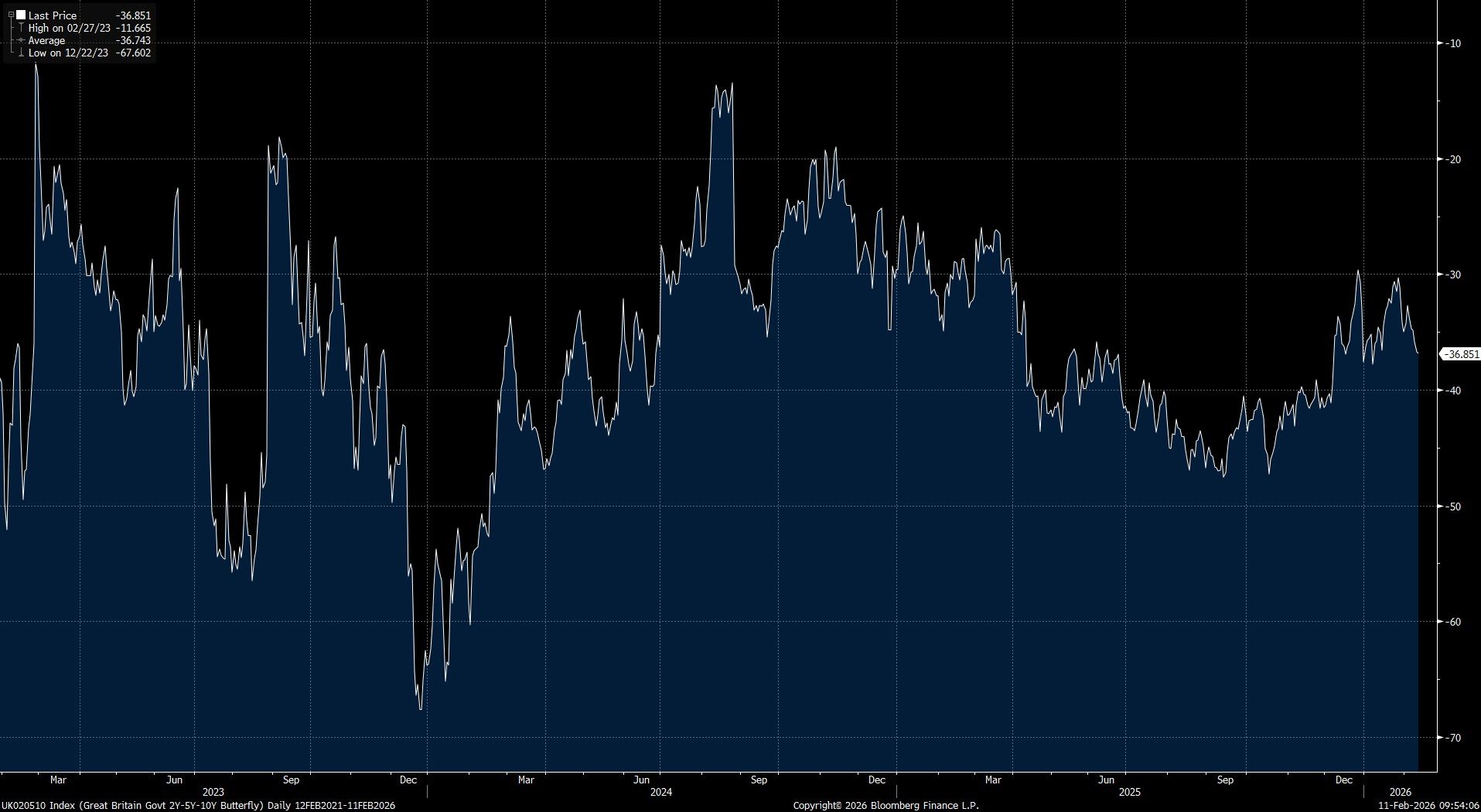

GILTS: Fiscal Risk & Dovish BoE Supports Receiving Belly of 2-/5-/10-Year Fly

Those looking for fresh fiscal/political risk premia to be embedded into gilts may look to engage in long 5s vs. 2s and 10s on a gilt butterfly after the structure failed to break its December closing high as 5s cheapened during January.

- We have previously noted that any eventual leadership challenge/Starmer resignation would probably see the market initially focus on the likelihood that UK fiscal policy would become more expansionary under a new PM, resulting in the pricing of shallower BoE easing.

- However, increased fiscal uncertainty would likely steepen the 5s10s side of the structure, providing at least some insulation to any hawkish monetary policy repricing, if not a full offset.

- Beyond the initial knee-jerk, medium-term focus could quickly come to the fore. If there is greater fiscal expansion it will need to be funded through increasing taxes (a left leaning government is more likely to be focus such hikes on business/higher earners/entrepreneurs and hit private sector confidence more, resulting in deeper BoE rate cuts) or without the backing of the OBR, risking a hit to credibility. The Truss moment provides a recent example of the latter, which would knock confidence and possibly result in deeper rate cuts being delivered further down the line. 5s could also outperform against this backdrop.

- Outside of a leadership change, further dovish developments at the BoE (after last week’s ‘dovish hold’) would provide tailwinds for the position. Here we caution that markets have been unable to fully discount 50bp of further easing for the current cycle during the 2 most recent instances of notable dovish repricing. This suggests that fresh dovish developments are required to promote a meaningful shift here e.g. signals of further easing alongside a March cut (~17bp of easing priced for the March BoE at present).

Fig. 1: Gilt 2-/5-/10-Year Butterfly (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

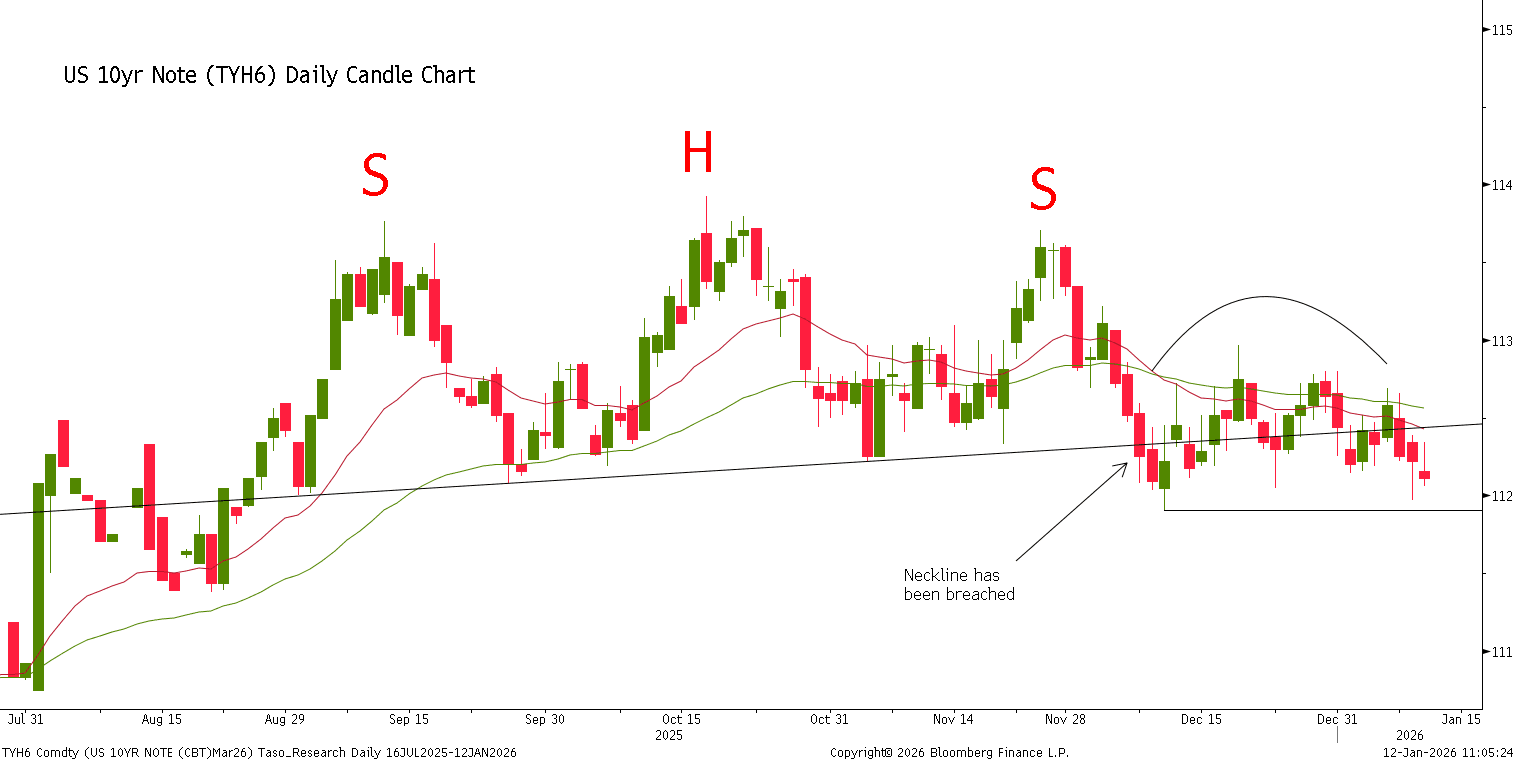

US 10YR FUTURE TECHS: (H6) Head And Shoulders Reversal Pattern

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-22 High Jan 7

- PRICE: 112-03+ @ 10:57 GMT Jan 10

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Treasuries remain above a key support - for now - at 111-29, the Dec 10 low. The trend set-up is bearish and a breach of 111-29 would confirm a continuation of the bear cycle. Note that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. A breach of 111-29 would open 111-19 initially, a Fibonacci projection. Key short-term resistance is unchanged at 112-31, the Dec 18 high.

EGB SYNDICATION: Greece 10-year mandate

"The Hellenic Republic has mandated BNP Paribas, BofA Securities, Deutsche Bank, Goldman Sachs Bank Europe SE, J.P. Morgan and Morgan Stanley as Joint Lead Managers for a new Reg S Cat 1/144A 10-year EUR Benchmark CAC bond to be issued in dematerialised registered form.

The syndicated transaction will be launched in the near future, subject to market conditions. ICMA stabilisation rules and regulations apply."

From market source

- In line with our expectations, as outlined in our January EGB syndication expectations. We pencil in a E4bln transaction size.

EFSF ISSUANCE: Dual Tranche 3/10-year Syndication: Final terms

New 3-year Benchmark

- Size: E3bln

- Spread set at MS+5bps (guidance was MS +6bps area)

- Books closed in excess of E18bln (inc E1.3bln JLM interest)

- Coupon: Long first

- Maturity: Feb 2, 2029

- ISIN: EU000A2SCAW0

New 10-year Benchmark

- Size: E4bln

- Spread set at MS+30bps (guidance was MS +33bps area)

- Books closed in excess of E37.5bln (inc E2.1bln JLM interest)

- Coupon: Long first

- Maturity: Feb 1, 2036

- ISIN: EU000A2SCAX8

For both:

- Total Size: MNI expected E5-7bln with upside risks. The combined size is therefore the top of our expected range.

- Bookrunners: BARCLAYS (DM/B&D) / DB / GSBE SE

- Settlement: Jan 19, 2026 (T+5)

- Timing: Allocations and pricing to follow

From market source / MNI colour